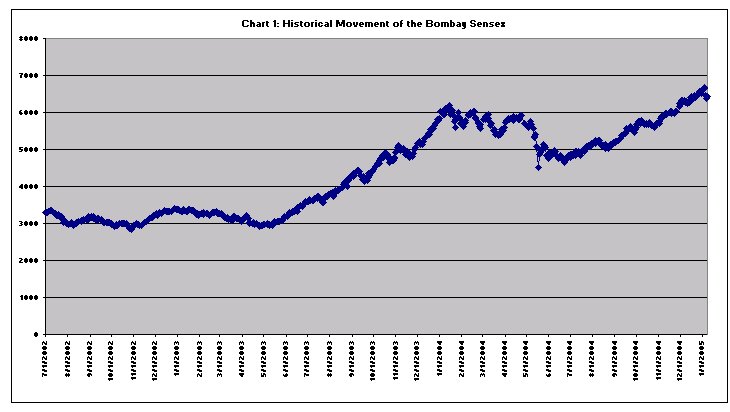

2004

was one more unusual year in India's stock markets.

It began with the Sensex still at a high and above

the 6000 mark. It witnessed a decline to a low in

mid-May of around 4500, delivered ultimately with

the market's single day loss of close to 565 points.

It then registered a recovery that turned into a bull

run, which took the Sense to 6679 on the first trading

day in the new year. And then it witnessed an abrupt

end to the bull run, signalled by a 316-point intra-day

decline in the Sensex on January 5. (Chart 1).

This volatility has been visible in the medium and

long term as well. From a low of 2924 on April 5,

2003, the Sensex had risen to 6194 on January 14,

2004, only to fall to 4505 on May 17, before rising

to close at a peak of 6679 on January 3, 2005. These

wild fluctuations have meant that for those who bought

into the market at the right time and exited at the

appropriate moment, the average return earned through

capital gains were higher in 2003 than 2004, despite

the extended bull run in the latter year.

Chart

1 >> Click

to Enlarge

There are two messages that this experience sends

out. The first is that, if market expectations can

turn so whimsically, the signals or rumours on which

they are based must lack any substance since any ''fundamentals''

on which they could be anchored have not shifted so

violently. The second is that there must be some unusually

strong force that is determining movements in the

market which alone can explain the wild swings it

is witnessing.

The combination of these two factors is indeed a disconcerting

phenomenon, since if some force has the ability to

lead the market and the others can be taken along

without much resistance, the market is in essence

being subjected to manipulation, even if not always

consciously. Not surprisingly, recent market developments

have once more focused attention on the volatility

that has come to characterise India's stock markets.

Movements in the Sensex during the two years have

clearly been driven by the behaviour of foreign institutional

investors (FIIs), who were responsible for net equity

purchases of as much as $6.6 and $8.5 billion respectively

in 2003 and 2004. These figures compare with a peak

level of net purchases of $3.1 billion as far back

as 1996 and net investments by FIIs of just $753 million

in 2002. In sum, the sudden FII interest in Indian

markets in the last two years account for the two

bouts of medium-term buoyancy that the Sensex recently

displayed.

At one level this influence of the FIIs is puzzling.

The cumulative stock of FII investment, totalling

$ 30.3 billion at the end of 2004, amounted to just

8 per cent of the $383.6 billion total market capitalisation

on the Bombay Stock Exchange. However, FII transactions

were significant at the margin. Purchases by FIIs

of $31.17 billion between April and December 2004

amounted to around 38.4 per cent of the cumulative

turnover of $83.13 billion in the market during that

period, whereas sales by FIIs amounted to 29.8 per

cent of turnover. Not surprisingly there has been

a substantial increase in the share of foreign stockholding

in leading Indian companies. According to one estimate,

by end-2003, foreigners (not necessarily just FIIs)

had cornered close to 30 per cent of the equity in

India's top 50 companies — the Nifty 50. In contrast,

foreigners collectively owned just 18 per cent in

these companies at the end of 2001 and 22 per cent

in December 2002.

A recent analysis by Parthaprathim Pal estimated that

at the end of June 2004, FIIs controlled on average

21.6 per cent of shares in Sensex companies. Further,

if we consider only free-floating shares, or shares

normally available for trading because they are not

held by promoters, government or strategic shareholders,

the average FII holding rises to more than 36 per

cent. In a third of Sensex companies, FII holding

of free-floating shares exceeded 40 per cent of the

total.

As Table 1, shows matters have not changed significantly

more recently. As of September 2004, which is the

last quarter for which information is available, FII

shareholding in the 30 companies included in the Sensex

stood at an average of 19.6 per cent. What is noteworthy,

however, is that this proportion varied from a low

of 2.52 per cent to a high of as much as 54 per cent

in the case of Satyam Computers and 63.17 per cent

in the case of HDFC. If FIIs as a group chose to move

out of the stock concerned, a collapse in the price

of the equity is inevitable.

Table

1: FII Holding in Sensex Companies End-September

2004 |

|

FII

Holding |

Total

Stock |

FII

Share |

Associated Cement

Companies Ltd. |

40900718 |

178277669 |

22.94 |

|

Bajaj Auto |

16330247 |

101183510 |

16.14 |

|

Bharti Tele |

221015179 |

1853366767 |

11.93 |

|

BHEL |

53591202 |

244760000 |

21.90 |

|

Cipla Ltd. |

52682658 |

299870233 |

17.57 |

Dr.Reddy's Laboratories

Ltd. |

12809188 |

76518949 |

16.74 |

|

Grasim Industries Ltd. |

19113076 |

91671233 |

20.85 |

Gujarat Ambuja Cements

Ltd. |

41620922 |

179399951 |

23.20 |

|

HDFC Bank Ltd. |

76402122 |

286232913 |

26.69 |

|

Herohonda M |

46161349 |

199687500 |

23.12 |

|

Hindalco IN |

17828040 |

92475275 |

19.28 |

|

Hindustan Lever Ltd. |

278289559 |

2201243793 |

12.64 |

Hindustan Petroleum

Corp. Ltd. |

66559789 |

339330000 |

19.62 |

Housing Development

Finance Co |

156482326 |

247703418 |

63.17 |

|

I T C Ltd. |

37548907 |

247924902 |

15.15 |

|

ICICI Bank Ltd. |

359488564 |

735928149 |

48.85 |

Infosys Technologies

Ltd. - ORDI |

108676702 |

267860670 |

40.57 |

|

Larsen & Toubro

Ltd. |

24048087 |

129902937 |

18.51 |

|

Maruti Udyog |

34644938 |

288910060 |

11.99 |

|

Ong Corp Ltd. |

93054697 |

1425933992 |

6.53 |

Ranbaxy Laboratories

Ltd. |

41321691 |

185831140 |

22.24 |

|

Reliance |

319138099 |

1396377536 |

22.85 |

|

Reliance ENR* |

32896582 |

185572799 |

17.73 |

|

Satyam Comp |

171632507 |

317593572 |

54.04 |

|

State Bank of India |

60294540 |

526298878 |

11.46 |

Tata Iron and Steel

Co.

Ltd. |

66306238 |

553472856 |

11.98 |

|

Tata Motors |

76364625 |

358485286 |

21.30 |

|

Tata Power |

26069920 |

197897864 |

13.17 |

|

Wipro Ltd. |

17630021 |

698951673 |

2.52 |

|

Zee Telef Lt |

154980521 |

412505012 |

37.57 |

|

Total Sensex Cos |

2723883014 |

14321168537 |

19.02 |

Table

1 >> Click

to Enlarge

Table 2, which provides the frequency distribution

of Sensex companies according to the size class of

FII shareholding proportions at the end of the first

three quarters of 2004, suggests that FIIs do shift

in and out of particular shares, just as they are

known to shift in and out of particular markets. Between

end-March and end-June FIIs were reducing their exposure

in Sensex companies, wheras by end-September they

had once again begun to increase their exposure. If

at the end of June there were 5 companies in which

the share of FIIs in total equity was less than 10

per cent, this figure had fallen to 2 by end-September,

whereas the number of firms in which FII exposure

was 10-20 per cent had risen from 12 to 14 and those

with 20-30 per cent exposure from 8 to 9. Given the

short period in which this had occurred and the small

proportion of floating shares in the case of many

companies, these changes are indeed significant.

Table 2: Frequency Distribution of FII Holdings

in Sensex Companies |

|

March 2004 |

June 2004 |

September 2004 |

|

< 10 per cent |

3 |

5 |

2 |

|

10-20 per cent |

13 |

12 |

14 |

|

20-30 per cent |

9 |

8 |

9 |

|

30-40 per cent |

1 |

2 |

2 |

|

> 40 per cent |

4 |

3 |

3 |

Table

2 >> Click

to Enlarge

Given the presence of foreign institutional investors

in Sensex companies and their active trading behaviour,

their role in determining share price movements must

be considerable. Indian stock markets are known to

be narrow and shallow in the sense that there are

few companies whose shares are actively traded. Thus,

although there are more than 4700 companies listed

on the stock exchange, the BSE Sensex incorporates

just 30 companies, trading in whose shares is seen

as indicative of market activity. This shallowness

would also mean that the effects of FII activity would

be exaggerated by the influence their behaviour has

on other retail investors, who, in herd-like fashion

tend to follow the FIIs when making their investment

decisions.

These features of Indian stock markets induce a high

degree of volatility for four reasons. In as much

as an increase in investment by FIIs triggers a sharp

price increase, it would provide additional incentives

for FII investment and in the first instance encourage

further purchases, so that there is a tendency for

any correction of price increases unwarranted by price

earnings ratios to be delayed. And when the correction

begins it would have to be led by an FII pull-out

and can take the form of an extremely sharp decline

in prices.

Secondly, as and when FIIs are attracted to the market

by expectations of a price increase that tend to be

automatically realised, the inflow of foreign capital

can result in an appreciation of the rupee vis-à-vis

the dollar (say). This increases the return earned

in foreign exchange, when rupee assets are sold and

the revenue converted into dollars. As a result, the

investments turn even more attractive triggering an

investment spiral that would imply a sharper fall

when any correction begins.

Thirdly, the growing realisation by the FIIs of the

power they wield in what are shallow markets, encourages

speculative investment aimed at pushing the market

up and choosing an appropriate moment to exit. This

implicit manipulation of the market if resorted to

often enough would obviously imply a substantial increase

in volatility.

Finally, in volatile markets, domestic speculators

too attempt to manipulate markets in periods of unusually

high prices. Thus, most recently, the SEBI is supposed

to have issued show cause notices to four as-yet-unnamed

entities, relating to their activities on around Black

Monday, May 17, 2004, when the Sensex recorded a steep

decline to a low of 4505.

All this said, the last two years have been remarkable

because, even though these features of the stock market

imply volatility; there have been more months when

the market has been on the rise rather than on the

decline. This clearly means that FIIs have been bullish

on India for much of that time. The problem is that

such bullishness is often driven by events outside

the country, whether it be the performance of other

equity markets or developments in non-equity markets

elsewhere in the world. It is to be expected that

FIIs would seek out the best returns as well as hedge

their investments by maintaining a diversified geographical

and market portfolio. The difficulty is that when

they make their portfolio adjustments, which may imply

small shifts in favour of or against a country like

India, the effects it has on host markets are substantial.

Those effects can then trigger a speculative spiral

for the reasons discussed above, resulting in destabilising

tendencies. Thus the end of the bull run in January

was seen to be the a result of a slowing of FII investments,

partly triggered by expectations of an interest rate

rise in the US.

These aspects of the market are of significance because

financial liberalisation has meant that developments

in equity markets can have major repercussions elsewhere

in the system. With banks allowed to play a greater

role in equity markets, any slump in those markets

can affect the functioning of parts of the banking

system. We only need to recall that the forced closure

(through merger with Punjab National Bank) of the

Nedungadi Bank was the result of the losses it suffered

because of over exposure in the stock market,

On the other hand if FII investments constitute a

large share of the equity capital of a financial entity,

as seems to the case with HDFC, an FII pull-out, even

if driven by development outside the country can have

significant implications for the financial health

of what is an important institution in the financial

sector of this country.

Similarly, if any set of developments encourages an

unusually high outflow of FII capital from the market,

it can impact adversely on the value of the rupee

and set of speculation in the currency that can in

special circumstances result in a currency crisis.

There are now too many instances of such effects worldwide

for it be dismissed on the ground that India's reserves

are adequate to manage the situation.

Thus, the volatility being displayed by India's equity

markets warrant returning to a set of questions that

have been bypassed in the course of neoliberal reform

in India. The most important of those questions is

whether India needs FII investment at all. With the

current account of the balance of payments recording

a surplus in recent years, thanks to large inflows

on account of non-resident remittances and earnings

from exports of software and IT-enabled services,

we don't need those FII flows to finance foreign exchange

expenditures. Neither does such capital help finance

new investment, focussed as it is on secondary market

trading of pre-existing equity. The poor showing of

the markets on the IPO front in most years during

the 1990s is adequate confirmation of this. And finally,

we do not need to shore up the Sensex, since such

indices are inevitably volatile and merely help create

and destroy paper wealth and generate, in the process,

inexplicable bouts of euphoria and anguish in the

financial press.

In the circumstances, the best option for the policy

maker is to find ways of reducing substantially the

net flows of FII investments into India's markets.

This would help focus attention on the creation of

real wealth as well as remove barriers to the creation

of such wealth, such as the constant pressure to provide

tax concessions that erode the tax base and the persisting

obsession with curtailing fiscal deficits, both of

which are driven by dependence on finance capital.