Fiscal Policy and Global Growth

Barely

three years since the Great Recession first affected the world economy,

the focus of global attention has shifted from the crisis and its origins

to the legacy left by the stimulus measures adopted by governments in

response to it. While this may be warranted by the sheer passage of

time, it does injustice to the facts that not all governments opted

for a significant, let alone adequate, fiscal stimulus in response to

the crisis; that not all of the accumulated fiscal deficits are attributable

to voluntary measures. Indeed, some deficits could be the result of

the crisis itself because of the need for large public spending to bail

out banks and other companies and also inasmuch as output contraction

adversely affects public revenues. Before turning to austerity and fiscal

consolidation, therefore, governments may need to look at the evidence

on fiscal stimuli and their influence on growth a little more closely.

Unfortunately, as of now, comparable IMF data on the cash surplus/deficit

to GDP ratios for a large enough sample of countries is available only

till 2008. Since the crisis broke in the second half of 2008, for many

countries this was the year when the fiscal stimulus just kicked in,

with much of the stimulus spending occurring in 2009.

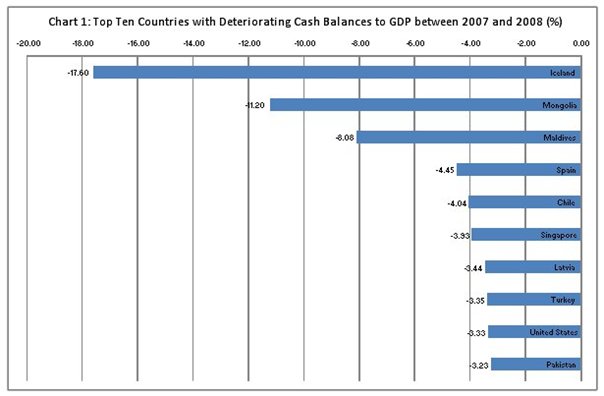

Even so, there are some messages that can be read from the available

evidence. Consider for example the cash balances (surpluses or deficits)

of governments defined as revenue (including grants) minus expense,

minus net acquisition of nonfinancial assets. Of the ten (of 69) countries

that recorded the largest decreases in their cash balance to GDP ratios

(Chart 1) between 2007 and 2008 (Iceland, Mongolia, Maldives, Spain,

Chile, Singapore, Latvia, Turkey, United States and Pakistan), only

Maldives, United States and Pakistan actually had a cash deficit in

2007, with the deficit to GDP ratio placed at 5.6, 2.2 and 4.2 per cent

respectively (Table 1). Iceland, Mongolia, Spain, Chile, Singapore Latvia

and Turkey had cash surpluses with the surplus to GDP ratios placed

at 4.82, 7.69, 2.44, 8.82, 12.05, 0.81 and 1.41 per cent respectively.

In the case of Maldives, the US and Pakistan their 2007 deficits widened

to 13.66, 5.54 and 7.41 per cent of GDP respectively in 2008. Iceland,

Mongolia, Spain, Latvia and Turkey saw their cash surpluses turning

to deficit to touch -12.78, -3.51, -2.01, -2.63 and -1.94 per cent of

GDP in 2008. Chile and Singapore, on the other hand maintained cash

surpluses, though at a lower level of 4.78 and 8.12 per cent of GDP

in 2008.

Some implications of this plethora of numbers relating to countries

that experienced the largest deterioration in their cash balance ratios

between 2007 and 2008 should be noted. To start with, only three of

these countries, namely Maldives, the United States and Pakistan can

at all be seen as countries that lacked the ''fiscal headroom'' in 2007

to adopt countercyclical fiscal policy measures in response to a recession.

With the others recording a surplus cash balance position in their government

accounts just before the crisis, they were in a position to respond

with fiscal measures, since pre-existing deficits had not made new debt

''unsustainable''. The countries that lacked the fiscal headroom did

end up recording significant deficits in 2008.

Secondly, three of the top four countries in terms of the deterioration

of fiscal balances between 2007 and 2008, were countries that had recorded

cash surpluses in 2007. Of these, only Iceland saw a significant deterioration

in its fiscal position with its deficit to GDP ratio rising to 12.8

per cent. Thirdly, of the top ten countries in terms of deterioration

of fiscal balances, only four (Iceland, Maldives, the US and Pakistan)

had cash deficit to GDP ratios in excess of 5 per cent in 2008. Two

(Chile and Singapore) in fact had surpluses, as noted above. Thus, at

least by 2008, the crisis had not resulted in any generalised tendency

towards substantial deterioration of fiscal balances.

Fourthly,

none of the top ten countries in terms of deterioration of fiscal balances,

except for Iceland, had recorded increases in expenditure to GDP ratios

in excess of 2.5 percentage points of GDP between 2007 and 2008. In

other words, at least in 2008, these were not the countries that had

resorted to huge fiscal stimuli. The country that saw an unusually high

increase in the expenditure to GDP ratio of 15 percentage points was

Iceland. This was also the country that had to put up a large amount

of money to cover the loans and deposits its banks had to repay when

the crisis rendered worthless the speculative investments they had made

using deposits and credit from abroad. That is, Iceland's fiscal situation

was not a reflection of its stimulus spending, but of the provisioning

needed to prevent a financial collapse.

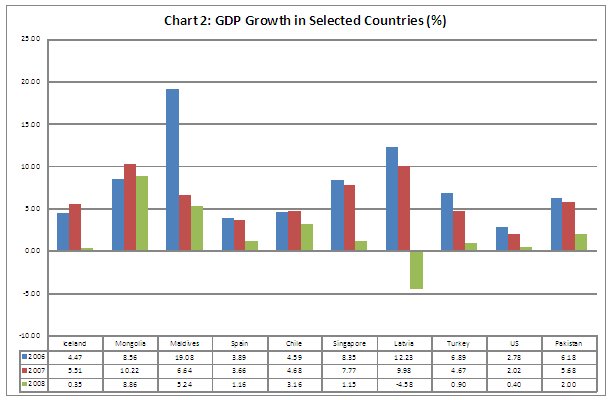

Finally, there is no clear relationship between the decline in the cash

balance to GDP ratio between 2007 and 2008 or the level of the cash

deficit to GDP ratio in 2008 and the relative GDP growth performance

of countries. Almost all countries (excepting for Mongolia) recorded

a significant decline in growth rates, with the extent of deterioration

in performance varying widely (Chart 2). This clearly was related to

the extent to which individual countries were affected by the financial

crisis per se and the manner in which individual countries are locked

into the global economy.

Table

1: Cash Surplus/Deficit to GDP Ratio by Year (%) |

||||||

2007 |

2008 |

|||||

| Iceland

|

4.82 |

-12.78

|

||||

| Mongolia

|

7.69 |

-3.51

|

||||

| Maldives

|

-5.58 |

-13.66

|

||||

| Spain

|

2.44 |

-2.01

|

||||

| Chile

|

8.82 |

4.78

|

||||

| Singapore

|

12.05 |

8.12

|

||||

| Latvia

|

0.81 |

-2.63

|

||||

| Turkey

|

1.41 |

-1.94

|

||||

| United States

|

-2.21 |

-5.54

|

||||

| Pakistan

|

-4.17 |

-7.41

|

||||

Thus, at least till 2008, there could be no clear link established between

the impact of the crisis in individual countries, the fiscal response

of governments to that crisis and the deterioration of the fiscal position

of countries. In fact, slower growth and the need to make large outlays

to salvage the financial sector rather than stimulus packages may have

been responsible for whatever deterioration in fiscal position occurred.

This would mean that the argument that the stimulus in response to the

crisis had gone too far, creating new problems attributable to fiscal

deterioration, and therefore needs to be corrected, is simply not valid

in most cases and only partially true in others.

The problem, however, is that 2008 was still an early point in the unfolding

of the crisis and the response to it and therefore analyses based on

data till that year may not be revealing the full picture.

There are, however, a few countries for which actual or provisionally

estimated numbers for 2009 are available from the IMF's government financial

statistics. Evidence from these 37 countries does seem to suggest that

there was further significant deterioration in the fiscal position of

many countries during the year 2009 with significantly higher declines

in the cash balance to GDP ratio between 2007 and 2009 and significantly

higher cash deficit to GDP ratios in 2009. However, what is noteworthy

is that this fiscal deterioration was accompanied by a substantial worsening

of the growth performance of many of these countries. This suggests

either that the fiscal deterioration was not reflective of an actual

stimulus that impacted positively on growth or that the stimulus was

inadequate given the gravity of the crisis in many countries or that

the deceleration in growth or intensification of recession affected

revenues adversely, thereby worsening the fiscal position of the countries

concerned.

Table

2: The Stimulus and Growth in 2009 |

||||||

Decline

in |

GDP |

GDP |

||||

| |

Cash

Balance to GDP |

Growth |

Growth |

|||

| |

2007

to 2009 |

2008 |

2009 |

|||

| |

(Percentage

pts) |

|||||

| Iceland

|

-15.5 |

12.9

|

1.5 |

|||

| Singapore

|

-13.7 |

3.0

|

-3.3 |

|||

| Chile

|

-13.5 |

3.9

|

2.7 |

|||

| Russian Federation

|

-10.4 |

24.6

|

-5.4 |

|||

| United States

|

-9.2 |

2.6

|

-1.3 |

|||

Consider, for example the five countries in the 2009 sample that recorded

the largest declines in their cash balance to GDP ratios between 2007

and 2009 (Table 2). All of them recorded negative cash balances (deficits)

relative to GDP in 2009. Yet every one of them recorded a substantial

deterioration in growth rates in 2009. This evidence, once again, points

in three possible directions. It could be that the deficit does not

represent a stimulus effort, but is the result of expenditure such as

bail-outs for bank that do not have much of an effect on demand and

production. Second, it may be the case that the crisis was so severe

that the component of increased expenditure that constituted a true

stimulus was inadequate to trigger a recovery. Or, third, it could be

that the impact of the crisis on growth was so adverse that the resulting

fall in government revenues substantially widened the cash deficit,

even when increases in stimulus spending were limited or non-existent.

If any of these holds then it is definitely not true that deficit spending

has been pushed far enough and that it is time to hold back on expansionary

spending.