The Burden of Farmers' Debt

The

agrarian crisis that has rampaged through rural India for the past few

years has been associated very clearly with a rising burden of indebtedness

among farmers. The inability to repay past debt - and therefore to access

fresh loans - has been widely accepted as the most significant proximate

cause of the farmers' suicides that were so widespread in Andhra Pradesh

and Karnataka, and are apparently continuing in areas as far apart as

Wayanad in Kerala, Vidarbha in Maharashtra and some areas of Punjab

and Rajasthan.

Despite this, apart from

reports from the field by some persistent journalists and other observers,

there has been nothing in the shape of aggregate data that would provide

some estimate of the actual extent of rural indebtedness. These reports

have suggested that the decline in access to institutional credit has

driven more farmers back to potentially more exploitative usurious relations

with traditional moneylenders or input dealers. Repayment problems,

resulting from the greater difficulties of cultivation because of rising

input prices and volatile output prices, have been compounded by the

higher interest rates charged by these informal sources.

Until recently, however, there has been no way of verifying these perceptions

on the basis of a large dataset based on information garnered from across

the country. Therefore, the recent report of the National Sample Survey,

based on the 59th Round Survey conducted in 2003, is particularly important,

since it provides the first systematic evidence since 1992, on the causes,

extent and sources of farmers' debt.

This is part of a series of reports based on the Situation Assessment

of Farmers, which covered the educational level of farmer households;

level of living as measured by consumer expenditure, income, productive

assets and indebtedness; their farming practices and preferences; resource

availability; awareness and access to technological developments etc.

The survey was conducted only in the rural sector of the country over

January to December 2003. In all 51,770 households spread over 6,638

villages were surveyed in the Central sample. The survey did not cover

landless workers.

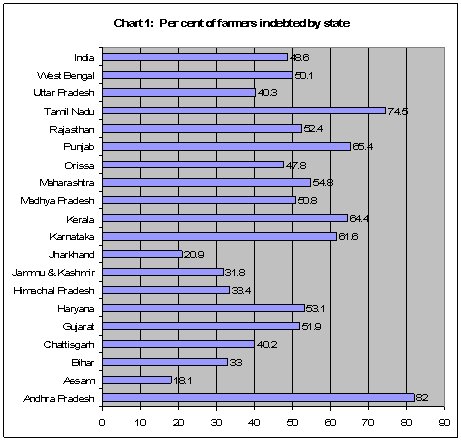

As expected, the extent of farmers' indebtedness emerges as very substantial.

As Chart 1 indicates, nearly half (48.6 per cent) of farmers households

were reported to be indebted. This is clearly a very substantial extent

of recorded debt, and also represents a substantial increase over time.

A similar survey by the NSS relating to 1991 found indebtedness among

only 26 per cent of farmers.

The incidence of indebtedness was the highest in Andhra Pradesh, where

more than four-fifths of surveyed farmers were in debt, followed by

Tamil Nadu with nearly three-fourths of farm households reporting indebtedness.

In Punjab, Kerala and Karnataka the proportion was nearly two-thirds,

and in Maharashtra, Haryana, Rajasthan, Gujarat, Madhya Pradesh and

West Bengal more than half of the farmers surveyed were in debt. It

is worth noting that some of the states where the agrarian distress

is reported to be especially severe, such as Andhra Pradesh, Karnataka,

Maharashtra, Punjab and Rajasthan, are also those which report high

levels of indebtedness.

The

proportion of indebted households appeared to be around the same, which

is between 48 and 52 per cent of households, across cultivating households

as well as those who received income from related activities such as

animal husbandry, poultry and fishery, and management of orchard crops.

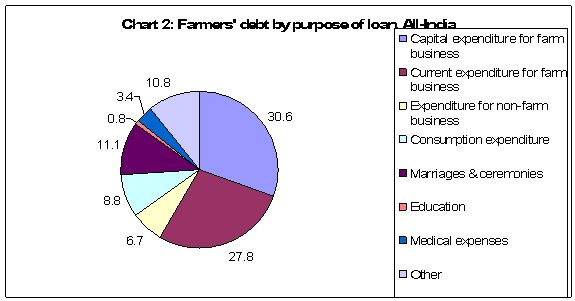

It is significant that the

dominant cause for taking loans was found to be for productive purposes.

Chart 2 provides this information, and shows that the two most important

purposes of taking loans were stated to be ''capital expenditure in

farm business'' and ''current expenditure in farm business'. At the

all-India level, out of every 1000 rupees taken as loan, 584 rupees

had been borrowed for these two purposes taken together.

The highest such proportion was in Maharashtra, where 75.4 per cent

of loans were taken for the purposes of productive investment on farms,

whether in the form of capital or current expenditure, followed by Karnataka

with 68.2 per cent. In Punjab, Andhra Pradesh and Uttar Pradesh the

proportion exceeded 60 per cent of the total amount of loans. As such,

this shift towards more emphasis on more productive loans would appear

to be desirable, but the problem in the recent past has been that even

such loans have been difficult to repay because of changes in production

conditions, leading to a vicious cycle of indebtedness. So cultivation

itself has become less economically viable over time.

The next important purpose

of taking loans was for spending on ''marriages and ceremonies'', which

however accounted for a much smaller proportion of total loans, at around

11 per cent. This purpose was most important for farmer households of

Bihar (22.9 per cent) followed by those in Rajasthan (17.6 per cent).

This is relatively small and certainly runs counter to any perception

that such unproductive expenditure is the dominant cause of farmers'

indebtedness.

A more worrying aspect that emerges is the significance of pure consumption

loans - these accounted for 8.8 per cent of all amounts borrowed by

farmers at the all-India level, and as much as 13.8 per cent in Rajasthan.

The persistence of such consumption loans is a sad comment indeed on

the viability of cultivation, and on the lack of progress in improving

basic survival conditions of agriculturalist families.

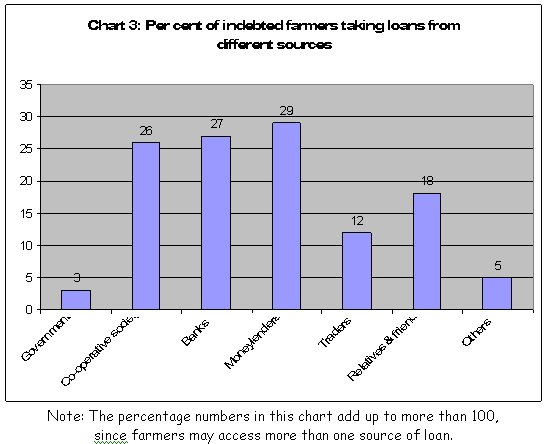

A question of great interest relates to the source of loans. The basic

purpose of bank nationalisation and the focus on agricultural credit

co-operatives was to extend the reach of institutional credit, so as

to weaken the stranglehold of traditional moneylenders and thereby ease

the credit conditions facing ordinary peasants. However, financial liberalisation

policies from 1992 have led to the progressive weakening of ''priority''

lending to agriculture and a substantial decline in the extension of

institutional credit to cultivators per capita or in terms of production

costs.

The consequence of this is

evident in Chart 3, from which it is clear that moneylenders have emerged

as the most significant source of credit for farmers, with 29 per cent

accessing this source. The influence of moneylenders appears to be especially

strong in Bihar (44 per cent) and Rajasthan (40 per cent). Traders -

of both inputs and outputs - also have provided loans to 12 per cent

of indebted farmers. However, institutional sources still remain significant,

with more than half of farmers accessing government, co-operative societies

and banks taken together.

The other striking feature that emerges from the survey is how widespread

indebtedness is across size classes of farmers. Table 1 indicates, as

expected, that the average amount of the outstanding loan increases

with the size of the land holding, but what is more interesting is that

the proportion of indebted farmers also increases with the size class.

Further, even among very small and marginal farmers, the amount of outstanding

loan is substantial, given the likely low incomes from such small holdings,

which suggests some sort of cumulative process leading to a debt trap

for the very resource poor cultivators.

Table

1: Per cent of indebted farmers by size of land holding |

||||||

Size

of land holding (hectares) |

Per

cent of indebted farmers |

Average

loan outstanding (Rs.) |

||||

Less

than 0.01 |

45.3 |

6,121 |

||||

0.01-0.4 |

44.4 |

6,545 |

||||

0.4-1.0 |

45.6 |

8,623 |

||||

1.01-2.0 |

51.0 |

13,762 |

||||

2.01-4.0 |

58.2 |

23,456 |

||||

4.0-10.0 |

65.1 |

42,532 |

||||

More

than 10 |

66.4 |

76,232 |

||||

All |

48.6 |

12,585 |

||||

Clearly,

the rural debt situation, especially for cultivators, is grim, and requires

urgent policy attention. A beginning has been made by the UPA government

in terms of increasing the provision of institutional credit to farmers,

but as this brief discussion has shown, that is only a part of the problem.

To rescue farmers from debt traps that have come about because they

have taken production loans, it is necessary to confront the problems

currently afflicting the viability of cultivation.

The problem

of agricultural indebtedness is intimately linked with issues of undesirable

input use, constantly increasing input costs, volatile crop prices and

difficulties in accessing markets. Therefore, it is to these aspects

of production conditions in agriculture that policy intervention must

now be directed.