The Lurking Debt Problem*

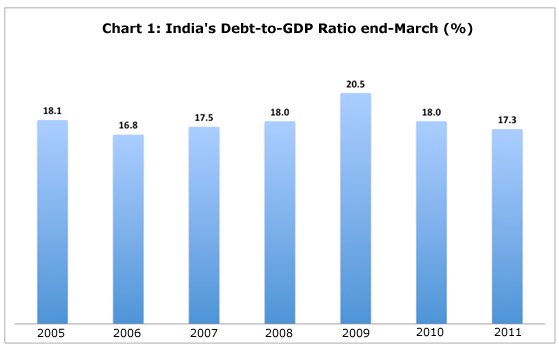

Three months ago, when the Finance Ministry released its annual assessment of India's external debt position, the scenario appeared comforting. On the one hand, the external debt to GDP ratio, at 17.3 per cent at the end of March 2011 (Chart 1), was well within limits considered safe. It was lower than in many other countries, much below where it had been during the 1991 crisis and below its level in the previous two years. Combine this with the fact that India has accumulated considerable foreign exchange reserves to cover any bunching of repayments and external debt does not appear to be among the country's problem areas.

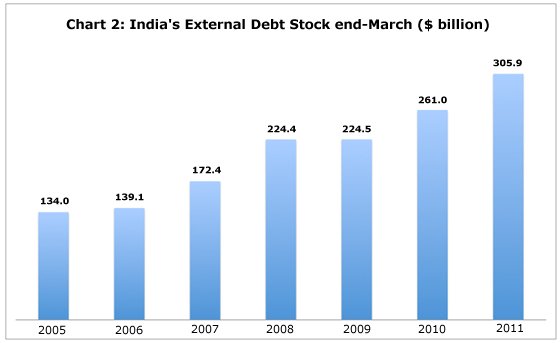

However, a closer examination of recent trends suggests that there may be some cause for concern on the external debt front. To start with, in recent years the absolute volume of external debt has been rising quite sharply, except for stagnation in crisis-year 2009. The stock of debt at the end of March rose by $33 billion and $52 billion in 2007 and 2008 and by $37 billion and $45 billion in 2010 and 2011 respectively (Chart 2). Clearly, India's appetite for debt has been increasing.

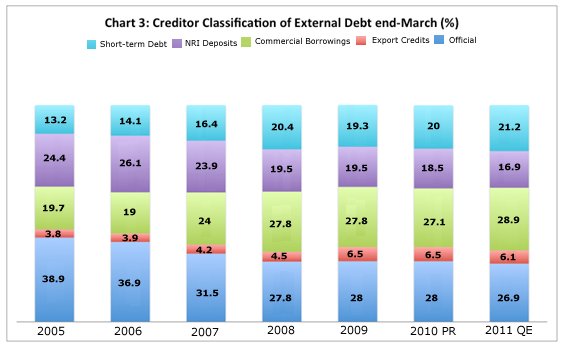

Secondly, as has been known for some time now, India is being graduated out of official (bilateral and multilateral) debt, so that the share of private sources in total debt has been rising significantly. Third, within these private sources, the share of deposits from Non-resident Indians seeking to benefit from differentials in interest rates between the Indian and global markets has been falling, while that of external borrowing by domestic entities has increased from around 20 per cent in 2005 to almost 30 per cent in 2011 (Chart 3).

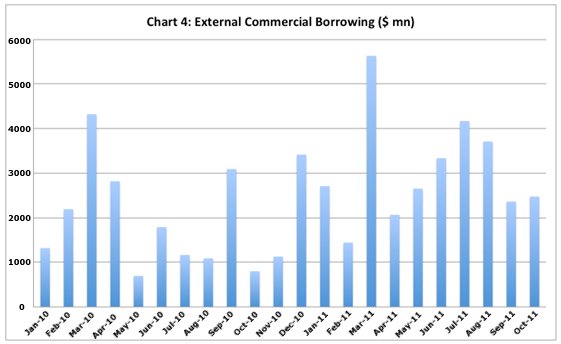

This increasing role for commercial borrowing has essentially been because of an increase in borrowing by India firms from international markets. The Reserve Bank of India releases monthly figures on external borrowing by Indian corporates through the ‘automatic' and ‘approval' routes. The most recent figure is for October 2011. Those figures show that despite month-to-month fluctuations, external borrowing by these entities has risen quite sharply from $8.6 billion between April and October 2010 to $16.4 billion between November 2010 and May 2011, and to $18.7 billion between April and October 2011 (Chart 4).

Finally, there has been an increase in short-term debt in total external

borrowing from 13 per cent to 21 per cent of the total. This may partly

reflect the unwillingness of lenders to increase only their long-term

exposures in a country with a rising appetite for debt. It may also

be because Indian borrowers are also using the short-term channel to

reduce financing costs, in the belief that they can, if necessary, roll-over

that debt when due.

Thus, the growth in external debt has been substantially because the

Indian corporate sector has stepped up its commercial borrowing from

the international market. This trend seems to have accelerated in recent

times. Underlying the month-to-month variations in the volume of borrowing

because of the presence or absence of large individual borrowers, there

is evidence of a continuous rise. To add to this, Indian borrowers have

not shied away from short-term debt either.

Three factors explain this tendency. One is the increased reliance of

the corporate sector on debt (as opposed to equity) to finance expenditures,

and more so on foreign debt because on average it tends to be much cheaper.

A second obvious cause is the sharp rise in domestic interest rates.

The Reserve Bank of India has announced around a dozen increases in

reference rates since March last year, raising the cost of credit provided

to the banking system by more than 3 percentage points. Since this is

the rate at which banks can borrow from the RBI, they in turn are charging

higher rates on loans to their clients. In the event, there has been

a widening of interest rates payable on borrowing from the domestic

and external markets, with the latter being the cheaper source. When

this happens, the normal tendency would be for firms to borrow abroad

to meet even their domestic expenditures and finance their expansion

plans targeted at the domestic market.

Finally, this tendency has been encouraged by the willingness of the

government to permit such access. In principle there is a ceiling on

aggregate external commercial borrowing (ECB) set by the government

at each point in time. But not only is that ceiling not imposed strictly,

but the government periodically revises the ceiling to accommodate increases

in private borrowing. The most recent increase was a $5 billion hike

in the ceiling for both government and corporate ECB to $15 billion

and $45 billion respectively.

This lax attitude has been strengthened by the rise in domestic interest

rates. With evidence that GDP growth and industrial growth are faltering,

the government and the RBI have been criticised for hurting growth in

an unsuccessful attempt to control inflation by hiking rates. One way

to mute that criticism is to allow the bigger and more vocal firms to

access cheap resources from the international market by permitting increased

volumes of ECB. Moreover, any increased inflow of foreign capital, even

in the form of debt, helps to shore up the rupee (which has depreciated

because of the global flight to safety to the dollar and the recent

tendency for foreign investors to exit from India in the context of

increasing trade and current account deficits in India's balance of

payments). This effect on the rupee must also be motivating the RBI

to facilitate the increase in debt.

There are, however, two much-discussed dangers associated with this

tendency. First, there arises a mismatch between the currency in which

debt service commitments on external loans must be met and the currency

in which revenues are garnered from the domestic market-oriented activities

that are financed by such loans. Hence, a part of the foreign exchange

earned or acquired in other activities would have to be diverted to

these borrowers in the future so that they can meet their debt service

commitments. This could put some strain on the balance of payments.

The second problem is that the borrowers themselves are taking on substantial

exchange rate risks. While they may be obtaining finance at interest

rates lower than currently charged in the domestic market, their debt

service commitments in rupee terms can rise sharply if there is a depreciation

of the domestic currency. This could more than neutralise the benefit

of an interest rate differential.

Besides these factors that call for exercise of caution, another danger

is a rise in in rates in international markets. Those interest rates

are low now because central banks in the developed countries have pumped

large volumes of cheap liquidity into the market in response to the

crisis. But there is no guarantee that the era of access to cheap liquidity

for emerging markets will continue, as illustrated by the difficulties

being faced by the peripheral countries in the Eurozone. If international

rates rise, efforts to refinance maturing debt would require expensive

borrowing. When all of this is put together, the rise in external borrowing,

though still within limits, increases the vulnerability of the corporate

sector and the nation.

The government, therefore, would be well-advised to continue with its

policy of limiting external borrowing. However, under pressure from

the corporate sector, it seems to be inclined towards loosening rules

with respect to external borrowing, to dampen corporate criticism of

the high interest rate regime. In response, corporates are being offered

an escape to cheap credit through means that increase external vulnerability.

There are conspiracy theories doing the rounds. Rumour has it that there

is a standoff between the Ministry of Finance and the Reserve Bank of

India over interest rate policy. Given the government's own failure,

the central bank has been forced to take on the burden of combating

inflation, leading to the sharp rise in interest rates. But since the

Finance Ministry does not seem to like that, it is reportedly using

the ECB lever to counter the impact of the RBI's intervention on the

corporate sector. Whatever the drivers, the process is increasing external

vulnerability.

*

This article was originally published in the Business Line on 12 December,

2011, and is available at

http://www.thehindubusinessline.com/opinion/columns/c-p-chandrasekhar/

article2709520.ece?homepage=true