Clearly,

we are back in another phase of sharply rising global

food prices, which is wreaking further devastation

on populations in developing countries that have already

been ravaged by several years of rising prices and

falling employment chances. The food

price index of the FAO in December

2010 surpassed its previous peak of June 2008, the

month that is still thought of as the extreme peak

of the world food crisis.

Some of the biggest increases have come in the prices

of sugar and edible oils. But even staple prices have

shown sharp increases, with the biggest increase in

wheat prices, which doubled in the second half of

2010 and have been increasing since then. Rice prices

have been relatively stable in global trade over the

past year in comparison, but are still much higher

(by around 48 per cent) than they were at the start

of 2008.

Of course this need not (and should not) translate

directly into prices faced by consumers in poor developing

countries. Certainly, given the much lower per capita

incomes in such countries and therefore lower purchasing

power of the people, it should be expected that there

would be some public mediation of the relationship

between global prices and domestic food prices. This

is all the more desirable, if not essential, in periods

of high price volatility in global trade, such as

has been observed in the past four years. Otherwise,

poor consumers in the developing world for whom basic

food grains still accounts for around 40-50 per cent

of the consumption basket, would be sharply affected

by such price movements.

As it happens, the period of dramatic increases in

price volatility in global markets has also been one

in which there has been very high transmission of

international price changes to domestic prices in

many developing countries. This is evident from a

quick perusal of retail price changes in wheat and

rice markets in some developing countries.

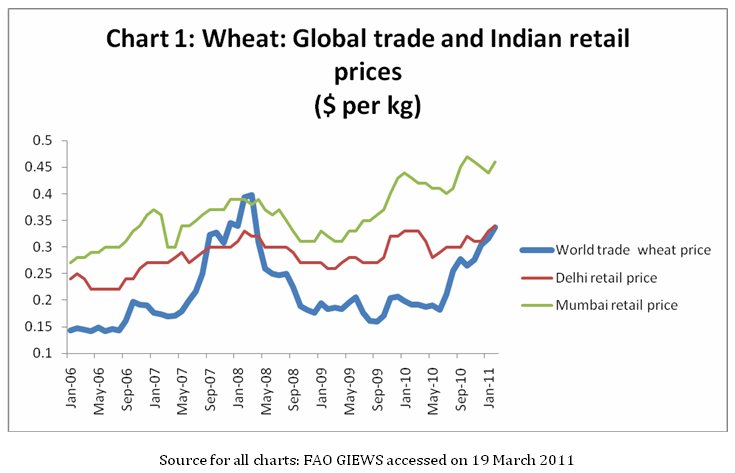

Consider India, a country which currently has the

largest number of hungry people in the world and very

poor nutrition indicators in general, despite nearly

two decades of rapid income growth. Chart 1 shows

the behaviour of retail wheat prices in two major

cities – Delhi and Mumbai – in relation to the global

trade price of wheat (relating to US wheat in the

Chicago Board of Trade).

Chart

1 >> Click

to Enlarge

Two

important features are immediately evident from this

chart. First, the substantial variation in retail

prices across the two Indian cities (which would be

reinforced by other data showing the variation in

retail prices across other towns and cities), which

suggests that there is still absence of a national

market for essential food items, even those that can

be transported and stored easily. Second, the degree

to which price changes, have tracked international

prices.

Many analysts have argued that the Indian food grain

market is insulated from the international market

because of the system of domestic public food procurement

and distribution. Indeed, until the early part of

the last decade, this has been generally true. However,

the opening of agricultural items to international

trade without quantitative restrictions has clearly

allowed for greater impact of global prices on domestic

prices.

Further, the public distribution system itself has

been increasingly run down in the past two decades.

Recently, this has been further complicated by the

insistence of the central government on raising procurement

prices and procuring more, but not distributing the

increased procurement to states to allow them to provide

wheat to the defined “non-poor” population in a manner

that would restrain prices. Instead, the focus has

been on building central stocks, which has even turned

out to be somewhat counterproductive because of the

lack of adequate storage facilities. As a result,

Indian retail wheat prices have been higher than global

prices in both these urban centres. They rose by about

30 per cent in the year to October 2010 as global

prices also increased.

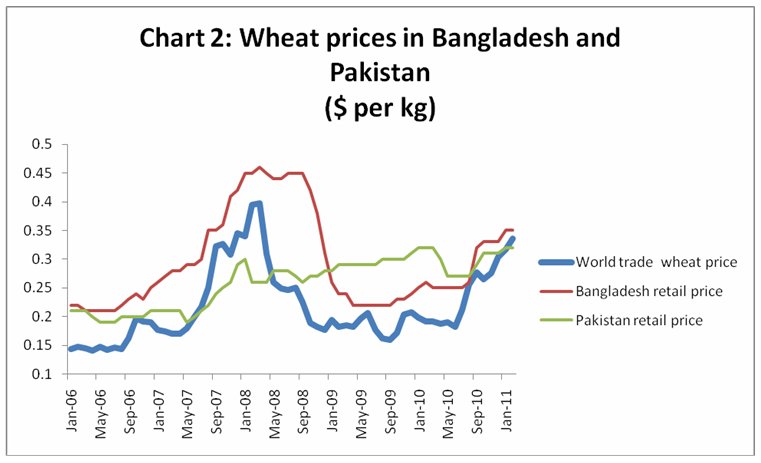

Chart 2 describes the behaviour of wheat retail prices

in two other South Asian countries – one a domestic

producer and occasional exporter of wheat (Pakistan)

and the other an importer in which wheat is still

important in fulfilling dietary needs (Bangladesh).

Chart

2 >> Click

to Enlarge

Bangaldeshi retail prices have closely tracked global

trade prices, always remaining higher. This in itself

is significant given the low purchasing power of most

Bangaldeshi consumers. It indicates that there is

little to no mediation between import prices and prices

faced by consumers in Bangaldesh, and that the latter

are subject to the fierce fluctuations and rising

tendencies that have characterised the global market.

What is surprising is that the same is broadly true

of Pakistan (the retail price here relates to Lahore

city). What is of interest in this case is that while

periods of rising prices appear to be marked by rapid

transmission to Lahore retail prices, the period of

global price reduction shows no such tendency. In

fact, Lahore retail prices kept rising even as global

prices came down, such that even after the latest

global price surge, global prices are still at around

the same level as the Pakistan retail price.

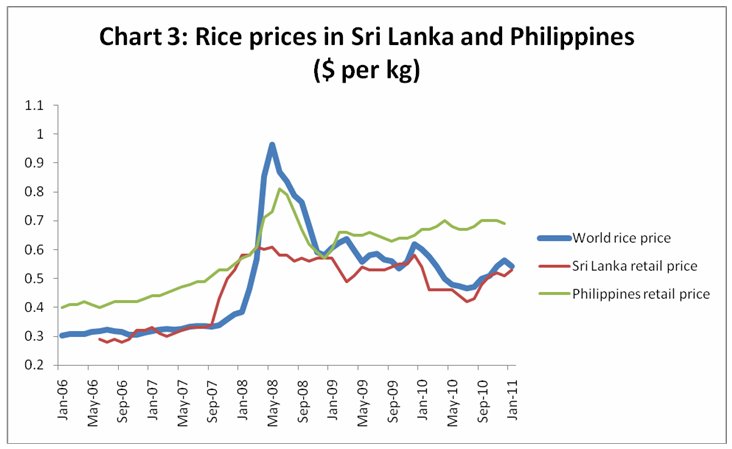

The food grain commodity that is the most important

for most Asian consumers is rice, which remains the

grain that is dominantly consumed by large parts of

the population in most of the region. Chart 3 indicates

the behaviour of rice prices in Sri Lanka and the

Philippines, in relation to the global price.

Chart

3 >> Click

to Enlarge

Note that the two are rather diffferent countries:

while Sri Lanka exports cash crops, it is close to

self-sufficient in rice in recent times, thanks to

major efforts to promote domestic rice cultivation.

Rice is of course by far the dominant food crop, accounting

for around 60 per cent of dietary requirements. The

Philippines, on the other hand, is a rice producer

but also depends on imports for between 15 and 20

per cent of domestic consumption, so it is likely

to be far more affected by international prices. Rice

accounts for around 46 per cent of dietary requirements.

Retail rice prices in Sri Lanka (referring to Colombo

in this chart) very closely track international prices.

Other than the extreme peak of June 2008, retail prices

have been close to global trade prices, despite the

lack of reliance on imports. So the global price volatility

has been reflected even in a country that is largely

self-sufficient in rice. In the Philippines, the story

is even more worrying. Rice prices (referring here

to retail prices in Metro Manila) rose dramatically

in response to global price movements, almost to the

same level as the peak in June 2008; came down as

global prices fell in the second half of 2008, but

since then have actually been higher in the Philippines

than in international trade. Further they have continued

to rise even as rice prices have stabilised in the

global market.

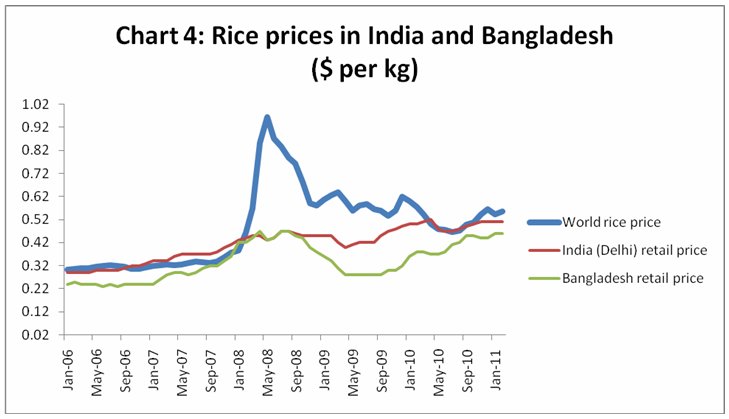

Chart 4 describes retail price movements in India

(Delhi) and Bangladesh (national average). It is worth

remembering the retail prices vary quite significantly

across towns and cities in India; even so this provides

an important indication of recent patterns.

Chart

4 >> Click

to Enlarge

According to FAO data, India is completely self-sufficient

in rice whereas Bangladesh currently is only 97 per

cent sufficient, importing around 3 per cent of its

requirement (possibly more if the cross-border smuggling

is taken into account). While retail rice prices did

not peak in June 2008, they have risen steadily in

India and increased by around 26 per cent in the second

half of 2010 alone. In Bangladesh there has been much

greater volatility, with prices rising sharply following

the global surge in 2007-08, then falling and then

rising again. In the past two years retail rice prices

in Bangladesh have increased by more than 35 per cent.

These trends in different Asian countries point to

a broader trend whereby prices in domestic food markets

are more and more strongly affected by and related

to international price changes. This is a matter of

some concern, especially in the context of the ongoing

extreme volatility in global prices.

The recent price increases, just as those in 2007-08

(which were followed by declines) do not represent

significant changes in global demand and supply balances.

Rather, once again, it is likely that a combination

of panic buying and speculative financial activity

is playing a role in driving world food prices up

well beyond anything that is warranted by real quantity

movements. The most recent data on financial activity

in commodity futures markets from the US Commodity

Future Trading Commission suggest that until the end

of January the net long positions of index investors

had increased dramatically in commodities like wheat

and corn. This is likely to have increased even more

in the past few weeks, given the announcements about

lower levels of public stocks.

Once again we are also seeing contango in these commodity

markets, with futures prices higher than spot prices.

This is all a repeat of 2007 and the first half of

2008, when prices of these commodities nearly tripled.

And it is not surprising, because the regulations

that could prevent or at least limit such speculative

financial activity are not yet in place, and there

are even concerns about whether they will be effective

or toothless in the implementation.

We now have direct recent experience of how financial

speculation in commodity markets can create not only

unprecedented volatility, but also affect prices in

developing countries with extreme effects on hunger

and nutrition for at least half of humanity. The case

for moving swiftly to ensure effective regulation

in this area – and for dealing with supply issues

in a serious and sustainable way - has never been

more compelling.