Employment Shifts after the Global Crisis*

For

more than a year now, it has been evident that the ''recovery'' from

the Great Recession, which has been visible if sputtering in terms of

output growth in the core capitalist countries, has not delivered anything

like the increases in employment that were expected. A recent report

of the ILO (''Short-term employment and labour market outlook and key

challenges in G20 countries'', ILO and OECD September 2011, page 1)

points out: ''With economic activity slowing in several major economies

and regions, earlier improvements in the labour market are now fading,

hiring intentions are softening and there are greater risks that high

unemployment and under-employment could become entrenched. This makes

for a highly uncertain outlook as to the timing and strength of a future

recovery in employment. Continued weak growth in employment in many

G20 countries, in turn, will make it impossible in the near term to

close the jobs gap accumulated during the crisis, which amounts to more

than 20 million jobs.''

Even the IMF, notorious for giving relatively short shrift to employment

and seeing it as generally strongly correlated with output, has woken

up to the severity of the problem in its latest World Economic Outlook

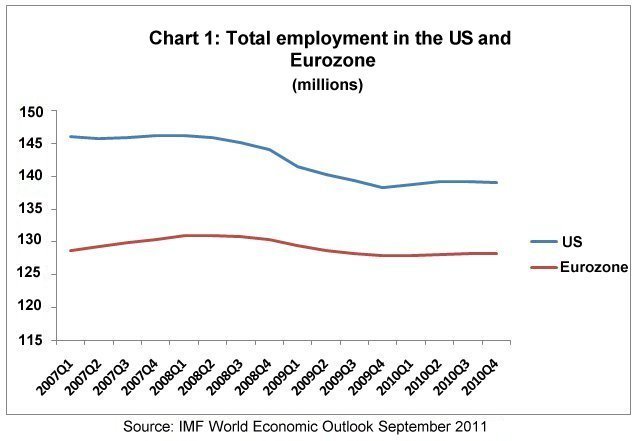

September 2011. As Chart 1 indicates, the collapse of aggregate employment

in the US and the continued stagnation at low levels in the eurozone

do not point to any real recovery at all in terms of employment. Now

that the global economic horizon has been darkened once again by very

real fears of the next dip, the concern is that employment conditions

will deteriorate further.

It

is true that the IMF’s analysis of the problem and possible solutions

remains weak, also because it continues to stress the need to encourage

''a rebalancing from public to private demand'' in these core capitalist

regions, at a time when this is completely unrealistic to expect. A

major cause of the crisis was the excessive build-up of private debt

(taken by both households and companies) that could not be sustained.

These private agents now necessarily have to go through a period of

deleveraging. In that period, if aggregate demand has to grow at all,

it must come from the public sector – but the combination of bond market

vigilantes and fiscal hawks active politically has forced governments

in both these areas to move to premature fiscal retrenchment.

In this analysis, the fact that there was not more of an employment

recovery is a source of surprise. After all, the G20 countries did at

first combine to provide very large fiscal stimuli in the major countries,

and in the developed world monetary easing has continued, leaving the

world economy awash with liquidity. The argument seems to be ''we adopted

Keynesian policies, but they have not delivered employment growth''.

This is actually less than the truth. Part of the problem is that the

stimulus measures adopted in most countries were not weighted in favour

of employment generation: a disproportionate amount went as bailouts

and support to large financial institutions that simply used the resources

to clean up their balance sheets. In the US, very little of the money

went into direct state spending on activities that directly increase

employment or have high multiplier effects. Social spending and government

employment fell as local governments were strapped for cash; small businesses

have been starved of bank credit; there has been no systematic attempt

to address the continuing problem of foreclosures in residential housing

markets. And now, even these half-hearted and slipshod stimulus measures

are to be clawed back with the new focus on fiscal austerity.

In Europe the imbalances in the eurozone are also being dealt with in

a counterproductive manner – forcing regressive austerity measures on

to deficit countries and sending them into a downward spiral of falling

output and employment in which their fiscal and public debt measures

will only get worse. It is ridiculous to expect private investment and

activity to increase to fill the slack created by public cuts, in this

context of continuing crisis. So it is not surprise that employment

is not recovering.

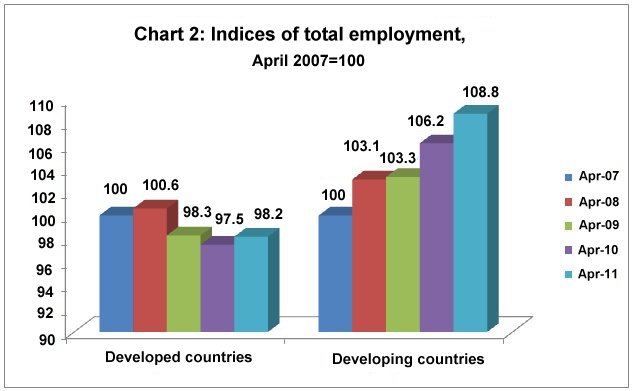

The poor performance of employment in the developed countries has reinforced

perceptions that the crisis has intensified and accelerated structural

shifts in global employment away from the rich countries to certain

emerging markets. Certainly, the data presented in Chart 2 would appear

to support that view. It is evident that total employment in developed

countries has still not recovered to pre-crisis levels. However, in

developing countries total employment did not fall after the crisis,

and since then has continued to rise.

The data in Charts 2 to 5 (all from the ILO’s Short Term Indicators

of the Labour Market, September 2011) should be interpreted with some

caution, since they relate only to (around 54) countries that provide

recent employment data of the required periodicity, and large countries

such as China and India are therefore excluded. Even so, they provide

a quick estimate of the ongoing trends.

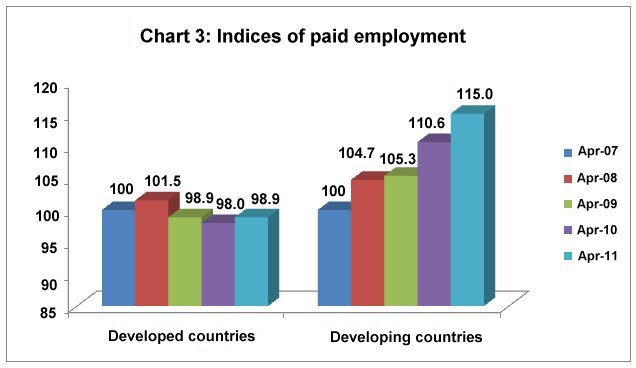

Chart 3 indicates a similar picture for paid employment (or number of

employees): - the slight decline followed by stagnation at below pre-crisis

levels in the developed world accompanied by continuing increase in

such numbers in the developing world. The level of paid employment in

April 2011 was around one per cent below pre-crisis levels in the developed

countries for which estimates are available, but 15 per cent higher

for developing countries.

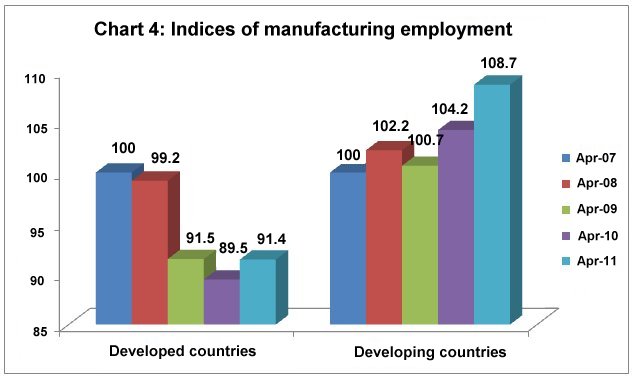

The biggest shift, and the one that has grabbed the most attention and created disquiet in rich countries, is the shift of manufacturing employment. This was a shift that was widely discussed but did not actually take place in the preceding decades: in fact aggregate manufacturing employment in the developing world did not increase despite the widespread perception of the North ''exporting jobs'' to the South. But the very recent trends after the global crisis suggest that the shift may be occurring now.

Chart 4 shows that manufacturing employment in developed countries was

more than ten per cent below the pre-crisis level in April 2010, and

has since recovered only slightly to be still around 9 per cent lower

in April 2011. Meanwhile, after a minor blip in early 2009, manufacturing

employment in developing countries continued to increase, such that

in April 2011 it was nearly 9 per cent higher than its level of four

years earlier.

Surely this is a clear sign that the much feared (or much anticipated)

shift of manufacturing activity to the South is finally taking place

and that the location of additional manufacturing employment will now

be concentrated in the South? It turns out that even this is not so

clear, if such employment is further disaggregated.

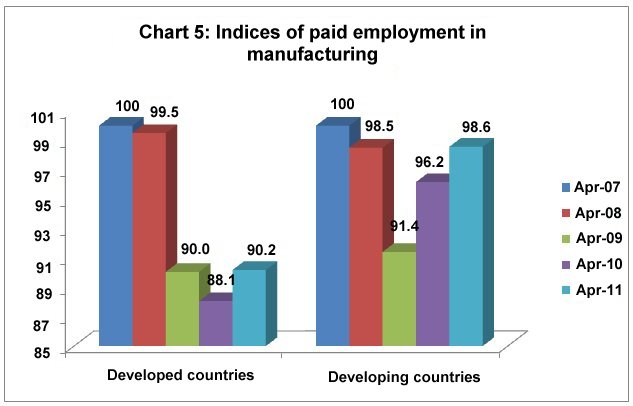

Chart 5 shows the indices of paid employment in manufacturing (that

is, the total number of employees rather than self-employed engaged

in manufacturing activity). This presents quite a different picture:

one in which the level have fallen after the crisis, in both developed

and developing countries! Indeed, in April 2009 the collapse in paid

manufacturing employment was similar in both regions, at around 8-10

per cent lower than the April 2007 level. The recovery in developed

countries thereafter was negligible. Such employment recovered more

rapidly and sharply in developing countries, but in April 2011 the level

was still below the pre-crisis level of paid manufacturing employment

even in developing countries.

So

the only real increase in manufacturing in developing countries seems

to have been in self-employment. What exactly does this mean? This really

points to the proliferation of petty activities at the bottom of the

production chain, typically in low productivity and low paid work that

usually reflects the absence of other viable income earning opportunities.

The expansion of self-employment in manufacturing in the developing

world, including in some of the most ''dynamic'' emerging markets, cannot

be seen as a very positive sign of industrial relocation, especially

in a world in which economies of scale are still rampant. It essentially

indicates a growing tendency to newer forms of organisation of production

in which there is international centralisation of production but decentralisation

of the actual work processes, with the risks of production borne largely

by the self-employed workers themselves, at the bottom of the production

chain.

Recently released survey data from India (the National Sample Survey

for 2009-10) suggest that even such employment, low paid and adverse

as it is, can also be fragile and transient and therefore decline. If

this is a more widespread tendency, when more data are eventually available

for all developing countries, we may find that aggregate manufacturing

employment in developing countries has barely recovered after the crisis.

*

The article was originally published in the Business Line, October 3,

2011