The New Structure of Global Balances

An

unusual and striking feature of the current global balance of payments

situation is the huge deficit on the current account of the world’s

dominant country, the United States, which is partly being financed

with surpluses in the current and capital account of developing countries,

especially those in developing Asia. At the end of the second quarter

of 2004, the annual current account deficit in the US balance of payments

stood at $572 billion and was forecast to touch 5.5 per cent of GDP

in 2004. At around the same time, 9 developing countries in Asia and

Latin America (Brazil, China, Hong Kong, India, Indonesia, Malaysia,

Singapore, South Korea, Taiwan, and Venezuela) were recording an annual

surplus of around $190 billion on their current account.

To boot, many of these developing countries were recipients of large

capital inflows-in the form of foreign direct investment, portfolio

capital and debt-resulting in surpluses on the capital account. Together

these current and capital account surpluses were adding to their reserves,

which in turn were being invested in dollar denominated financial assets,

thereby financing in part the US deficit.

Weekly data from the Federal Reserve relating to November 3, 2004 showed

the Fed's holdings of assets for official institutions - which is a

proxy for foreign central bank holdings - rose over the previous year

by $253.6 billion to $1,053 billion. This compares with a rise of $217

billion during the whole of 2003. Needless to say, not all of these

investments are from developing countries, since Japan is a major investor.

The Japanese government spent a record $180 billion in 2003 on intervention

in foreign exchange markets and much of that money found its way into

the US Treasury market. During that period, Japan's foreign exchange

reserves rose by $203.8 billion to $673.5 billion. In the first two

months of this year, those reserves rose a further 15 per cent to $776.9

billion. While developing countries may not be playing a similar role,

their contribution is still important.

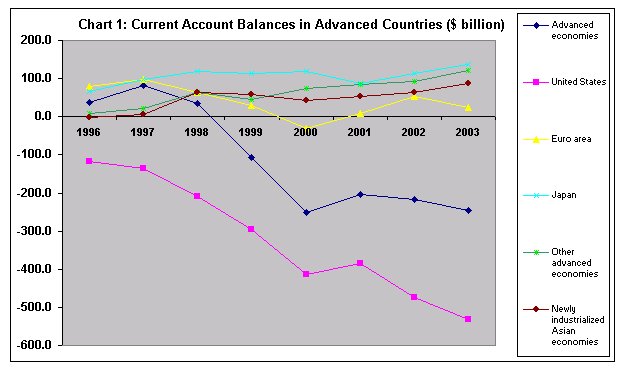

As Chart 1 shows, the current account deficit in the US has widened

continuously since the mid-1990s, resulting in an overall deficit for

all advanced economies, despite the fact that every one of them has

shown surpluses in almost all those years. On the other hand, during

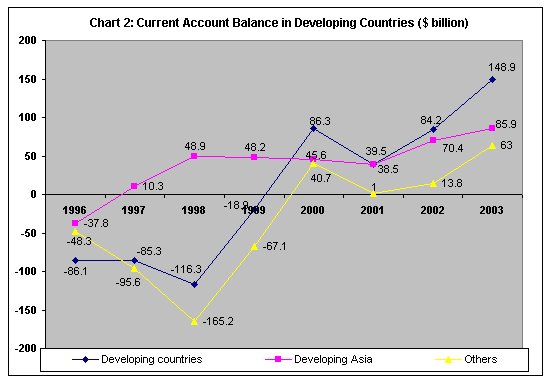

this period developing countries as a group have seen a transformation

of their current account deficits into surpluses (Chart 2). While this

was true initially of a set of countries in Asia, they have since been

joined by countries in West Asia, the Commonwealth of Independent States

(included by the IMF in the developing countries and emerging markets

group) and Latin America, though not Africa and Central and Eastern

Europe. However, developing and emerging market countries outside Developing

Asia have also been recording a surplus as a group.

This implies that three decades of globalisation have fundamentally

transformed the international balance of payments situation. Prior to

the oil shocks, which were important triggers for the major changes

in the quantum and nature of international capital flows, the international

payments scenario reflected differences in the global economic strength

of individual nations. The scenario was one where the developed countries

recorded large surpluses, the oil-exporting developing countries much

smaller surpluses and the oil-importing developing countries were burdened

with significant deficits. The process of restoring global balance involved

adjusting growth in the oil-importing developing countries so as to

tailor their deficits to correspond to the extent to which surpluses

from the developed countries could be recycled to finance those deficits.

Though for a short period after the oil shocks of the 1970s this situation

changed with surpluses in developed countries falling, those earned

by the oil exporters rising sharply and deficits in the oil-importing

developing countries exploding, the picture returned to its pre-oil

shock form by the 1980s. Even when oil exporters were earning large

surpluses, the fact that these surpluses were being deposited within

the banking system in the developed world made the process of recycling

surpluses one of transfers from the developed to the oil-importing developing

countries. The real change was that private rather than official flows

through the bilateral and multilateral development network came to dominate

capital flows.

Associated with this shift was a transformation of capitalism in the

developed countries which witnessed the rise to dominance of finance

capital. To start with, oil surpluses deposited with the international

banking system resulted in a massive increase in credit provision, both

within the developed countries and in the so-called emerging markets.

Second, the breakdown of the system of fixed exchange rates triggered

by the US decision to delink the dollar from gold, resulted in a sharp

increase in foreign exchange trading. Third, growing exposure of financial

agents in domestic and international debt markets and in foreign exchange

markets resulted in the burgeoning of derivatives that allowed financial

institutions to hedge their bets by transferring credit risk. And, finally,

the liberalisation of financial markets in developing countries aimed

at exploiting the benefits of a global financial system awash with liquidity

provided an opportunity for banks, pension funds and other financial

firms to increase their investments in developing countries in search

of lucrative returns.

The long term effects of these developments are there to see. Available

figures point to galloping growth in the global operations of financial

firms. In the early 1980s, the volume of transactions of bonds and securities

between domestic and foreign residents accounted for about 10 per cent

of GDP in the US, Germany and Japan. By 1993, the figure had risen to

135 per cent for the US, 170 per cent for Germany and 80 per cent for

Japan. Much of these transactions were of bonds of relatively short

maturities.

Since then, not only have these transactions increased in volume, but

a range of less traditional transactions have come to play an even more

important role. Traditional bank claims, though important, are by no

means dominant. Banks reporting to the Bank of International Settlements

(BIS) recorded foreign claims on residents of all countries at $15.7

trillion at the end of 2003. This compares with the annual global GDP

of $36400 trillion in that year.

Non-bank transactions have been far more important. In 1992, the daily

volume of foreign exchange transactions in international financial markets

stood at $820 billion, compared to the annual world merchandise exports

of $3.8 trillion or a daily value of world merchandise trade of $10.3

billion. According to the recently released Triennial Central Bank Survey

of Foreign Exchange and Derivatives Market Activity, in April 2004,

the average daily turnover (adjusted for double-counting) in foreign

exchange markets stood at $1.9 trillion. With the average GDP generated

globally in a day standing at close to $100 trillion in 2003, this appears

to be a small 2 per cent relative to real economic activity across the

globe. But the sum involved is huge relative the daily value of world

trade. In 2003, the value of world merchandise exports touched $7.3

trillion, while that of commercial services trade rose to $1.8 trillion.

Thus, the daily volume of transactions in foreign exchange markets exceeded

the annual value of trade in commercial services and was in excess of

one quarter of the annual merchandise trade.

The trade in derivatives is also large and significant. The Triennial

Survey indicates that the average daily volume of exchange traded derivatives

amounted to $4.5 trillion in 2004. In the OTC derivatives market, average

daily turnover amounted to $1.2 trillion at current exchange rates.

The OTC market section consists of ''non-traditional'' foreign exchange

derivatives - such as cross-currency swaps and options - and all interest

rate derivatives contracts. Thus total derivatives trading stood at

$5.7 trillion a day, which together with the $1.9 million daily turnover

in foreign exchange markets adds up to $7.6 trillion. This exceeds the

annual value of global merchandise exports in 2003.

One consequence of these developments was that the flow of capital to

developing countries, particularly the ''emerging markets'' among them

had nothing to do with their financing requirements. Capital in the

form of debt and equity investments began to flow into these countries,

especially those that were quick to liberalize rules relating to cross-border

capital flows and regulations governing the conversion of domestic into

foreign currency. The point to note is that these inflows did not spur

substantial productive investment in these countries. Even foreign direct

investment, defined as investment in firms where the foreign investor

holds 10 per cent or more of equity, had ''portfolio'' characteristics,

and often took the form of acquisitions rather than greenfield investment.

What is important from the point of view of global balances is that

the inflow of such capital imposes a deflationary environment on developing

countries, because one requirement for keeping financial investors happy

is to substantially reduce the deficit of the government or its expenditures

financed with borrowing. Financial interests are against deficit-financed

spending by the State for a number of reasons. To start with, deficit

financing is seen to increase the liquidity overhang in the system,

and therefore as being potentially inflationary. Inflation is anathema

to finance since it erodes the real value of financial assets. Second,

since government spending is ''autonomous'' in character, the use of

debt to finance such autonomous spending is seen as introducing into

financial markets an arbitrary player not driven by the profit motive,

whose activities can render interest rate differentials that determine

financial profits more unpredictable. Finally, if deficit spending leads

to a substantial build-up of the state’s debt and interest burden, it

may intervene in financial markets to lower interest rates with implications

for financial returns. Financial interests wanting to guard against

that possibility tend to oppose deficit spending. Given the consequent

dislike of expansionary fiscal policy on the part of financial investors,

countries seeking to attract financial flows or satisfy existing financial

investors are forced to adopt a deflationary fiscal stance, which limits

their policy option.

Part of the reason why developing countries record a surplus on their

current account is the deflationary fiscal stance adopted by their governments.

Growth is curtailed through deflation so that, even with a higher import-to-GDP

ratio resulting from trade liberalisation, imports are kept at levels

that imply a trade surplus. Consider the flows that deliver current

account surpluses for developing countries? As Table 1 shows, two factors

account for these surpluses: first, the transformation of the trade

deficit (goods and services) in these countries into surpluses, and

a substantial inflow of current transfers, mainly in the form of remittances.

So, unless exports of goods and services and/or remittances are large

and growing, deflation must be the factor influencing the current account.

Table

1: The Current Account of Developing and Emerging Market Countries ($ billion) |

||||||||

1996 |

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003 |

|

Current

account balance |

-86.1 |

-85.3 |

-116.3 |

-18.9 |

86.3 |

39.5 |

84.21 |

148.9 |

Balance

on goods and services |

-46.6 |

-45.6 |

-66.1 |

42.2 |

147.9 |

93.5 |

128.6 |

183.4 |

Income,

net |

-83.7 |

-91.8 |

-99.5 |

-114.3 |

-188.3 |

-116.9 |

-124.5 |

-137.3 |

Current

transfers, net |

44.2 |

52.1 |

49.2 |

53.2 |

56.7 |

63 |

80 |

102.7 |

In

sum, while the inflow of remittances is reflective of one aspect of

the process of globalisation that has benefited developing countries,

the rise of trade surpluses reflect the deflation imposed by financial

flows and the financial crises they engineer in some countries. As a

result, developing countries as a group did not require capital inflows

to finance their balance of payments. But such inflows did occur, particularly

in the form of private foreign investment. Such capital inflows then

either went out as other net investment or were accumulated as reserves

that were invested in large measure in US Treasury bills. That is, private

capital flowed into developing countries to earn lucrative returns,

and this capital then flowed out as investment in low interest Treasury

bills in order to finance the US balance of trade deficit.

What is more, if a country is successful in attracting financial flows,

the consequent tendency for its currency to appreciate forces the central

bank to intervene in currency markets to purchase foreign currency and

prevent excessive appreciation. The consequent build-up of foreign currency

assets, while initially sterilized through sale of domestic assets,

especially government securities, soon reduces the monetary policy flexibility

of the central bank. Governments in Asia, especially India, faced with

these conditions are increasingly resorting to trade and capital account

liberalization to expend foreign currency and reduce the compulsion

on the central bank to keep building foreign reserves. That is, if financial

liberalisation is successful, in the first instance, in attracting capital

flows, it inevitably triggers further liberalization, including of capital

outflows, leading to an increase in financial fragility.

Thus, financial liberalisation that successfully attracts capital flows

increases vulnerability and limits the policy space of the government.

Unfortunately, the dominance of finance globally has meant that such

debilitating flows occur even when individual developing countries or

developing countries as a group have no need for such flows to finance

their balance of payments or augment their savings. The real benefit

of such flows is derived by the US government, which, being the home

of the reserve currency can resort to large scale deficit financing

which it opposes in developing countries. The resulting balance of trade

and current account deficits are not a problem because they are financed

with capital flows from the rest of the world including ''emerging market''

developing countries. The problem now is that the willingness of private

investors and governments to hold more dollar denominated assets is

waning. If that continues a crisis at the metropolitan centre of global

capitalism is a possibility.