Themes > Features

05.12..2008

Foreign Reserves and the Rupee

The

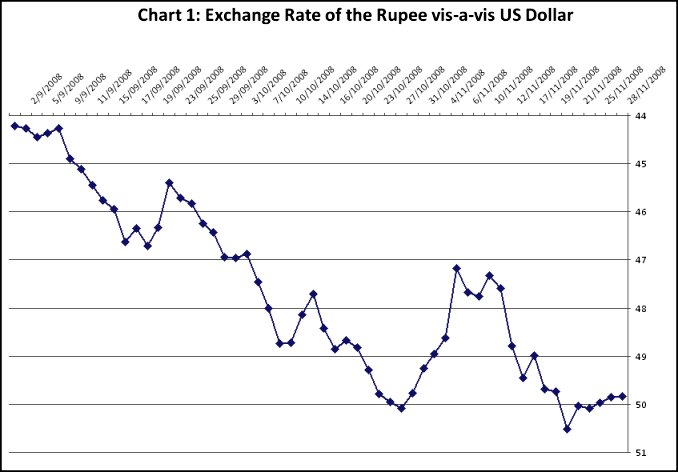

sharp depreciation of the Indian rupee from around Rs.44 to the dollar

at the beginning of September to close to Rs.50 to the dollar through

much of November gives cause for concern on many counts (Chart 1). To

start with, while it does little to increase India’s exports given similar

depreciation in the currencies of India’s competitors, it is bound to

increase the foreign exchange outflow on account of imports and worsen

the trade balance. Second, by increasing the rupee value of dollar debt

service commitments of Indian corporations, which have risen substantially

in recent years, it is bound to affect the viability of these firms at

a time when demand growth is clearly slowing. Third, increases in the

rupee prices of imports of an economy that is more import-dependent after

liberalisation would keep rupee inflation up despite lower growth. And

finally, sharp and persistent depreciation of this kind creates the possibility

of a speculative attack on the rupee that can only make matters worse.

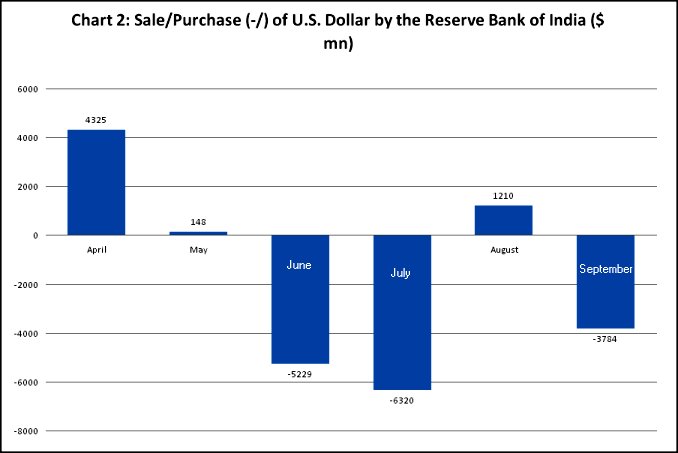

All this makes an analysis of the factors underlying the rupee’s decline imperative. What is clear is that the depreciation of the currency is not the result of any reticence or failure on the part of the Reserve Bank of India to intervene in the market to stabilise the rupee. As its Mid-Term Review of Macroeconomic and Monetary Developments declared, among the measures adopted in the wake of the global financial crisis was the decision that the Reserve Bank “would continue to sell foreign exchange (US dollar) through agent banks or directly to augment supply in the domestic foreign exchange market or intervene directly to meet any demand-supply gaps.” That this decision was implemented emerges from Chart 2, which shows that while as recently as April the RBI was purchasing large quantities of dollars and adding them to its reserves, its net sales of the dollar between June and September was as much as $14.1 billion. Indications are that sales have been as high or even higher in the two months since then.

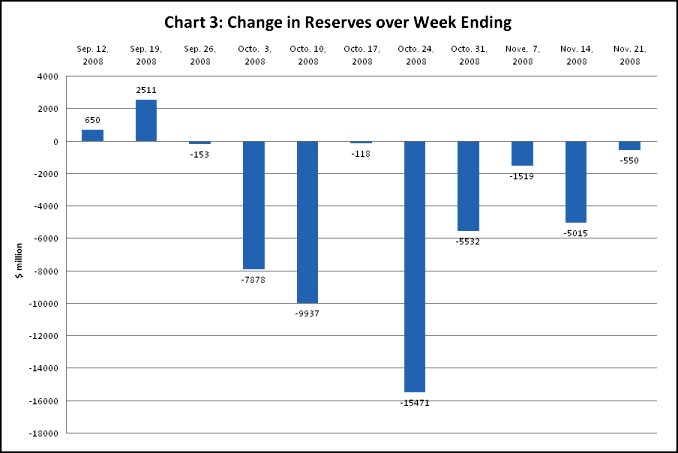

In fact, ever since the week ending October 3, in most weeks the foreign exchange assets held by the Reserve Bank of India have declined rather sharply, indicating that the central bank has been accommodating demands for foreign exchange at the expense of reserves. Overall, the decline in reserves between the end of March 2008 and November 7, 2008 has been $58.4 billion, which is a substantial proportion of the $310-plus billion India had when reserves were at their peak. What therefore seems to be creating the uncertainty that leads to rupee depreciation is not the non-availability of the dollar, but evidence that normal foreign exchange inflows are far short of the requirements needed to finance outflows, leading to a sharp fall in reserves.

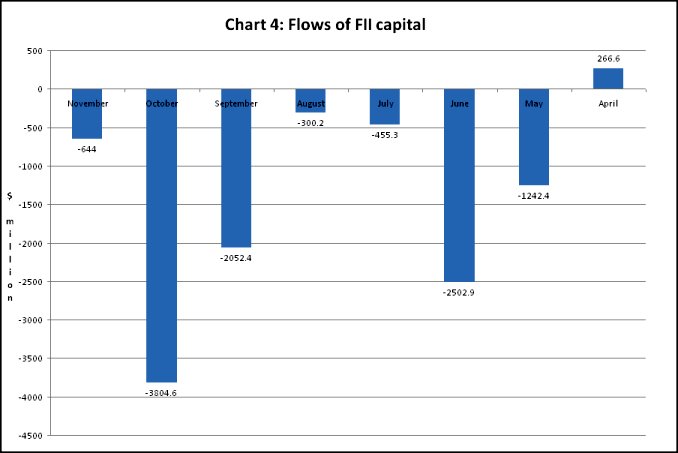

One factor responsible for the excess of outflows over inflows is of course the exodus of foreign institutional investors. But this does not seem to be the whole explanation. Total outflows from equity investments by FIIs between April and November 2008, which is seen as underlying the stock market collapse, amounted to $10.7 billion (Chart 4), or less than a fifth of the decline in reserves during this period.

This leaves outflows on account of trade related payments, which would indeed have gone up because the shrp increase in the price of oil. The average price of India’s crude import basket touched $142 a barrel on July 3, 2008. Over the period April-August, 2008 the average price of the basket stood at US $ 120.4 per barrel (having ranged between US $ 105.8 – 132.2 per barrel). This was 76.6 per cent higher than the US $ 68.2 per barrel recorded during April-August, 2007.

It must be noted, however, that the merchandise trade deficit does not does not really capture the excess demand for foreign currency emanating from the current account, because of the importance of invisible inflows in the form of remittances and software and IT-enabled export revenues in India’s balance of payments. Quarterly balance of payments figures, which are thus far available only for the April-June 2008 period (Table 2), show that while the merchandise trade deficit increased by close to $11 billion between April-June 2007 and April-June 2008, the current account deficit rose by only around $4.5 billion, because of the benefit of increased net invisible incomes.

Moreover, the drain of foreign exchange reserves during the period when the rupee was depreciating would have been far less affected by the merchandise trade deficit because of the sharp decline in oil prices. By September 10, the average price of Indian crude imports had fallen below the $100-a-barrel level, and this figure fell below $44 a barrel by November 24. This would have moderated the trade deficit, making the current account deficit much less of a factor generating an excess demand for dollars and applying downward pressure on the rupee.

In the circumstances, the drain of reserves and the depreciation of the rupee appear to be the result of one of two factors or a combination of both. The first is a possible sharp fall in inflows of capital other than foreign institutional equity investment into the economy. The balance of payments data referred to above, point to a decline in aggregate (direct and portfolio) foreign investment from $10.1 billion during April-June 2007 to $5.9 billion during April-June 2008, and a decline in foreign debt flowing into the country from $7 billion to $1.6 billion across these two periods. Given the fall out of the financial crisis, there is sufficient reason to believe that this tendency would have not just continued but intensified in the period after June 2008. If this shortfall in capital inflows accounts for the excess demand for foreign exchange, it implies that the weakness of India’s balance of payments and of the Indian rupee stem from their fact that their earlier “strength” was not earned, but merely the result of a capital surge into the country. With that surge having reversed itself the drain of reserves and the depreciation of the currency seems to have followed.

A second factor accounting for the sharp depreciation of the rupee could be speculative activity in the foreign exchange market based on expectations that the currency’s decline is inevitable. But in a liberalised foreign exchange market such speculation is bound to occur, especially when indications are that India’s balance of payments strengths were ephemeral and were being quickly reversed. In the event, even large reserves, which are still substantial and adequate to finance more than a year’s worth of imports seem insufficient to stall the rupee’s fall.

All this makes an analysis of the factors underlying the rupee’s decline imperative. What is clear is that the depreciation of the currency is not the result of any reticence or failure on the part of the Reserve Bank of India to intervene in the market to stabilise the rupee. As its Mid-Term Review of Macroeconomic and Monetary Developments declared, among the measures adopted in the wake of the global financial crisis was the decision that the Reserve Bank “would continue to sell foreign exchange (US dollar) through agent banks or directly to augment supply in the domestic foreign exchange market or intervene directly to meet any demand-supply gaps.” That this decision was implemented emerges from Chart 2, which shows that while as recently as April the RBI was purchasing large quantities of dollars and adding them to its reserves, its net sales of the dollar between June and September was as much as $14.1 billion. Indications are that sales have been as high or even higher in the two months since then.

In fact, ever since the week ending October 3, in most weeks the foreign exchange assets held by the Reserve Bank of India have declined rather sharply, indicating that the central bank has been accommodating demands for foreign exchange at the expense of reserves. Overall, the decline in reserves between the end of March 2008 and November 7, 2008 has been $58.4 billion, which is a substantial proportion of the $310-plus billion India had when reserves were at their peak. What therefore seems to be creating the uncertainty that leads to rupee depreciation is not the non-availability of the dollar, but evidence that normal foreign exchange inflows are far short of the requirements needed to finance outflows, leading to a sharp fall in reserves.

One factor responsible for the excess of outflows over inflows is of course the exodus of foreign institutional investors. But this does not seem to be the whole explanation. Total outflows from equity investments by FIIs between April and November 2008, which is seen as underlying the stock market collapse, amounted to $10.7 billion (Chart 4), or less than a fifth of the decline in reserves during this period.

This leaves outflows on account of trade related payments, which would indeed have gone up because the shrp increase in the price of oil. The average price of India’s crude import basket touched $142 a barrel on July 3, 2008. Over the period April-August, 2008 the average price of the basket stood at US $ 120.4 per barrel (having ranged between US $ 105.8 – 132.2 per barrel). This was 76.6 per cent higher than the US $ 68.2 per barrel recorded during April-August, 2007.

This does seem to have affected India’s trade deficit over the April-August 2008 period, when it stood at $49.3 billion, as compared with $34.6 billion during the corresponding period of the previous year (Table 1). This widening of the deficit was on account of the oil trade deficit which rose from $12.3 to $20.5 billion, whereas the non-oil deficit actually shrank from $13.5 billion to $9 billion.

Table

1:

India's Merchandise Trade: April-August |

||

| (US $ billion) | ||

| ITEMS | 2007-08 R | 2008-09 P |

| Exports | 60.1 | 81.3 |

| (19.3) | (35.3) | |

| Oil Exports * | 4.7 | 9.0 |

| (6.2) | (91.5) | |

| Non-Oil Exports * | 26.0 | 39.1 |

| (5.5) | (50.3) | |

| Imports | 94.6 | 130.5 |

| (34.2) | (38.0) | |

| Oil Imports | 28.8 | 46.1 |

| (42.7) | (28.3) | |

| Trade Balance | -34.6 | -49.3 |

| Oil Trade Balance * | -12.3 | -20.5 |

| Non Oil Trade Balance * | -13.5 | -9.0 |

| * : Figures pertain to April - June | ||

| R : Revised, P: Provisional | ||

| Note: Figures in parentheses show percentage change over the previous year. | ||

| Source : DGCI & S | ||

It must be noted, however, that the merchandise trade deficit does not does not really capture the excess demand for foreign currency emanating from the current account, because of the importance of invisible inflows in the form of remittances and software and IT-enabled export revenues in India’s balance of payments. Quarterly balance of payments figures, which are thus far available only for the April-June 2008 period (Table 2), show that while the merchandise trade deficit increased by close to $11 billion between April-June 2007 and April-June 2008, the current account deficit rose by only around $4.5 billion, because of the benefit of increased net invisible incomes.

Moreover, the drain of foreign exchange reserves during the period when the rupee was depreciating would have been far less affected by the merchandise trade deficit because of the sharp decline in oil prices. By September 10, the average price of Indian crude imports had fallen below the $100-a-barrel level, and this figure fell below $44 a barrel by November 24. This would have moderated the trade deficit, making the current account deficit much less of a factor generating an excess demand for dollars and applying downward pressure on the rupee.

In the circumstances, the drain of reserves and the depreciation of the rupee appear to be the result of one of two factors or a combination of both. The first is a possible sharp fall in inflows of capital other than foreign institutional equity investment into the economy. The balance of payments data referred to above, point to a decline in aggregate (direct and portfolio) foreign investment from $10.1 billion during April-June 2007 to $5.9 billion during April-June 2008, and a decline in foreign debt flowing into the country from $7 billion to $1.6 billion across these two periods. Given the fall out of the financial crisis, there is sufficient reason to believe that this tendency would have not just continued but intensified in the period after June 2008. If this shortfall in capital inflows accounts for the excess demand for foreign exchange, it implies that the weakness of India’s balance of payments and of the Indian rupee stem from their fact that their earlier “strength” was not earned, but merely the result of a capital surge into the country. With that surge having reversed itself the drain of reserves and the depreciation of the currency seems to have followed.

Table

1:

India's Overall Balance of Payments |

||

| ITEMS | $ Millions | |

| April - June 2008 P | April - June 2008 PR | |

| A. Current Account | ||

|

1. Merchandise |

-31,574 | -20,701 |

|

2.Invisible (a+b+c) |

0,850 | 14,400 |

| Total Current Account (1+2) | -10,724 | -6,301 |

|

B. Capital Acccount |

||

| 1. Foreign Investment (a+b) | 5,909 | 10,116 |

|

a) Foreign Direct Investment |

10,117 | 2,658 |

| b) Portfolio Investment | -4,208 | 7,458 |

| 2.Loans (a+b+c) | 4,083 | 9,035 |

| a) External Assistance | 351 | 241 |

|

b) Commercial Borrowings (MT<) |

1,559 | 6,990 |

| c) Short Term to India | 2,173 | 1,804 |

| 3. Banking Capital (a+b) | 2,735 | -919 |

| 4. Rupee Debt Service | -30 | -43 |

| 5. Other Capital | 518 | -843 |

| Total Capital Account (1to5) | 13,215 | 17,346 |

|

C. Errors & Omissions |

-256 | 155 |

|

D. Overall Balance |

2,235 | 11,200 |

| ii) Foreign Exchange Reserves | -2,235 | -11,200 |

| ( Increase - / Decrease +) | ||

| P: Preliminary PR: Partially Revised | ||

A second factor accounting for the sharp depreciation of the rupee could be speculative activity in the foreign exchange market based on expectations that the currency’s decline is inevitable. But in a liberalised foreign exchange market such speculation is bound to occur, especially when indications are that India’s balance of payments strengths were ephemeral and were being quickly reversed. In the event, even large reserves, which are still substantial and adequate to finance more than a year’s worth of imports seem insufficient to stall the rupee’s fall.

©

MACROSCAN 2008