Economic Reform and Inflation

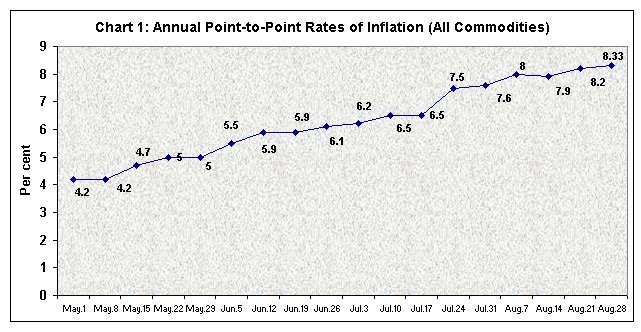

Inflation is clearly a cause for concern for the UPA government. Among the few economic policy initiatives it has taken in its less-than-four months in office, efforts to rein in inflation dominate. The reason: As on August 28, the point-to-point annual rate of inflation as measured by the Wholesale Price Index (WPI) stood at 8.33 per cent. The climb to that figure has been consistent, starting from 4.2 per cent on an annualised basis on May 1.

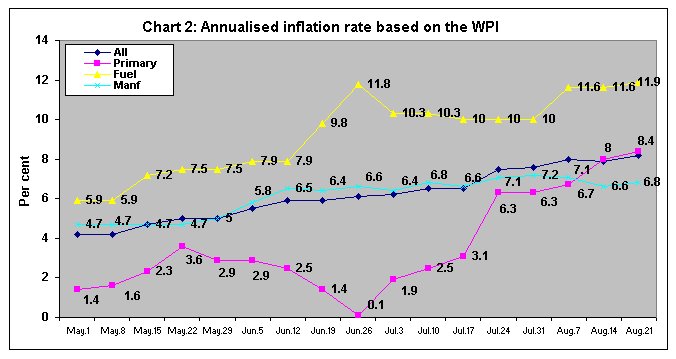

Interestingly, other than an effort to squeeze liquidity by raising the cash reserve ratio, the government's anti-inflation drive has focused on individual commodities such as oil, steel and sugar. This is because the evidence indicates that the inflationary spurt is in large part accounted for by a few commodity groups.

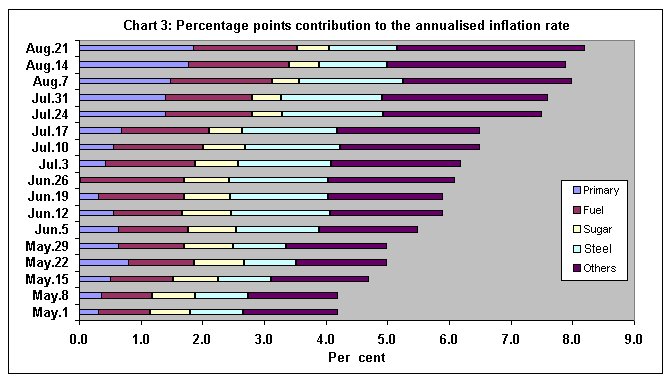

Specifically, the sharp rise in the inflation rate is attributable to Fuel, Primary articles and Steel, with Sugar playing a small role as well. At the beginning of May this year, this set of commodities contributed a total of 2.7 percentage points to the 4.2 per cent inflation rate. By August 21, they contributed 5.2 percentage points to the 8.2 per cent inflation rate.

Thus

throughout the period of the inflationary spurt, these commodities accounted

for between 63 and 71 per cent of the annualised inflation rate computed

every week. In fact, even the residual one-third of the inflation rate

is in part attributable to some of these commodities. These commodities,

especially oil and steel, enter into the costs of production of a range

of others, with oil being in the nature of a universal intermediate.

Hence, any increase in their prices has second-order effects that translate

into a more generalised inflation. The sharp increase in oil and steel

prices relative to the corresponding period of the previous year would

have raised the costs of production and therefore the prices of all

commodities, including those that are implicitly being categorised under

the residual ‘Others' category in this discussion. Thus, any assessment

of the factors underlying inflation has to focus on the factors that

cause the price rise in this set of commodities.

Seen in these terms, the current inflation appears to be driven substantially

by external factors, since domestic inflation in oil and steel is obviously

driven by international price trends. In the case of oil, a host of

developments varying from the war in Iraq, the troubles in Venezuela

and the controversies that dog the Russian oil industry, have ensured

that prices continue to rule well above the $40-per-barrel level. Given

the much lower levels at which oil prices prevailed during the corresponding

months of the previous year, the figures yield a high annualised increase

in international oil prices.

Steel prices too have been buoyant for a long time now. Global steel

prices rebounded sharply in 2002 from a 20-year low the year before.

Since then they have been buoyant, sustained by a surge in demand from

China. In 2003, the sharp rise in consumption in Asia and particularly

in China had helped offset stagnation in the West and brightened the

outlook for the leading steel producers in Europe, Japan and the US,

which had otherwise been cutting production in order to support prices.

They had by then opted to exploit the strong market with higher margins

that spelt high profits.

Since then demand in China has remained strong despite expectations

that it would taper off. According to the International Iron and Steel

Institute (IISI), the world's steel demand is forecast to swell to 917

million tons this year, breaking through the 900-million-ton mark for

the first time. Chinese demand for steel products is predicted to reach

263 million tons in 2004, accounting for 29 per cent of the total global

demand. With China's high steel consumption expected to last, global

steel demand is projected to grow at an annual average of 4.6 per cent,

reaching 1.04 billion tons in 2007. In the event, international steel

prices are expected to keep their uptrend even after 2005 owing to a

supply-demand imbalance.

These developments in the international economy have impacted India

adversely because the government's liberalisation policy has either

consciously sought to link domestic prices to world prices or trade

liberalisation has ensured that border prices drive domestic prices

in the country. Prior to the repeal of the administered pricing regime

in oil, its domestic price was considered one of the instruments of

the government tax-cum-subsidy regime. As domestic prices were stable

when international oil prices fell, the oil companies accumulated surpluses

through an implicit tax on consumers, which were available for investment

purposes or were transferred to the government's budget. On the other

hand, when international oil prices ruled high, the oil companies incurred

losses which had to be either implicitly (through finance for expenditures)

or explicitly be subsidised by the government through its revenues from

elsewhere. The repeal of administered pricing has meant that fluctuations

in global oil prices directly impact the consumer.

In the case of steel, matters are slightly different. Prior to steel

price decontrol, domestic prices were fixed at a level that covered

domestic costs of production and offered producers a reasonable rate

of return. But even after decontrol, any tendency for the prices of

the metal or its products to rise excessively because of buoyant market

conditions was implicitly controlled, because of the strong presence

of the public sector enterprises in the industry and the strong arm

of the government in the public sector. Liberalisation has changed all

that. Internal liberalisation has meant that domestic producers, including

the public sector, are free to set prices depending on what the market

would bear. And with restrictions on imports and exports removed under

the liberalised trade policy, what the market would bear has come to

be determined by the level of global prices. Thus, international supply

and demand balances determine domestic steel prices as well.

It could be argued that given the high share of imported crude and oil

products in domestic consumption, some link between domestic and international

prices is inevitable, if the government is not to be subsidising oil

consumption indiscriminately. But the same argument can hardly apply

to steel where domestic prices have risen sharply despite the ability

of the domestic industry to meet domestic demand. According to official

sources, the domestic price of hot-rolled coils had increased to Rs

29,875 per tonne in May 2004 from Rs 20,500 per tonne in January 2003

and Rs 15,500 per tonne in January 2002. Similarly, the price of cold-rolled

coils had risen to Rs 34,300 per tonne in May 2004 from Rs 26,000 per

tonne in January 2003 and just Rs 19,500 per tonne in January 2002.

Cost increases do not explain the price spurt, and has resulted in huge

profits for the steel producers.

In sum, India's dependence on imports of crude oil and her integration

into the world steel market, combined with a more market-driven pricing

system, has contributed in substantial measure to the current rate of

inflation. The net effect is that in the case of both oil and steel,

liberalisation has meant that global trends have resulted in sharp increases

in domestic prices as well. These price increases have resulted in these

contributing as much as 1.5-1.7 percentage points each to the 6-7.5

per cent rate of inflation between mid-June and early-August.

The price increase has been partly moderated through a reduction in

duties imposed on petroleum and petroleum products. But so long as the

view that domestic oil prices should keep pace with international values

prevails, there are limits to which the domestic inflation rate can

be insulated from the effects of international oil price trends.

Unfortunately, this has been combined with an indifferent and uneven

monsoon that was delayed substantially in many parts of the country.

While this is not expected to result in agricultural output shortfalls

of the kind witnessed in 2002-03, production is not likely to equal

that in 2003-04. Fortunately, given the current food stock position,

this would not result in any imbalance between demand and supply. However,

the uncertainties over the monsoon have provided the basis for speculative

price increases in the case of a number of primary commodities, resulting

in a significant inflation in the wholesale price indices for Primary

articles. As a result this too has contributed to the sharp rise in

prices.

Finally, in the case of sugar, a decline in production over two years

has resulted in a significant fall in the level of stockholding. This

has triggered a price increase, fuelled by speculation, even though

international prices in this case have been subdued.

The congruence of this set of factors explains the return of inflation,

which once again is grabbing headlines. It must be said that, compared

to its lethargy in most other areas, the government's response on this

front has been quick and varied. This response has included duty cuts

on petro-products and steel, a 50-basis-point hike in the cash reserve

ratio and relaxation of the norms with regard to sugar imports. Raw

sugar imports are now allowed duty-free with the obligation to export

from domestic production within 24 months. In the case of steel, the

government has also sought to deal with this problem by forcing domestic

producers to hold and even cut their prices.

Thus the response is three-fold in nature. First, it attempts to moderate

the effects of global price movements on domestic inflation by making

compensatory reductions in domestic duties and persuading domestic suppliers

to hold their prices. Secondly, it attempts to dampen speculation by

reducing liquidity in the system through measures such as the hike in

the cash reserve ratio. And, thirdly, it seeks to reverse domestic price

increases by facilitating larger imports.

None of these is likely to be effective enough to deal with the problem.

However, the problem is that in the wake of liberalisation, the government

has left itself with few options to deal with situations like this.

Duty cuts can only be carried to a limit, and in any case worsen the

government's already weak fiscal position. The use of monetary levers

is ineffective and already under attack from industry because it could

push up interest rates. And imports are not an effective option since

it is international prices that drive domestic inflation in any case.

So long as increases in the international prices of oil and steel persist

and the link between domestic and international prices is not sought

to be directly broken, measures such as duty reductions can only serve

as short-term and partial palliatives. It is also unlikely that half-hearted

measures to reduce liquidity can make any difference to speculation.

And, finally, easier imports can make a difference only in the case

of commodities like sugar and edible oils, in whose case international

prices are subdued. But their contribution to the inflation rate is

the least. Hence, unless there is a change in policy stance, inflation

is likely to persist so long as international prices of oil and steel

remain buoyant and the base for speculative price increases in primary

commodities exists.

The danger is that this inflation driven by international price trends

and speculation rather than by demand-supply imbalances would provide

an argument for further fiscal contraction, even though food stocks,

foreign exchange reserves and unutilised capacity warrant an expansionary

fiscal stance. If that happens, the still slow progress on implementing

the National Common Minimum Programme would soon be halted.