Is the Centre Resource-stretched?

Speaking

on the need for more inclusive growth at the recently held National

Development Council meeting to approve the Approach to the XIth Plan,

Prime Minister Manmohan Singh reportedly said: ''We cannot escape the

fact that the Centre's resources will be stretched in the immediate

future and an increasing share of the responsibility will have to be

shouldered by the States.'' More generally, his view on resources for

the Plan was that much of the investment needed for rapid growth would

come from the private sector. This, in his opinion, called for a sound

macroeconomic framework, an investor-friendly environment and a strong

and innovative financial sector capable of responding to the needs of

new entrepreneurs.

Implicit in this position are two contentious issues. The first is the

validity of the view that reliance on the private sector to deliver

investment and growth would not imply an inequalising and less inclusive

path of development, especially if private initiative is combined with

social expenditures financed by the government. There are indeed many

who believe that the crisis in agriculture (which the Prime Minister

referred to) and the evidence of exclusion (which he emphasised) are

partly the result of the shift to a private sector-led strategy of growth.

In the event an 8 per cent growth rate notwithstanding, large sections

of the population garner few benefits and even experience deterioration

in their economic position.

The second contentious issue is that in the process of creating an investor-friendly

environment—which in practice implies substantial tax concessions and

reduced tax rates—the Centre may be engineering an environment when

it finds itself resource-stretched to finance even crucial capital and

social expenditures, encouraging it to call upon state governments to

take a larger share of the responsibility.

We are here concerned with the second of these propositions. One striking

feature of the period since 1989-90, which incorporates the years of

accelerated economic reform is that despite evidence of high and accelerating

growth rates and signs of growing inequality, there has been no improvement

in the Centre's ability to garner a larger share of resources to finance

expenditures it considers crucial. Even when corporate profits and managerial

salaries are reported to be rising sharply, taxes do not appear as buoyant.

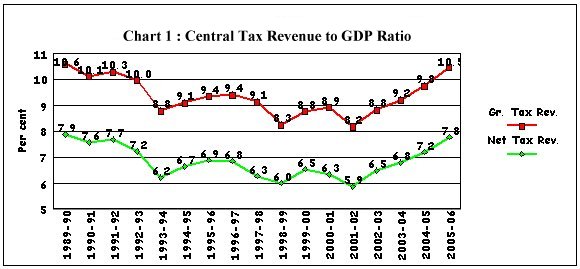

The Central tax-to-GDP ratios in India have been declining for much

of this period. And despite the increase in the ratio in recent years,

their 2005-06 values were at around the same level they were at in 1989-90

(Chart 1).

As can be seen from Chart 1, the tax-to-GDP ratios were at their lowest in 2001-02, when they stood at 8.2 per cent in the case of the Centre's Gross Tax Revenue and 5.9 per cent in the case of Net Tax Revenue, having fallen from 10.6 and 7.9 per cent respectively in 1989-90. This decline has occurred despite some improvement in the collection of Corporation, Income and Service taxes (relative to GDP) because they could not cover the loss suffered in customs duty collections and excise duty revenues as a result of trade liberalisation and the ostensible ''rationalisation'' of excise duties (Table 1).

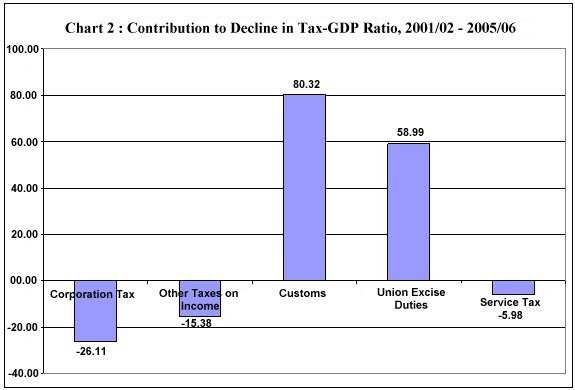

If we decompose the decline in the tax-GDP ratio between 1989-90 and 2001-02, the contribution of the decline in customs duties relative to GDP amounted to 80 per cent and that of Excise Duties to 58 per cent. Hence, despite the neutralising effects of the improved contributions from Corporation Taxes (26 per cent), Income Taxes (15.4 per cent) and the newly introduced Service Tax (6 per cent), the decline in the overall tax-GDP ratio could not be stalled.

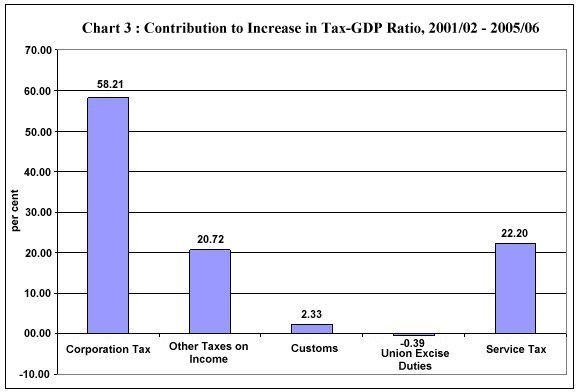

It is indeed true that, subsequently, buoyant corporate profits, a widened tax base and improved collection of dues and arrears, have helped raise the tax-GDP ratio. But despite high growth, improved profitability and signs of increased inequality (which should improve tax collection), the increase has just been adequate to put the tax-GDP ratio back to its immediate pre-liberalisation levels. This is because, while Corporation, Income and Service tax revenues (particularly the first) contributed to the increase, their effect was inadequate to raise the level above that which prevailed in the late 1980s.

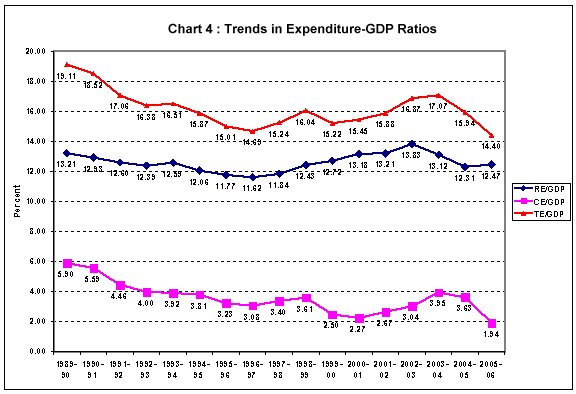

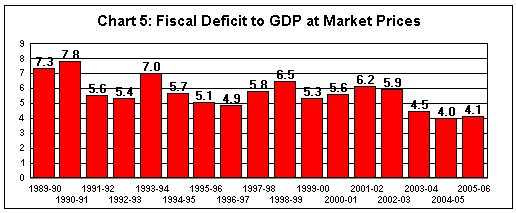

What is noteworthy is that the decline in capital expenditure has been particularly sharp over the three years ending 2005-06, when the central tax-GDP ratio has been on the rise. This was because these where the years when, armed with the Fiscal Responsibility and Budget Management (FRBM) Act, the government has been finally realising its ambition to substantially curtail the fiscal deficit (Chart 5). With revenues not rising adequately and the fiscal deficit being curtailed significantly, expenditures had to be cut to fulfil the FRBM Act, and the axe fell disproportionately on capital expenditures. This is the reason why the Prime Minister has to declare that investment and growth in the coming years will have to be driven by the private sector.

There are a number of difficulties with that argument. To start with, it does not question whether tariff reductions that have such a significant impact on revenues were justified. In fact, when tariff reductions were being made, one of the arguments was that trade buoyancy would ensure that revenue losses would be marginal. This has not really occurred. Second, it glosses over the fact that what was considered mere ''rationalisation'' of the excise duty structure, as part of a process of fiscal reform, has amounted in practice to the provision of significant excise duty concessions that have had extremely adverse effects. Third, it does not raise the question, which has been raised by the Planning Commission itself, whether there is any rationale for sharply curtailing the fiscal deficit, despite its extremely adverse impact on capital and social expenditures.

Finally, it does not answer the criticism that the Centre has not gone even part of the way in tapping resources from direct taxes of various kinds, but in fact has doled out concessions that are unjustifiable. A striking example is the income earned from equity investment. There are two principal ways in which income is garnered through such investment: dividends and capital gains. Both have them have benefited from recent tax concessions. To start with, on the grounds that corporate incomes are already taxed so that taxing shareholder dividend income would amount to a form of double taxation, it was decided in 1999-2000, that dividends paid out to shareholders should be made tax-free. Being controversial, this decision was reversed in the budget for 2002-03, only to be reinstated again in the Budget for 2003-04.

What has been the fall-out of this exemption? An extremely revealing analysis by B.G. Shirsat (Business Standard, July 14 and 22/23, 2006) of 1,050 major dividend-paying, listed companies has found that dividends paid out during the three years ending 2005-06 amounted to Rs. 29,532 crores. Since the beneficiaries of these dividends are likely to be in the highest marginal tax bracket, if this dividend income had been subject to tax, the revenue earned by the government over these three years would have been an additional Rs.10,000 crore (if we assume that the dividend pay out rate would have been the same even if the tax was effective). This is by no means a small sum.

What is noteworthy is the inequality in the distribution of this tax benefit. It is known that a miniscule proportion of the domestic population invests in equity. But even among them, the distribution of dividend and therefore the benefit of the tax exemption is highly skewed. Of the close to Rs.30,000 crore of dividends paid out by these companies, Rs.14,000 crore or around 45 per cent accrued to the promoters of the companies themselves. In fact, small or so-called ''retail'' shareholders received a relatively small share of this benefit. Over ninety per cent of the shareholders holding up to 500 shares each received just over Rs.4000 crore of dividend income, while public shareholders with equity holding in excess of 500 shares garnered Rs.7,575 crore as dividends. A significant amount of the dividend paid to public shareholders went to foreign investors. Foreign institutional investors (FIIs) received Rs.12, 808 crore of dividend income during this period and investors in GDRs and ADRs, NRI investors and other overseas bodies received Rs.4,567 crore. In sum, a combination of promoters, high net worth domestic investors and foreigners were the main beneficiaries of the dividend tax hand out.

There remains the argument that the exemption of dividends from taxes was not a hand out but the redressal of an unjust scheme of double taxation. Even if this is accepted, there remains the fact that there is a high degree of inequality in the distribution of incomes in the country, which the accrual of record dividend incomes seems to aggravate substantially. If the idea was for the government to garner a fair share of the surplus for social and capital expenditures, then the removal of the tax on dividends should have been accompanied by an increase in the marginal corporate tax rate. The fact that the government has not chosen to resort to such an increase only strengthens the perception that it has failed to tax a section of the rich adequately and effectively.

The evidence on unwarranted benefits to investors in equity does not end here. It is visible in the case of the other form of return from equity holding—capital gains—as well. The budget for 2003-04 also decided that, ''in order to give a further fillip to the capital markets'', all listed equities that were acquired on or after March 1, 2003, and sold after the lapse of a year, or more, were to be exempted from the incidence of capital gains tax. Capital gains made on those assets held by the purchaser for at least 365 days were defined for taxation purposes as long term gains. Long term capital gains tax was being levied at the rate of 10 per cent up to that point of time.

An analysis of share price movements of 28 Sensex companies found that if we assume that all shares purchased in 2004 were sold after 365 days in 2005, the total capital gains that could have been garnered in 2005 would have amounted to Rs. 78,569 crore. If these gains had been taxed at the rate of 10 per cent prevalent earlier, the revenue yielded would have amounted to Rs. 7,857. That reflects the revenue foregone by the State and the benefit accruing to the buyers of these shares. It is indeed true that not all shares of these companies bought in 2004 would have been sold a year-and-one-day later. But some shares which were purchased prior to 2004 would have been sold during 2005, presumably with a bigger margin of gain. And this estimate relates to just 28 companies.

In sum, the stock market alone has become the site for tax-exempt gains of a magnitude which suggest that a more appropriate tax policy relating to dividends and capital gains could have yielded substantial revenues for the government. This is only one area. There are many more such which the central government should look to when looking for money to finance crucial expenditures. But what the instances quoted prove is that in the effort not just to facilitate but ''induce'' private investment with tax concessions, the government is engineering a fiscal situation which is by no means indicative of a macroeconomic framework that is ''sound'' from a growth and equity point of view.