Lessons from the US Sub-prime Lending Crisis

A

noticeable feature of growth dynamics in contemporary times is that

investment and consumption spending by households has been an important

stimulus to growth. Such spending, in turn, has been stimulated by changes

in the financial sector that have increased the volume of credit, eased

interest rates and made credit available to individuals and firms that

would have earlier been considered inadequately creditworthy.

The last of these is of relevance, because it draws into the market

for housing and non-essential consumption a set of consumers, who would

not be present in these markets if their spending was determined by

their current income. A credit boom expands the market for certain assets

and commodities at a much faster rate than is possible if demand growth

were dependent purely on either income growth or on changes in income

distribution.

Needless to say, income growth does matter in the medium term, inasmuch

as indebted households would have to earn the incomes to meet the interest

and amortisation payments on their debt. If the requisite increases

in income do not materialise, defaults multiply and this unwinds the

boom. It would also have collateral effects because it impacts on financial

agents left with non-performing debt and assets whose prices are falling

because of excess supplies of confiscated assets on sale.

The US is an economy that now is experiencing such a downturn, the full

consequences of which are still unclear. The housing market in the US

has been crucial to sustaining growth in the US ever since the dotcom

bust of 2000. Galloping housing purchases stimulated residential investment

and rising housing asset values encouraged a consumption splurge, keeping

aggregate investment and consumption growing.

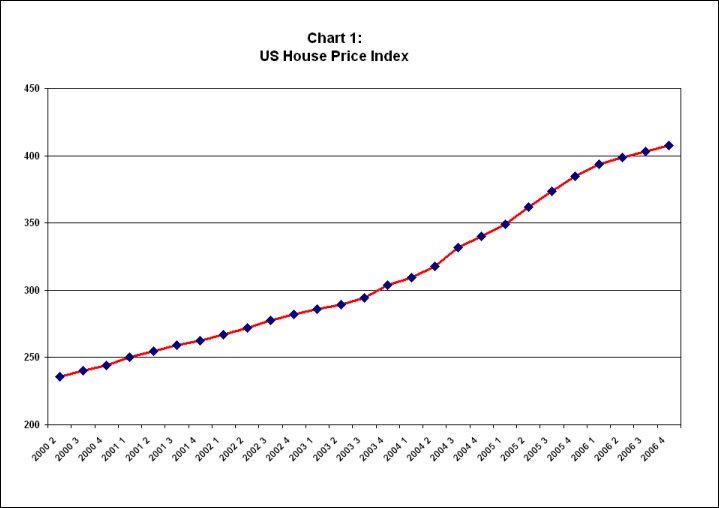

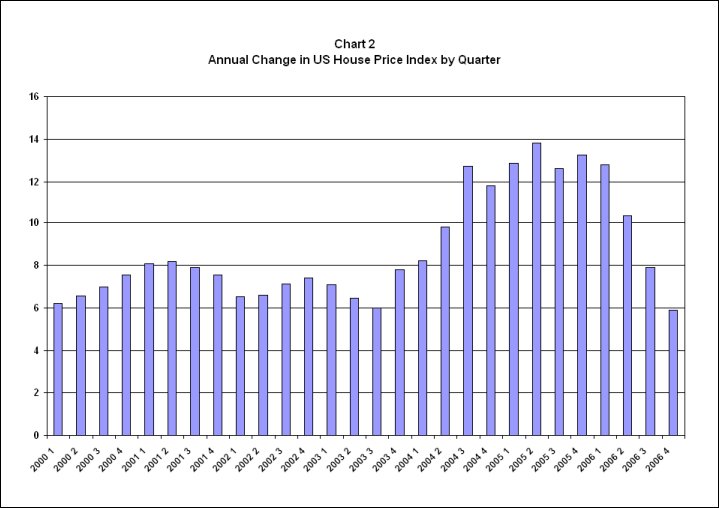

As Chart 1, which provides the quarter-wise annual rate of change in

the combined US House Price Index shows, the housing market began experiencing

a boom in the middle of 2003, which peaked in mid-2005. Though housing

prices have continued to rise since then, the annual rate of inflation

has consistently declined (Chart 2). This in itself may be a much needed

correction that should be welcome.

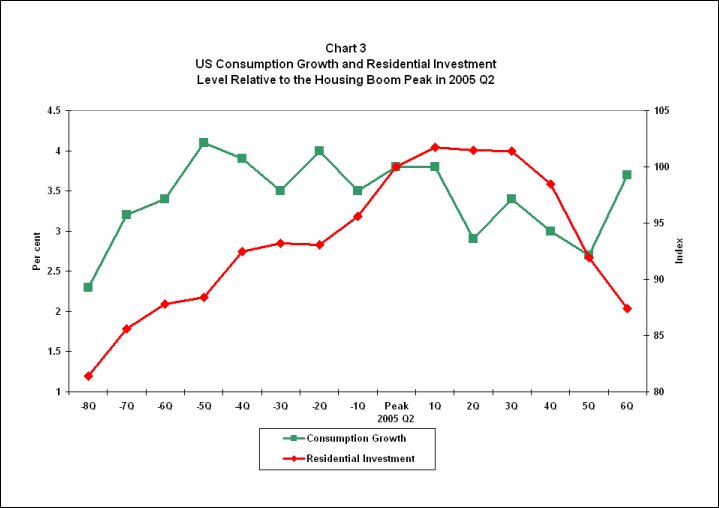

But the downturn is giving cause for concern for two reasons. First,

as mentioned earlier, growth in the US economy has been sustained by

the boom in housing. Rising house values increases the wealth of home

owners and has a wealth effect that encourages debt-financed consumption.

This drives demand and growth. The housing boom also pushes up residential

investment and construction which through the demands it generates and

the employment it creates helps accelerate growth. As Chart 3 shows,

these features seem to have played a role during the current housing

cycle as well, though the effect is more noticeable in the case of residential

investment than consumption, where other factors too must have played

a role.

The second problem lies in the way in which the boom was triggered and

kept going. Housing demand grew rapidly because of easy access to credit,

with even borrowers with low creditworthiness scores, who would otherwise

be considered incapable of servicing debt, being drawn into the credit

net. These sub-prime borrowers were offered credit at higher rates of

interest, which were sweetened by special treatment and unusual financing

arrangements-little documentation or mere selfcertification of income,

no or little down payment, extended repayment periods and structured

payment schedules involving low interest rates in the initial phases

which were "adjustable" and move sharply upwards when they

are "reset" to reflect premia on market interest rates. All

of these encouraged or even tempted high-risk borrowers to take on loans

they could ill afford, either because they had not fully understood

the repayment burden they were taking on or because they chose to conceal

their actual incomes and take a bet on building wealth with debt in

a market that was booming.

The

default risk which was almost inevitable in this kind of lending, increased

sharply when interest rates rose. The net result has been an increase

in defaults and foreclosures. The Mortgage Bankers Association has reportedly

estimated aggregate housing loan default at around 5 per cent of the

total in the last quarter of 2006, and defaults on high-risk sub-prime

loans at as much as 14.5 per cent. With a rise in so-called "delinquency

rates", foreclosed homes are now coming onto the market for sale,

threatening a situation of excess supply that could turn decelerating

house-price inflation into a deflation or decline in prices. The prospect

of such a turn are strong given estimates by firms like Lehman Brothers

that mortgage defaults could total anywhere between $225 billion and

$300 billion during 2007 and 2008.

The first casualties in the crisis have been the mortgage lenders, who

used borrowed capital to finance mortgage lending. Firms like New Century

Financial, WMC Mortgage and others, which made huge returns during the

boom, expanded lending volumes, encouraged by low interest rates and

slowing house price inflation in 2006. This required moving into the

sub-prime market to find new borrowers. Estimates vary, but according

to one by Inside Mortgage Finance quoted by the New York Times, sub-prime

loans touched $600 billion in 2006 or 20 per cent of the total as compared

with just 5 per cent in 2001. These mortgages reflected very little

own equity of the borrower. According to Bank of America Securities,

loans to sub-prime borrowers in 2001 covered on average 48 per cent

of the value of the underlying property. This had risen to 82 per cent

by 2006. According to the Financial Times, more than a third of sub-prime

loans in 2006 were for the full value of the property.

Mortgage lenders or brokers were encouraged to do this because they could easily sell their mortgages to banks and the investment banks in Wall Street to finance their activity and make a neat profit. And the investment banks themselves were keen to buy into the business because of the huge profits that could be made by "securitising" these mortgages. Firms such as Lehman Brothers, Bear Stearns, Merrill Lynch, Morgan Stanley, Deutsche Bank, UBS and others bought into mortgages, pooled them, packaged them into securities and sold them for huge fees and commissions. Numbers released by the Bond Market Association indicate that mortgaged backed securities issued in 2003 were at a peak in 2003 when they totalled $3 trillion. Even though total values have declined since then because of the deceleration in home price inflation, they are still close to the $2 trillion mark. Among the investors in these collateralised debt obligations (CDOs) are European pension fund and Asian institutional investors.

With high

returns on creating these products and facilitating trade in them, the

investment banks were hardly concerned with due diligence about the

underlying risk associated with these securities. That risk mattered

little to them since they were transferred to the purchasers of those

securities. The risks in the final analysis are shared with pension

funds and institutional investors which were buying into these securities,

looking for high returns in an environment of low interest rates. They

are now experiencing a sharp fall in their asset values and threatened

with losses.

In fact the process of securitisation involves many layers. To quote

the Financial Times, the original mortgages are "sold by specialist

mortgage lenders on to new investors, such as Wall Street banks, who

then use these to issue bonds which are often then repackaged again

as derivatives." According to that paper, data from the Securities

Industry and Financial Markets Association indicate that more than $2

trillion of mortgage-backed bonds were sold last year, of which about

a quarter were linked to sub-prime mortgages. In sum, this whole process,

which has at the bottom home owners faced with foreclosure, is driven

by layers of financial interests looking for quick profits or high returns.

This has transformed the mortgage securities business. In earlier times,

these securities were bought by investors who held them till the loans

matured and earned their returns over time. Now these are marked to

market and traded. They are also use to create complex derivatives which

too are marked to market and traded.

The net result is that the housing market crisis threatens to build

into a crisis of sorts in the US financial sector, resulting in a liquidity

crunch that can aggravate the slowdown and precipitate a recession.

All this has occurred also because of the regulatory forbearance that

has characterised the ostensibly "transparent" but actually

opaque markets that are typical of modern finance. Investment banks

did not reveal the weak credit base on which the mortgage securities

business was built, investment analysts routinely issued reports assuaging

fears of a meltdown, credit rating agencies did not downgrade dicey

bonds soon enough, and the market regulators chose to look the other

way when the speculative spiral was built.

But now that the crisis has struck, fingers are being pointed at others

by every segment of the business. The first fall-person has been the

ostensibly deceitful home owner. "Liar-loans" in which the

borrower does not truthfully declare incomes is blamed by the business

for its crisis. But it takes little to prevent such activity, if lenders

actually want to. The Mortgage Asset Research Institute, found from

an analysis of 100 loans involving self-declared incomes that documents

those borrowers had filed with the IRS showed that 60 per cent of them

had inflated their incomes by more than half. It doesn’t take much to

demand an IRS return when making a loan.

The investment banks are of course blaming the mortgage lenders. Wall

Street banks are filing suits to force mortgage lenders to repurchase

loans which they claim were sold to them based on misleading information.

If a Wall Street bank can be tricked, they don’t have the right to advise

investors where to put their money. And reports have it that those who

bought into the bonds and derivatives these banks peddled are planning

to move court accusing these Wall Street firms of failures of due diligence.

Finally, the regulators and Congress are sitting up, as they did after

the crash of the late 1990s which led to the passing of the Sarbanes-Oxley

Act. US Congressmen are threatening to frame a law that restricts the

freedoms investment banks and other financial entities have when creating

bonds and derivatives by repackaging mortgages to sell them to investors

around the world.

But all this is to wake up after the event has transpired. The "efficient"

American financial system is clearly not geared to preventing a crisis,

even if it proves capable of finding a solution. A solution that prevents

the sub-prime crisis from overwhelming the mortgage business as a whole,

by triggering a collapse in house prices, is imperative given the importance

of the housing boom in keeping the American economy going. A slowdown

in growth may be manageable. But a recession can send ripples across

the globe.

All this has lessons for countries like India. First, they should be

cautious about resorting to financial liberalisation that is reshaping

their domestic financial structures in the image of that in the US.

That structure is prone to crisis, as the dotcom bust and the current

crisis illustrates. Second, they should refrain from over-investing

in the doubtful securities that proliferate in the US. Third, they should

opt out of high growth trajectories driven by debt-financed consumption

and housing spending, since these inevitably involve bringing risky

borrowers into the lending and splurging net. Finally, they should beware

of international financial institutions and their domestic imitators,

who are importing unsavoury financial practices into the domestic financial

sector. The problem, however, is that they may have already gone too

far with processes of financial restructuring that have increased fragility

on all these counts.