Early in May this year, India's central bank, the

Reserve Bank of India, issued an unusual set of guidelines

for foreign banks operating in the country. The notification

stated: ''It has been decided that for all foreign

banks operating in India, the CEO (chief executive

officer) will be responsible for effective oversight

of regulatory and statutory compliance as also the

audit process and the compliance thereof in respect

of all operations in India.''

For those accustomed to normal principles of corporate

governance, this official notification must come as

a surprise. Who other than the CEO of a company would

be finally responsible for compliance? The RBI, however,

had a reason to state the obvious, based on allegations

of fraud in branches of banks such as Citibank and

Standard Chartered Bank. ''It is observed,'' it noted,

''that Indian operators of foreign banks functioning

in India as branches of the parent banks generally

do not have a separate audit committee vested with

the responsibility of examining and reviewing inspection/audit

reports for their compliance.'' As a result in its

view, ''In the recent past there have been concerns

about the adequacy of regulatory compliance by foreign

banks in India and it is felt that this is on account

of business heads and units reporting directly to

their ‘functional heads' located overseas and not

to the CEO of Indian operations.''

To deal with this, the RBI is also contemplating institutional

requirements that would improve regulatory oversight.

As opposed to allowing foreign banks to function through

''branches'' of units registered abroad, it is expected

to soon require foreign banks to operate in India

through wholly owned subsidiaries registered in the

country. This would make the bank's Indian operation

an Indian entity and facilitate regulation.

The problem is not restricted to India. Indonesia

has experienced a recent instance of fraud in which

a relationship manger allegedly spirited $2 million

from the accounts of customers. In response, the Indonesian

central bank has banned Citibank from canvassing new

premium customers for a year.

These instances point to a much deeper problem that

emerging markets face when dealing with foreign banks,

whose presence in their economies is increasing. During

what is considered the ''second wave'' of global financial

integration since the 1960s (with the first dated

between 1890 and 1930), the relationship between international

banks and developing countries took two forms. The

first was the acquisition of international claims

by the banking system in emerging markets, involving

cross-border flows of capital to both public and private

sector targets. The second was an expansion of the

host country presence of international banks in emerging

markets, increasing deposit mobilisation and lending

by local subsidiaries in local currencies.

However, as the Committee on the Global financial

System (CGFS) noted in a 2010 report, the history

of international banking even in the period after

the 1960s has seen some kind of a sructural shift.

During the first two and a half decades starting in

the 1960s, international banking transactions were

largely between the developed countries. In the period

from the mid-1980s to the present, however, there

has been an increasing emphasis on the creation of

branches and subsidiaries in developing countries,

with focus on the retail business.

There are a number of noteworthy features of this

recent period. The first was an initial increase and

subsequent acceleration of international bank lending

in developing countries. Taking the cross-border claims

and local claims of foreign banks in both foreign

and local currencies together, the ratio of international

bank lending to developing countries rose gradually

at around 4 per cent per annum between the 1980s and

the early 2000s, and then accelerated to touch almost

double its 2002 value by the time of the financial

crisis of 2008. Second, while there was a close relation

between the ratio of international trade to GDP and

the international claims of banks relative to GDP

till the end of the last century, subsequently there

has been a sharp divergence with bank claims racing

ahead of trade. If trade had led or, at least, significantly

influenced financial flows earlier, that seems to

be much less true more recently. Finally, there is

other evidence that the activity of financial capital

had acquired a degree of independence with a weakening

of its reationship with trends in the real economy.

Principal among these was the emergence and growth

of securities and derivatives markets, leading to

a substantial lengthening of intermediation chains

and the emergence of new institutions and instruments.

Overall, even though the exposure of international

banks in developing countries is only a fifth of that

in the developed, that exposure has in recent years

reportely traversed from a relative flat trajectory

to a steeply rising one.

Associated with this growing exposure of foreign banks

in developing countries has been a significant increase

in their physical presence. According to an earlier

(2004) study by the CGFS, there has been a surge in

foreign direct investment in the financial sectors

of developing countries. The study, by examining cross-border

M&As targeting banks in emerging market economies

(EMEs), found that cross-border deals involving financial

institutions from EMEs as targets, which accounted

for 18 per cent of such M&A deals worldwide during

1990-96, rose to 30 per cent during 1997-2000. The

value of financial sector FDI rose from about $6 billion

during 1990-96 to $50 billion during the next four

years. Such FDI peaked at $20 billion in 2001, declined

sharply in 2002, but stabilized in 2003. The net result

is a clear shift in the ownership of the financial

sector. More recent evidence indicates that this figure

has risen sharply since.

It is indeed true that the M&A drive, involving

the acquisition of banks in emerging markets by financial

firms from the developed countries has been concentrated

in two regions: Eastern Europe and Latin America,

with some countries such as Slovak Republic1

and Mexico being the focus. However, there is evidence

that even Asia, where thus far the absolute share

in banking assets of foreign firms is low, has been

experiencing an increase in foreign presence especially

after the 1997 crisis.

With respect to Asia, the CGFS found that: ''The proportion

of cross-border M&As in East Asia's financial

sector initially was small compared with other regions.

The value of cross-border M&As targeting non-Japan

Asian countries was $14 billion or 17 per cent of

the total during 1990-2003. Asia, however, has been

one of the fastest growing target regions for M&A,

with a sizeable jump in cross-border M&A activity

occurring in Korea and Thailand. In addition, there

has been a large number of small-value cross-border

M&A transactions in the finance sector between

East Asian economies. In 2003, Asia received the largest

share of FSFDI inflows.''

Among the many reasons cited as explaining the desire

of banks to establish a physical presence in emerging

markets to expand their business, three are of particular

relevance. These are: (i) a combination of increased

competition and saturating business opportunities

at home; (ii) increased access to enhanced liquidity

at low interest rates as a result of monetary easing;

and (iii) greater liberalisation, better profit conditions

and improved security in EMEs. These are important

because they point to the role of supply side decisions

in driving foreign bank expansion and presence in

emerging markets.

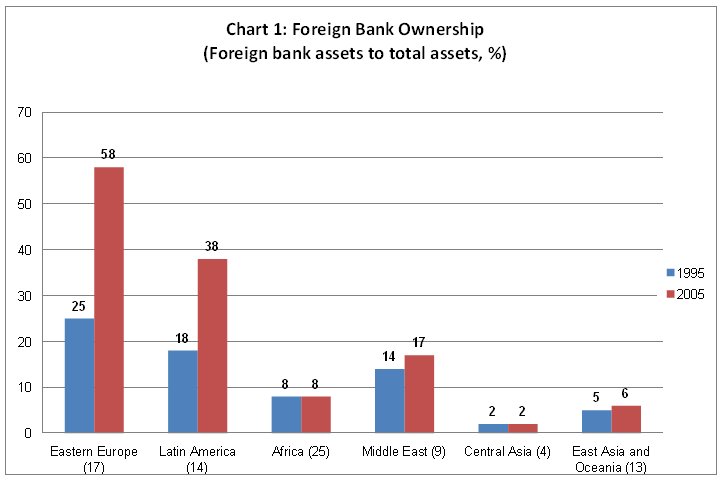

As a result of these processes, an IMF study found,

between 1995 and 2005, the share of foreign banks

in total bank assets rose from 25 to 58 per cent in

Eastern Europe and from 18 to 38 per cent in Latin

America, though even by that date the increase in

East Asia and Oceania was much less (from 5 to 6 per

cent) (Chart 1). However, as noted above, it is likely

that the trend would have been visible in Asia as

well more recently.

Chart

1 >> Click

to Enlarge

Not surprisingly, with this increase in presence,

the share of foreign banks in lending to non-bank

residents has been rising. From the mid-1990s (and

by 2009) the share of foreign banks in credit to non-bank

residents rose from 30 to 50 per cent in Latin America,

to nearly 90 per cent in emerging Europe, but is still

at about 20 per cent in emerging Asia.

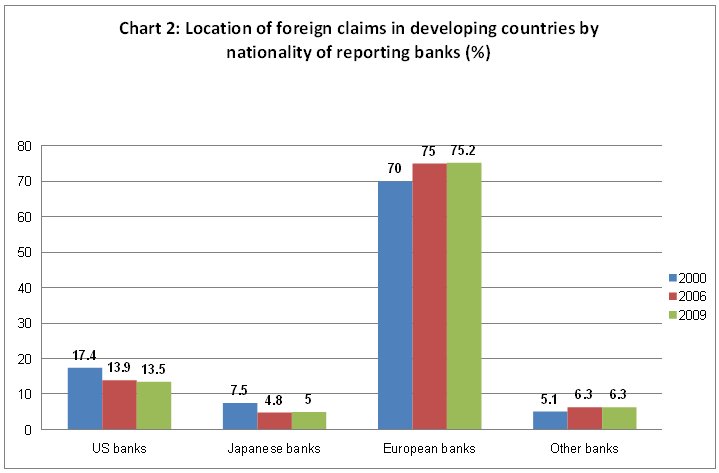

A second feature of the recent focus on emerging markets

is that the international banks involved are predominantly

European. Around three fourths of foreign claims in

developing countries is on account of European Banks

(Chart 2). Part of the reason is that mid-sized European

banks faced with increased competition at home are

now seeking out developing countries to expand business

and sustain profitability.

A third feature is that in their lending banks are

no more targeting either governments or international

corporations investing in developing countries. Rather

their focus is increasingly on retail lending, in

the form of housing-related and other personal lending.

As a result, the share of non-bank private sector

borrowers in the portfolio of foreign banks has grown

from about 25 per cent to more than 60 per cent of

claims over the 1985-2009 period. Public sector borrowers

now account for only 15 per cent of total international

claims on developing countries, ac compared with more

than 40 per cent two decades ago.

Finally, the increased presence of these foreign banks

has been accompanied by a substantial increase in

their activity in wholesale markets, including securities

and derivatives markets.

Chart

2 >> Click

to Enlarge

Thus, financial integration results in a supply-side

push of international banks into developing countries

in two senses. It involves, as in the past, an increase

in capital flows into developing countries, which

is determined by liquidity and structural conditions

in the developed countries. It also involves the creation

of branches and subsidiaries of foreign firms in developing

countries, to expand business beyond what can be undertaken

only with capital from the home country. One implication

of these developments is that the presence of these

institutions imports into the ''emerging markets''

the practices and instruments associated with the

process of financial innovation in developed countries

since the mid-1980s. Local institutions too begin

to adopt these practices and stay with them even when

events such as the recent financial crisis suggest

that they render the system fragile and crisis-prone.

This obviously means that the regulation in developing

countries must either be geared to limiting foreign

presence in their banking sectors or dealing with

new institutions, instruments and practices. The recent

moves of the Indian government indicate that while

it has chosen to relax restraints to foreign entry,

it is yet to devise an adequate regulatory frame to

deal with the resulting brave new world.

1

Between

1995 and 2002, the Slovak Republic witnessed an increase

in the share of assets held by foreign banks from

9 to almost 82 percent. In Mexico, the share of assets

held by foreign banks increased from 2.31 percent

in 1995 to 61.9 per cent in 2002 (Cull and Peria 2007).

*

This article was originally published in The Business

Line, 31st May 2011.