The Signs of a Global Recovery

Finance

Ministers of the G8 meeting at Lecce in Italy during the latter part

of week ending June 14, were cautiously optimistic. The final communiqué

noted that in the aftermath of efforts at financial stabilisation and

fiscal stimulation ''there are signs of stabilization in our economies,

including a recovery of stock markets, a decline in interest rate spreads,

(and) improved business and consumer confidence''. But, the ministers

cautioned ''the situation remains uncertain and significant risks remain

to economic and financial stability''.

There were two elements of the communiqué that pointed to a compromise

between the differing perceptions of the US and UK, on the one hand,

and Germany and France, on the other, regarding the principal problems

and tasks at hand. The first of these elements was the reference to

the persistence of ''significant risks'' which was not there in the

original draft of the communiqué, and was ostensibly inserted

by those countries (UK and US) who feel that it is not yet time to decide

that the recovery is here and the stimulus provided thus far has been

adequate. Moreover, the mention of ''encouraging figures in the manufacturing

sector'' that figured in the draft was dropped, since it went against

the evidence that industrial production in the eurozone area had fallen

by 21 per cent in April, relative to the corresponding month of the

previous year.

The second element of the communiqué of interest is that it pushes

for going beyond thinking of recovery and formulating national level

''exit strategies'' ''for unwinding the extraordinary policy measures

taken to respond to the crisis.'' The reference here is to the huge

budget deficits and high levels of public debt that many countries,

especially the US, have accumulated in the wake of the bail-outs and

the stimulus packages they have been put in place. Though the US and

UK have played down this aspect of the discussions, there is clearly

a difference in emphasis among the leading powers on where the world

economy stands and what is the immediate priority in terms of action.

The difference hinges, quite clearly, on the extent to which different

sections believe that the worst is over. The reason for uncertainty

regarding a potential recovery is that the figures are yet to point

to a definitive revival. As of May 2009, nearly two years since the

financial crisis broke and a year-and-a-half after the onset of the

global recession, the economic scenario remains uncertain, if not bleak.

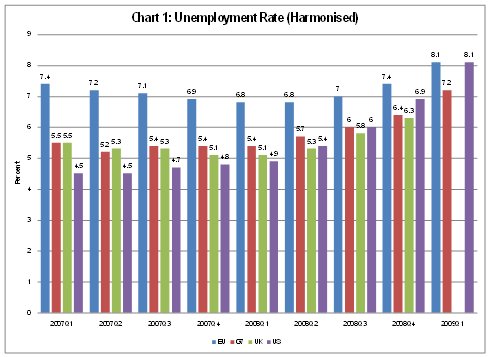

The rate of unemployment in the US, which stood at less than 5 per cent

in the first quarter of 2008, had risen to 8.1 per cent in the first

quarter of 2009 (Chart 1) and is estimated to have touched 9.4 per cent

in May 2009—its highest rate for the last 26 years. This possibly explains

US pessimism. It is true that the unemployment rate in the European

Union had also risen from 6.8 to 8.1 per cent between the first quarters

of 2008 and 2009. But the higher base level may be making the problem

appear less alarming to ruling governments there than in the US, influencing

their perceptions.

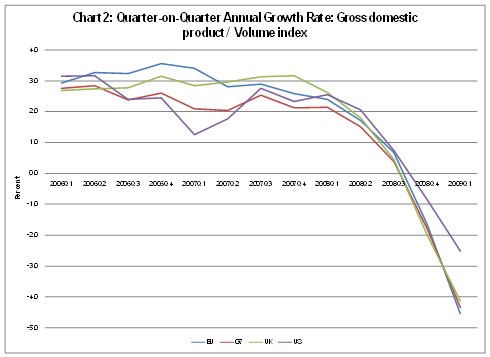

Output growth too gives no cause for optimism. Quarter-on-quarter growth

rates of US GDP (as measured relative to the corresponding quarter of

the previous year) had declined sharply in the last quarter of 2008

and first quarter of 2009 across the G7. This decline was even sharper

in the UK and the EU, than the US (Chart 2). The crisis had clearly

not gone away by the beginning of April, despite signs of recovery in

the stock market. The disconcerting element is that this situation prevails

despite huge infusion of funds by G7 governments. According to one estimate,

the US Federal Reserve had by April 2009 offered about $12.7 trillion

in guarantees and commitments to the US financial sector, and spent

a little over $4 trillion in combating the crisis. As a result the federal

deficit has risen to more than 12 per cent of GDP, frightening fiscal

conservatives who predict the onset of stagflation. The big thrust seems

to be over and the recovery is still not in sight. What it has possibly

done, and even that is not certain, is prevent the recession from turning

into a depression.

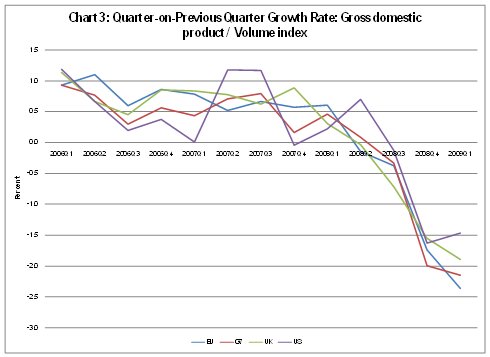

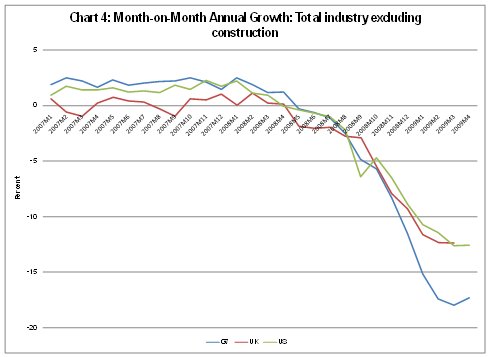

The third potential cause for comfort is the sign that relative to previous months, the decline in production is slowing. As Chart 3 shows, the decline in GDP relative to the immediately preceding quarter, which was rising till the first quarter of 2009, seems to have bottomed out in the US and to a lesser extent in the EU. What is more, this trend seems to be reflected even in the month-on-month annual growth rates of industrial production, with the rate of decline in April 2009 relative to the corresponding month of the previous year showing signs of reversing its hitherto continuous increase in the US, UK and EU (Chart 4).

Further, it is unclear whether there would be adequate alternative stimuli to sustain the recovery when the effects of the already implemented fiscal stimulus wane. Governments could hold back on providing any fresh stimulus because of arguments of the kind espoused by conservative economists, representatives of the financial sector and even some European governments, which emphasise the dangers of inflation. If that happens, recovery would depend on the return of the consumer to the market.

But here too the prognosis is not all too happy. Fears generated by the recession and rising unemployment and the increased desire to save to make up for the decline in the values of accumulated housing and financial assets is encouraging savings even in the US. According to a recent estimate of the Federal Reserve, the net worth of US households had fallen 2.5 per cent or by $1,300 billion in just the first three months of 2009. This comes on top of the 18 per cent fall in the previous year which was the worst since the Fed began estimating household wealth in 1946. The net result is that household savings rates in the US are rising and consumer spending was falling in March and April this year.

In the event many still remain sceptical. The Financial Times quotes Martin Feldstein as saying that ''it is possible but unlikely'' that the recession is over. ''I think it is a more likely scenario that we are seeing the favourable effects of the fiscal stimulus,'' he reportedly said. ''That, for a while, will offset the general diminished trend we have seen over the past two quarters, but it is a one-shot thing.'' Put otherwise, there could be more bad news ahead.