Asian Currencies: New Global Scapegoats

In

mid-July, Alan Greenspan, chairman of the US Federal

Reserve, while deposing before a congressional committee,

warned the Chinese authorities that they could not

continue to peg the renminbi to the US dollar, without

adversely affecting the functioning of their monetary

system. This touching concern for and gratuitous advice

to the Chinese had, however, some background. Greenspan

was merely echoing the sentiment expressed by a wide

circle of conservative economists that the Chinese

must float their currency, allow it to appreciate

and, hopefully, help remove what is being seen as

the principal bottleneck to the smooth adjustment

of the unsustainable US balance of payments deficit.

China was, of course, only the front for a wide range

of countries in Asia, who were all seen as using a

managed and "undervalued" currencies to

boost their exports. Around the same time that Greenspan

was making his case before the congressional committee,

The Economist published an article on the global economic

strains being created by Asian governments clinging

to the dollar either by pegging their currencies or

intervening in markets to shore them up. That article

reported the following: "UBS reckons that all

Asian currencies, except Indonesia's are undervalued

against the dollar … The most undervalued are

the yuan, yen, the Indian rupee and the Taiwan and

Singapore dollars; the least undervalued are the ringgit,

the Hong Kong dollar and the South Korean won."

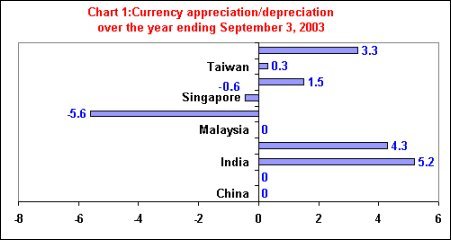

The evidence to support this is of course limited.

It lies in the fact that while over the year ending

September 3rd the euro has appreciated against the

dollar by about 9 per cent, many Asian currencies have

either been pegged to the dollar, appreciated by a much

smaller percentage relative to the dollar or even

depreciated vis-à-vis the dollar.

|

|

To anyone who has been following the debate on exchange

rate regimes and exchange rate levels in developing

countries, this perception would appear to be a dramatic

reversal of the mainstream, conservative argument

that had dominated the development dialogue for the

last three to four decades. Till recently, many of

these countries were being accused of pursuing inward

looking policies, of being too interventionist in

their trade, exchange rate and financial sector policies,

and, therefore, of being characterized by "overvalued"

exchange rates that concealed their balance of payments

weaknesses. An "overvalued" rate, by setting

the domestic currency equivalent of, say, a dollar

at less than what would have been the case in an equilibrium

with free trade, is seen as making imports cheaper

and exports more expensive. This can be sustained

in the short run because trade restrictions do not

result in a widening trade and current account deficit.

But in the medium term it seen as encouraging investments

in areas that do not exploit the comparative advantages

of the country concerned, leading to an inefficient

and internationally uncompetitive economic structure.

What was required, it was argued, was substantial

liberalization of trade, a shift to a more liberalized

exchange rate regime, less intervention all-round,

and a greater degree of financial sector openness.

Partly under pressure from developed county governments

and the international institutions representing their

interests, many of these countries have since put

in place such a regime.

Seen in this light, consistency and correctness are

not requirements it appears when defending the world's

only superpower. Nothing illustrates this more than

the effort on the part of leading economists, the

IMF, developed country governments and the international

financial media to hold the exchange rate policy in

Asian countries, responsible for stalling the "smooth

adjustment" of external imbalances in the world

system. The biggest names have joined the fray to

make the case: Alan Greenspan, chairman of the US

Federal Reserve, John Snow, US treasury secretary,

and Kenneth Rogoff, IMF chief economist.

The adoption of a liberalized economic regime in which

output growth had to be adjusted downwards to prevent

current account difficulties and attract foreign capital

had its implications. It required governments to borrow

less to finance deficit spending, which often led

to lower growth, lower inflation and lower import

demand. Combined with or independent of higher export

growth, these effects showed up in the form of reduced

deficits or surpluses on their external trade and

current accounts. Since in many cases the ‘chronic'

deflation that the regime change implied was accompanied

by large capital inflows after liberalization, there

was a surplus of foreign exchange in the system, which

the central bank had to buy up in order to prevent

an appreciation in the value the nation's currency.

Currency appreciation, by making exports more expensive

and imports cheaper, could have devastating effects

on exports in the short run and generate new balance

of payments difficulties in the medium term. In fact,

among the reasons underlying the East Asian crises

of the late 1990s was a process of currency appreciation

driven by export success on the one hand and liberalized

capital inflows on the other.

Faced with this prospect countries like China and

India chose to adopt a more cautious approach to economic

liberalization and, especially with regard to the

exchange rate regime and to the liberalization of

rules governing capital flows into and out of the

country. However, even limited liberalization entailed

providing relatively free access to foreign exchange

for permitted trade and current account transactions

and the creation of a market for foreign exchange

in which the supply and demand for foreign currencies

did influence the value of the local currency relative

to the currencies of major trading partners. This

made the task of managing the exchange rate difficult.

The larger the flow of foreign exchange because of

improved current account receipts (including remittances)

and enhanced inflows of capital (consequent to limited

capital account liberalization), the greater had to

be the demand for foreign exchange if the local currency

was to remain stable. But given the context of extremely

large flows (China) and/or relatively low demand during

the late 1990s due to deflation (India), there was

a tendency for supply to exceed demand, even if this

did not always reflect a strong trading position.

As a result, to stabilize the value of the currency

the central banks in these countries were forced to

step in, purchase foreign currencies to stabilize

the value of the local currency, and build up additional

foreign exchange reserves as a consequence.

Different countries adopted different objectives with

regard to the exchange rate. China, for example, chose

to make a stable exchange rate a prime objective of

policy and has frozen its exchange rate vis-à-vis

the dollar at renminbi 8.28 to the dollar since 1995.

To its credit, it stuck by this policy even during

the Asian currency crisis, when the value of currencies

of its competitors like Thailand and Korea depreciated

sharply. This helped the effort to stabilize the currency

collapse in those countries, even if in the immediate

short run it affected China's trade adversely. India

too had adopted a relatively stable exchange rate

regime right through this period, allowing the rupee

to move within a relatively narrow band relative to

a basket of currencies, and not just the dollar.

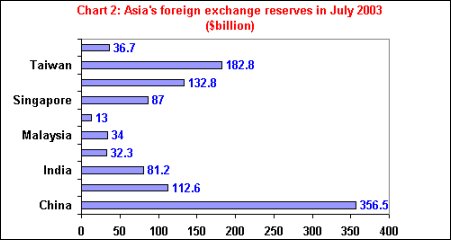

The net result is that most Asian countries –

some that fell victim to the late 1990s financial

crises, like Korea, and those that did not, like China

and India – have accumulated large foreign exchange

reserves (Chart 2). According to one estimate, Asia

as a whole is sitting on a reserve pile of more than

$1600 billion. This was the inevitable consequence

of wanting to prevent autonomous capital flows that

came in after liberalization of foreign direct and

portfolio investment rules from increasing exchange

rate volatility and threatening currency disruption

due to a loss of investor confidence. These reserves

are indeed a drain on these systems, since they involve

substantial costs in the form of interest, dividend

and repatriated capital gains but had to be invested

in secure and relatively liquid assets which offered

low returns. But that cost was the inevitable consequence

of opting for the deflation and the capital inflow

that resulted from the stabilization and adjustment

strategy so assiduously promoted by the US, the G-7,

the IMF and the World Bank in developing countries

the world over. Unfortunately, the current account

surpluses and the large reserves that this sequence

of events resulted in have now become the "tell-tale"

signs for arguing that the currencies in these countries

are "under-" not "overvalued"

and therefore need to be revalued upwards.

|

|

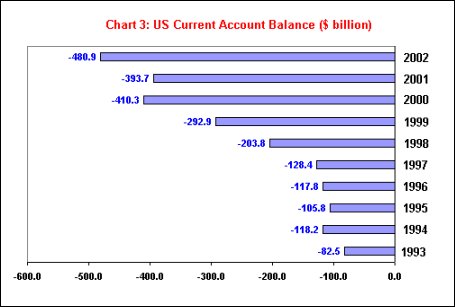

For long, this episode of rising reserves in till-recently

poor countries appeared almost conspiratorial, because

these reserves were being invested in dollar denominated

assets including government securities in the US and

played an important role in financing the burgeoning

current account deficit in the US (Chart 3). The choice

of US assets was, of course, determined by the facts

that the dollar still is the world's reserve currency

and the US the world's sole superpower, both of which

engender confidence in American, dollar-denominated

assets. The direct benefit for the US was obvious.

With America experiencing growth without the needed

competitiveness, that growth was accompanied by a

widening of the trade and current account deficits

on its balance of payments. Capital inflows into the

US helped finance those deficits, without much difficulty.

For example, UBS estimates that in the second quarter

of 2003, the central banks in Japan and China bought

$39 billion and $27 billion of dollars respectively.

If these are invested in American assets they would

finance close to 45 per cent of the estimated $147

billion US current account deficit in that quarter.

They indeed were. Central banks, mostly from Asia,

are estimated to have financed more than half of the

US current account deficit in the second quarter.

|

|

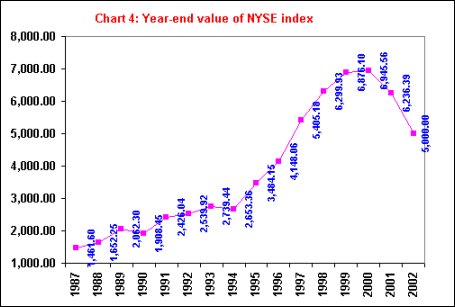

The indirect benefits of this arrangement are even

greater. For more than a decade now, the US has benefited

from a long period of buoyancy, so much so that it

has accounted for 60 per cent of cumulative world

GDP growth since 1995. That buoyancy came not because

the US was the world's most competitive nation in

economic terms. Rather, till the turn of the last

decade growth was accounted for by a private consumption

and investment spending boom, spurred by the bubble

in US stock and bond markets (Chart 4) that substantially

increased the value of the savings accumulated by

US households. The money market boom was encouraged

by the flight of capital from across the world to

the safe haven that dollar denominated assets were

seen as providing. Investment of reserves accumulated

by the Asian countries was one important component

of that capital inflow. With the value of their savings

invested in stocks and securities inflated by the

boom, consumers found confidence to spend.

|

|

To be sure, when the speculative boom came to end

in 2000, triggered in part by revelations of corporate

fraud, accounting scandals and conflicts of interest,

this spur to growth was substantially moderated. But

the low interest rate regime adopted by the Fed still

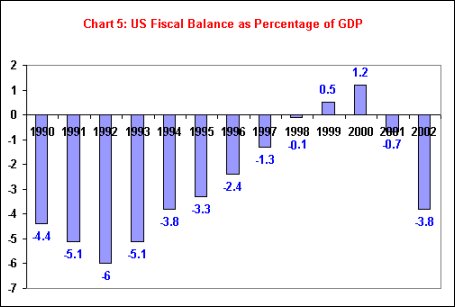

encouraged debt-financed consumer spending. Together

with the return to deficit-financed spending by the

American state (Chart 5), justified by its nebulously

defined war on terror, America is once again witnessing

buoyant output growth even if this has not improved

the employment situation significantly. In fact, 2.6

million manufacturing jobs have been lost in the US

since Bush assumed office in 2001.

|

|

The only threat to US buoyancy throughout this period

was the possible unsustainability of the widening

current account deficit in its balance of payments.

But the boom was not aborted, because the rest of

the world appeared only too willing to finance those

deficits, even if at falling interest rates in some

periods.

Unfortunately, few other countries benefited directly

from this chain of events. They did not because they

did not have the military power to create the required

confidence in their currencies, even if sheer competitiveness

warranted a decline in the dollar. Some countries

benefited indirectly: China, for example, because

of the export boom to the US; the UK because, among

other things, of a boom in services, including financial

services. But overall, to use a phrase popularized

by former US Treasury secretary Lawrence Summers,

the world economy was flying on one engine.

Within the imperial order always fearful of a "hard

landing", this has created two imperatives. First,

in the medium term, the world needs other supportive

engines, which must be from within the developed economies.

Second, till that time, and even thereafter, US growth

must be sustained. The new discovery that Asian currencies,

particularly the Chinese renminbi, is under- and not

overvalued, stems from the second of these two concerns.

With the US current account deficit expected to exceed

5 per cent this year, there are few who are convinced

that it would find investors who would be confident

enough to continue financing that deficit. This is

becoming clear from the fact that the share of the

deficit financed by central bank investments is rising,

as private investors grow more cautious. Thus, if

the dollar is not to collapse, the US current account

deficit must be curtailed and reversed.

However, this cannot be ensured by curtailing US growth

and therefore the growth of US imports. It is necessary

to boost exports, so that growth can coexist with

a reducing trade and current account surplus. This

is where China and the fact that it notched up a record

$103 billion trade surplus with the US last year comes

in. Ignoring the fact that simultaneously China had

recorded a trade deficit of $75 billion with the rest

of the world, the surplus with the US is seen as a

direct consequence of China's undervalued exchange

rate, which has been pegged to the dollar since 1995

despite rising capital flows and reserves. Thus, the

story goes, if China revalues its currency vis-à-vis

the dollar by anywhere between 15 and 40 per cent,

depending on the advocate, China would absorb more

imports from and be able to export less to the US,

correcting the trade imbalance between the two countries.

But that is not all. If China revalues its currency,

it is argued, Europe would improve its competitiveness

lost as a result of the appreciation of the euro vis-à-vis

the dollar and therefore the renminbi, allowing it

to register higher export growth. Further, China's

revaluation would reduce the need to pressurize Japan

to revalue the yen, despite its own surpluses with

the US and the high level of its reserves. This deals

with the danger that yen revaluation might abort the

feeble recovery that Japan is experiencing after a

decade of stagnation. These benefits could possibly

yield the supportive engines needed to keep the world

economy in flight.

In this assault on the less-developed nations, involving

a complete reversal of the argument regarding the

currency regime in developing countries, the US and

its allies are finding strange supporters. Trade unions

and manufacturing companies located in the US who

have experienced job and market losses have joined

the chorus through organizations such as "The

Coalition for a Sound Dollar". They are even

threatening to take the Chinese to the dispute settlement

body of the WTO on the grounds that it is manipulating

the exchange rate to win unfair gains from trade.

There effort is ostensibly aimed at invoking a provision

in the World Trade Organisation that bars countries

from influencing exchange rates to "frustrate

the intent" of WTO trade agreements. In practice,

the clamour is all intended to get the US government,

in a pre-election year, to increasing pressure on

China to float its currency.

However, not all of American business supports this

effort. Calman Cohen of the Emergency Committee for

American Trade, which represents many large US companies

doing business in China, is reported to have said

that while the renminbi may well be undervalued, it

was not the main cause of the industrial problems

facing the US. His principal and well-founded fear

is that action against China would adversely affect

US companies that as part of their competitive strategy

are sourcing their products from countries like China.

Not surprisingly, Rob Westerhof, chief executive of

Philips Electronics North America and former chief

executive of Philips Electronics East Asia, argues:

"A free float or sudden revaluation would be

bad for China and bad for business. Instead, Beijing

should maintain the peg for now and aim for a gradual

revaluation of about 15 per cent over the next five

years. Free- floating the renminbi can be considered

only when China has a well established financial system.

That will take at least another 10 years." He

made it clear that "business prefers a stable

renminbi-dollar exchange rate. A sudden revaluation

of the renminbi would disrupt results for the many

multinational companies (Philips included) that supply

American and European retail chains with goods made

in China. Currently, hedging against exchange rate

fluctuations of a free-floating, unpredictable renminbi

would be very costly for those companies."

Unfortunately, some Asian countries, particularly

those that have been experiencing an appreciation

of their currencies from the lows they reached after

the 1997 financial crisis are supporting the demand

with the hope that they would benefit from the loss

of Chinese export competitiveness that a revaluation

of the renminbi would involve. Interestingly, Japan

too is part of this group, even though it is itself

intervening in currency markets to prevent the yen

from appreciating too much against the dollar.

Thus at the end of September, the dollar recovered

sharply against the yen as a result of Bank of Japan

intervention, conducted through the New York Federal

Reserve. This help reverse a prior downward lurch

of the dollar vis-à-vis the yen. According

to information released recently by the Japanese Finance

Ministry, the government and central bank have spent

a total of $ 40 billion between August 28 and September

26, taking the total amount spent on supporting the

yen in the first nine months of 2003 to well above

$100 billion. This willingness to intervene openly

is partly explained by the fact that the G-7 has accepted

that any excessive appreciation of the yen could abort

a recovery which has come after a long while and which

is seen as crucial for overall global growth. This

support for action against yen appreciation goes against

the G-7's own recent statement that cam out in favour

of exchange rate flexibility in the world, which it

is now clear was aimed at developing Asia in general

and China in particular.

Despite its own actions, the Japanese government has

been willing to go along with the demand that the

Chinese and other developing Asian countries should

revalue their currency by opting for a float. Once

again the fact that the developed countries believe

that developing countries should do as the G-7 says

and not as it does has been brought home.

The flaws in these arguments are obvious. A revaluation

of the renminbi may reduce China's trade surplus with

the US, but it is unlikely to trigger either export

or output growth in the US. Rather, the space vacated

by the Chinese in US markets would be occupied by

some other trading country such as Vietnam, Korea

or the Philippines. Further, those Asian countries

that expect to gain from the renminbi's revaluation

would soon find that their current account surpluses

and reserves are seen as grounds for identifying their

currencies as undervalued and provide the basis for

a revaluation demand. India, with less than $90 billion

of foreign exchange reserves is already being targeted.

Whatever gains would occur from China's revaluation

would be shortlived.

Further, if China and other countries, like India,

with rising reserves are deprived of those reserves

on these grounds, the capital required to finance

the current account and budget deficits accompanying

US growth would soon dry up. This would drive up interest

rates in the US, cut consumption and investment spending,

make the current account deficit unsustainable, and

ensure the collapse of US growth and the dollar that

the revaluation is expected to stall.

In sum, the whole episode indicates that the desperation

to protect the current imperial order is yielding

a number of scatter-brained proposals. Economics has

been reduced to deformed ideology, devoid of consistency

and rationality. Fortunately, the Chinese have thus

far stood their ground and refused to yield. Hopefully,

other developing countries would also see where their

best interests lie.