Revisiting Capital Flows*

A

striking feature of the recent global financial crisis and its aftermath

is the behaviour of private international capital flows, especially

to emerging markets. Prior to the crisis, in the years after 2003, a

number of analysts had noted that the world was witnessing a surge in

capital flows to emerging markets. These flows, relative to GDP, were

comparable in magnitude to levels recorded in the period immediately

preceding the financial crisis in Southeast Asia in 1997. They were

also focused on a few developing countries, which were facing difficulties

managing these flows so as to stabilise exchange rates and retain control

over monetary policy. They also included a significant volume of debt-creating

flows, besides other forms of portfolio flows.

Interestingly, these developments did not, as in 1997, lead up to widespread

financial and currency crisis originating in emerging markets, as happened

in 1997. However, the risks involved in attracting these kinds of flows

were reflected in the way the financial crisis of 2008 in the developed

countries affected emerging markets. Financial firms from the developed

world, incurring huge losses during the crisis in their countries of

origin, chose to book profits and exit from the emerging markets, in

order to cover losses and/or meet commitments at home. In the event,

the crisis led to a transition from a situation of large inflows to

emerging markets to one of large outflows, reducing reserves, adversely

affecting currency values and creating in some contexts a liquidity

crunch.

Given the legacy of inflows and the consequent reserve accumulation,

this, however, was to be expected. What has been surprising is the speed

with which this scenario once again transformed itself, with developing

countries very quickly finding themselves the target of capital inflows

of magnitudes that are quickly approaching those observed during the

capital surge. As the IMF noted in the latest (April 2011) edition of

its World Economic Outlook: ''For many EMEs, net flows in the first

three quarters of 2010 had already outstripped the averages reached

during 2004–07,'' though they were still below their pre-crisis highs.

One implication of the quick restoration of the capital inflow surge

is the fact that, in the medium-term, net capital inflows into developing

countries in general, and emerging markets in particular, has become

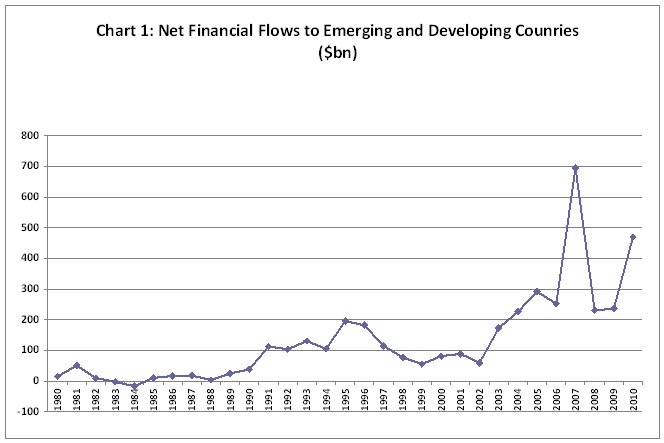

much more volatile. As Chart 1 shows, net capital flows which were small

though the 1980s, rose significantly during 1991-96, only to decline

after the 1997 crisis to touch close to early-1990s levels by the end

of the decade. But the amplitude of these fluctuations in capital inflows

was small when compared with what has followed since, with the surge

between 2002 and 2007 being substantially greater, the collapse in 2008

much sharper and the recovery in 2010 much quicker and stronger.

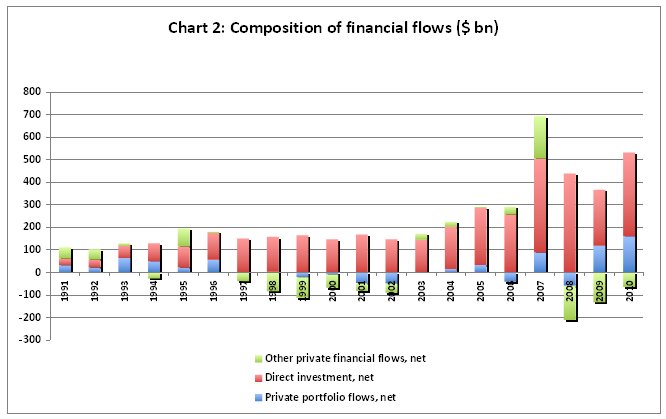

When

we examine the composition of flows we find that volatility is substantial

in two kinds of capital flows: ''private portfolio flows'' and ''other

private'' flows, with the latter including debt (Chart 2). There has

been much less volatility in the case of direct investment flows. However,

in recent years the size of non-direct investment flows has been substantial

enough to provide much cause for concern. Further, besides the fact

that direct investment flows are differentially distributed across countries

(with China taking a large share), the definition of direct investment

is such that the figure includes a large chunk of portfolio flows. The

magnitude of the problem is, therefore, still large.

Does this increase in volatility during the decade of the 2000s speak

of changes in the factors driving and motivating capital flows to emerging

markets? The IMF in its World Economic Outlook does seem to think so,

though the argument is not formulated explicitly. In its analysis of

long-term trends in capital flows the IMF does link the volatility in

flows to the role of monetary conditions (and by implication monetary

policy) in the developed countries, especially the US, in influencing

those flows.

As the WEO puts it, ''Historically, net flows to EMEs have tended to

be higher under low global interest rates, (and) low global risk aversion,''

though this assessment is tempered with references to the importance

of domestic factors. Shorn of jargon, there appears to be two arguments

being advanced here. The first is that capital flows to emerging markets

are largely influenced by factors from the supply-side, facilitated

no doubt by easy entry conditions into these economies resulting from

financial liberalisation. The second is that easy monetary policies

in the developed countries has encouraged and driven capital flows to

developing countries. This is because easy and larger access to liquidity

encourages investment abroad, while lower interest rates promote the

''carry-trade'', where investors borrow in dollars to invest in emerging

markets and earn higher financial returns, based on the expectation

that exchange rate changes would not reduce or neutralise the differential

in returns. Needless to say, when monetary policy in the developed countries

is tightened, the differential falls and capital flows can slow down

and even reverse themselves.

The evidence clearly supports such a view. The period of the capital

surge prior to 2007 was one where the Federal Reserve in the US, for

example, adopted an easy money policy, involving large infusion of liquidity

and low interest rates. While this was aimed at spurring credit-financed

domestic demand, especially for housing, so as to sustain growth, it

also encouraged financial firms to invest in lucrative markets abroad.

Flows reversed themselves when the losses and the uncertainty resulting

from the sub-prime crisis and its aftermath resulted in a credit crunch.

Finally, flows resumed and rose sharply when the US government responded

to the crisis with huge infusions of cheap liquidity into the system,

aimed at relaxing the liquidity crunch. A substantial part of the so-called

stimulus consisted of periodic resort to ''quantitative easing'' or

the loosening of monetary controls.

This close link between monetary policy in the developed countries and

capital flows to emerging markets is of particular significance because,

with the turn to fiscal conservatism, the monetary lever has become

the principal instrument for macroeconomic management. Since that lever

can be moved in either direction (monetary easing or stringency), net

flows can move either into or out of emerging markets. As a corollary,

the consequence of monetary policy being in ascendance is a high degree

of volatility and lowered persistence of capital inflows to these countries.

From the point of view of developing countries the implications are

indeed grave. When global conditions are favourable for an inflow of

capital to the developing countries, these countries experience a capital

surge. This creates problems for the simultaneous management of the

exchange rate and monetary policy in these countries, and leads to the

costly accumulation of excess of foreign exchange reserves. Costly because

the return earned from investing accumulated reserves is a fraction

of that earned by investors who bring this capital to the developing

economy. Moreover, when global conditions turn unfavourable for capital

flows, capital flows out, reserves are quickly depleted and there is

much uncertainty in currency and financial markets.

The problem is particularly acute for countries that are more integrated

with US financial markets, since dependence on the monetary level is

far greater in that country, partly because of the advantages derived

from the dollar being the world's reserve currency. The IMF's WEO, therefore,

predicts: ''economies with greater direct financial exposure to the

United States will experience greater additional declines in net flows

because of U.S. monetary tightening, compared with economies with lesser

U.S. financial exposure.'' This tallies with the evidence. Overall,

''event studies demonstrate an inverted V-shaped pattern of net capital

flows to EMEs around events outside the policymakers' control, underscoring

the fickle nature of capital flows from the perspective of the recipient

economy.''

This increase in externally driven vulnerability explains the IMF's

recent rethink on the use of capital controls by developing countries.

Having strongly dissuaded countries from opting for such controls in

the past, the IMF now seems to have veered around to the view that they

may not be all bad. However, its endorsement of such measures has been

grudging and partial. In a report prepared in the run up to this year's

spring meetings of the Fund and the World Bank, the IMF makes a case

for what it terms capital flow management measures, but recommends them

as a last resort and as temporary measures, to be adopted only when

a country has accumulated sufficient reserves and experienced currency

appreciation, despite having experimented with interest rate policies.

This may be too little, too late. But, fortunately, many developing

countries have gone much further. Only a few like India, which is also

the target of a capital surge, seem still ideologically disinclined.

*

This article was originally published in The Businessline, 3 May, 2011.