When

GDP growth bounced back to close to 9 per cent after

the slump induced by the global recession, India’s

growth performance once again appeared remarkable

by global comparison. But one feature that has sullied

this record is evidence of a deceleration in industrial

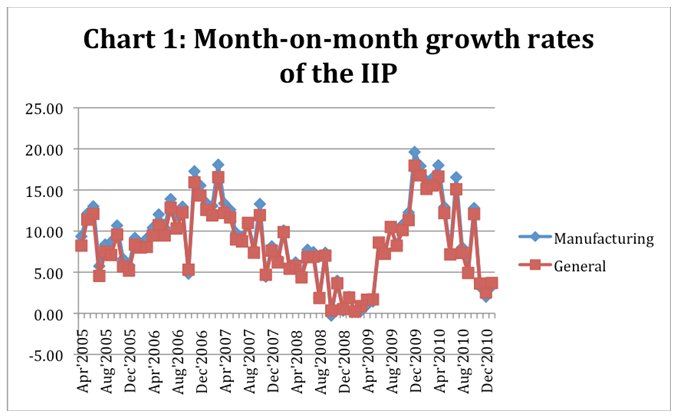

growth in recent months. Month-on-month annul growth

rates which stood at between 10 and 18 per cent during

most months of the August 2009 to July 2010 period,

have since decelerated and stood at less than 5 per

cent in four of the five most recent months (September

2010 to Jan 2011) for which data are available (Chart

1). As a result, even though annual rates of growth

are still respectable (Chart 2), some disquiet has

been expressed in various circles.

Chart

1 >> Click

to Enlarge

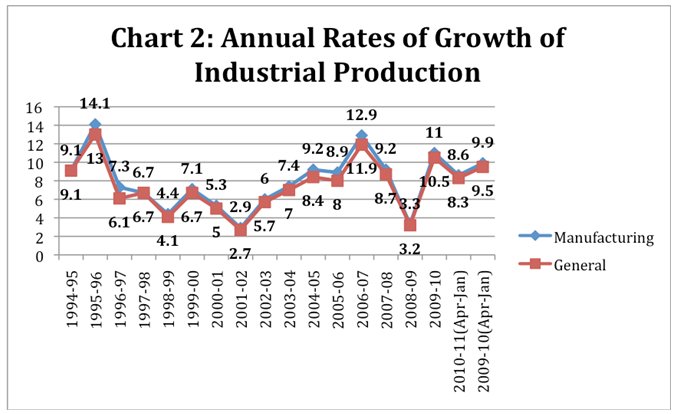

It

is useful to view the recent downturn as being part

of longer-term trends in industrial growth. Unfortunately,

since IIP figures have been recompiled from April

2004 onwards, using the new series of WPI to deflate

IIP items for which production is reported in value

terms, fully comparable month-on-month rates of growth

are available only from April 2005. But examining

this series (Chart 2) points in two directions. The

first is that the recent downturn is sharper than

the one experienced during the immediately preceding

cycle. Second, while the previous downturn may have

begun earlier, it stretched across the period that

saw the onset of the global financial crisis and witnessed

the global recession. On the other hand, the more

recent downturn has occurred in a period when the

recession had bottomed out and the world economy was

experiencing a recovery.

Chart

2 >> Click

to Enlarge

One inference that could be

drawn from this is that it is not so much an export

recovery as developments in the domestic market that

underlie the deceleration in industrial growth. This

is of significance because, as Chart 2 illustrates,

if we take a long view, after a mini-boom during the

mid-1990s, industrial growth remained low for most

years during the 1996-97 to 2002-03 period. After

that, growth recovered and reached a peak in 2006-07.

And, if we exclude 2008-09, which was a year of slow

growth induced by the global recession, it appears

that Indian industry had subsequently settled into

a trajectory of growth of around 8 to 9 per cent a

year. What the recent slowdown does is question the

sustainability of that manufacturing growth trajectory.

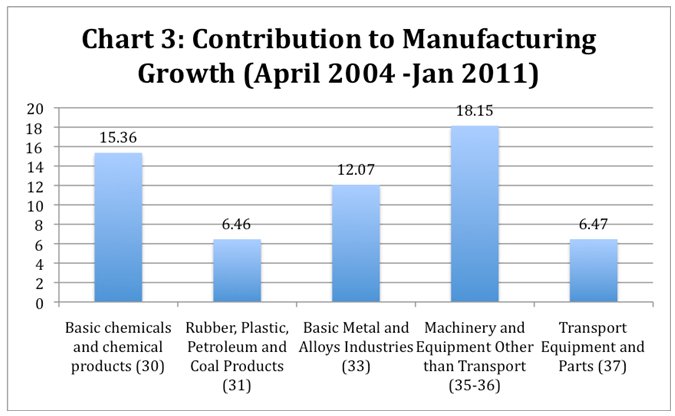

The sustainability issue is all the more relevant

because of the concentration of post-2004 growth in

a few industrial sectors. Consider for example an

analysis in which the contribution of each of 17 two-digit

industry groups to aggregate manufacturing growth

during April 2004 and January 2011 is computed. This

is done by multiplying by the trend rate of growth

of the relevant group with its weight in the index

of manufacturing production. The resulting figure

shows that that there are only five of these seventeen

that contributed at least 5 per cent of the observed

growth in manufacturing over this period. These five

were all metal- or chemical-based and included: (i)

Manufacture of Basic Chemicals and Chemical Products

(except products of petroleum and coal) (Group 30

of National Industrial Classification 1987); (ii)

Manufacture of Rubber, Plastic, Petroleum and Coal

Products (Group 31); (iii) Basic Metal and Alloys

Industries (Group 33); (iv) Manufacture of Machinery

and Equipment Other than Transport Equipment (Group

35-36); and (v) Manufacture of Transport Equipment

and Parts (Group 37). These five out of 17 industry

groups accounted for as much as 58.5 per cent of the

total growth in the index of manufacturing production

(Chart 3).

Chart

3 >> Click

to Enlarge

This concentration of growth

in the metal- and chemical-based industries has a

number of possible implications. The most obvious

of these stems from the fact that the metal- and chemical-based

industries tend to be among the more capital intensive

in the industrial sector. Employment per unit of investment

or output in these industries is much smaller than

in many other manufacturing sectors. Hence, if growth

is biased in favour of the metal- and chemical-based

industries, the responsiveness of employment in the

manufacturing sector to a unit increase in manufacturing

output would be lower than would otherwise be the

case. Growth could be jobless or inadequately job

creating. This has indeed been a feature characterising

registered manufacturing growth in India in recent

years.

But there could be implications for the nature of

growth itself. To start with, inasmuch as it is domestic

demand that drives growth in these industries, that

demand would in all probability be fuelled by (i)

public expenditure, particularly public investment,

which tends to be biased in favour of demand for these

industrial products; (ii) upper income group consumption

of such commodities that are normally not ''necessities'';

and (iii) debt-financed household investment (in housing),

purchases of automobiles and consumption of ''luxuries''.

These are the kinds of demands for final products

that tend to be directed at the metal- and chemical-based

industries. Hence, growth based on such industries

would depend on the availability of one or more of

these sources of demand as stimuli for the industrial

sector.

Besides being driven by demands of these kinds, these

industries are normally in the nature of clusters,

in the sense that the metal- and chemical-based industries

are dependent on inputs from similar industries and

serve, if at all, as inputs for downstream metal-

and chemical-based industries. This results in the

fact that growth or deceleration in these sectors

tends to be ''cumulative''. If exogenous demand trends

induce a slowdown of growth in some of these industries,

they have a dampening effect on the growth of related

industries as well.

These two features of growth, in turn, have implications

for the sustainability of the growth process. If growth

is to continue, one or more of these sources of demand

must remain strong. There are limits to the degree

to which upper income demand can continue to sustain

growth, since even though incomes are high in this

group, the share of the population included is extremely

small. Hence, public expenditure and debt-financed

investment and consumption have to be sustained.

A feature of fiscal reform policy has been an attempt

by the government to rein in deficit spending by reining

in expenditures. This tendency has been stronger because

tax policy reform in recent years has focused on the

reduction of customs duties as part of trade liberalisation,

on a reduction of direct taxes to incentivise private

saving and investment, and of indirect taxes as part

of a process aimed at rationalising them. As a net

result the tax-GDP ratio has been significantly lower

than would have been the case if these changes had

not been made. A corollary is that for any given reduction

of the fiscal deficit, the expenditure-reduction required

tends to be higher than would have been the case earlier.

Thus, the more successful is fiscal reform in terms

of tax and deficit reduction, the larger would be

the relative reduction in public expenditure.

From the point of view of industrial growth, therefore,

the successful implementation of fiscal reform implies

a transition to a deflationary fiscal environment

with dampened demand. It is possible that it is this

effect that explains the slowdown in industrial growth

in the period between the mid-1990s and 2003-04 (Chart

2). But that does raise the question as to the factors

underlying the subsequent recovery in industrial growth.

That recovery cannot be attributed to a reversal of

fiscal reform, except for the period after the onset

of the downturn induced by the global recession in

2008, when the government responded with a fiscal

stimulus that was adopted also because of the parliamentary

elections scheduled for April-May 2009.

Thus, during much of the period of high growth after

2003-04, the stimulus to industrial growth in all

probability came from debt-financed private investment

in housing, private purchases of automobiles and private

consumption. Growth based on debt-financed demand,

however, requires the continuous expansion of the

universe of the indebted. While enhanced availability

of cheap liquidity and financial innovation that can

bundle and distribute risk can encourage such expansion,

at some point the threat of unsustainable defaults

would slow, if not stop, the process. That would slow

demand growth as well. This is perhaps what explains

the evidence of the decline of the month-on-month

growth rates of the indices of manufacturing and industrial

production after March 2007, which was before the

global recession and well before its effects were

felt in India.

Once the effects of the recession were felt, industrial

growth slumped. It was the response of a government,

with an eye to the impending elections, to that slump,

that led to the recovery and return to high growth.

But the fiscal stimulus encouraged by the election

was a once-for-all effort on the part of a government

that was committed to fiscal conservatism. When it

returned to power it chose to unwind the stimulus.

It is because that unwinding process was not accompanied

by any neutralising surge in debt-financed private

investment and consumption that we have witnessed

over the last fiscal a significant deceleration in

month-on-month growth rates in industrial production,

which now appears to be quite steep. It is indeed

too early to conclude with confidence that this is

what is happening. But that seems to be an argument

that explains trends in industrial growth over the

medium term. If so, we can expect that we are set

for a return to a period of slower industrial growth

as happened in the second half of the 1990s. Unless

once again, some other stimulus, such as exports,

provides the basis for growth.