Growth

in India is slowing, even as inflation remains stubbornly

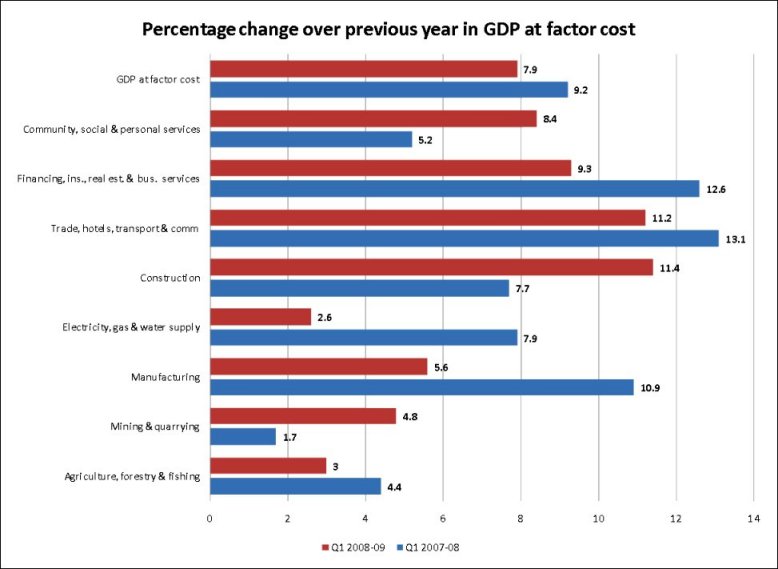

high. According to recently released figures, GDP

growth during the first quarter of 2008-9 stood at

7.9 per cent, down from the 9.2 per cent rate of growth

registered in the corresponding quarter of the previous

financial year. India, some fear, may have crossed

a turning point, with growth in the future likely

to be below the creditable 9 per cent per annum trajectory

achieved over the last five years. But, it could be

argued that a single quarter is no indication of what

could happen over even this financial year, let alone

over a longer period. In fact, over the last five

years there has been one (2004-05) when the rate of

growth fell to 7.5 per cent, only to bounce back the

next year. So the prospect of a long-term trend rate

of growth of 9 per cent may not have eroded as yet.

However, there are a number of features of growth

performance during the first quarter that give cause

for such concern. To start with, among the sectors

that have lost their momentum is agriculture. This

is of significance because advocates of reform have

been arguing that over the last three to four years,

the long-term, post-reform tendency for agricultural

growth to lag behind industry and services has been

reversed. If that was true, it is indeed an important

development, because one factor that was taking the

sheen off the higher growth of the 1990s and after

was the extreme disproportionality in growth between

the agricultural and non-agricultural sectors. The

disparity in the rate of growth of agricultural and

non-agricultural GDP increased significantly after

the 1970s, with the process being particularly marked

after the mid-1990s.

Chart

1 >> Click

to Enlarge

However, figures on trends in crop production do not

unequivocally support such a view. To start with,

in the case of all important crops, rates of growth

in individual years have been extremely volatile,

with high growth occurring in particular commodities

in very different years. The rate of growth of rice

stood at -6.1 per cent in 2004-05, 10.5 per cent in

2005-06, 1.7 per cent in 2006-07 and 3.21 per cent

in 2007-08. The corresponding figures for wheat were

-5.0, 1.1, 9.2 and 3.4. Volatility was particularly

marked in coarse cereals (-10.9, 1.8, -0.6 and 20.1)

and oilseeds (-3.2, 14.8, -13.2 and 18.5). The only

consistent and good performer was cotton with rates

of growth of 19.7, 12.8, 22.2 and 14.2 per cent in

each of these four years.

As a result of this volatility, a second feature of

recent agricultural growth performance was that the

average increase in production over the period 2003-04

to 2007-08 was low for almost all important crops

excepting sugarcane and cotton. Finally, the revival

in agricultural production holds largely for a few

non-foodgrain crops, especially cotton and sugarcane,

and not in foodgrains, which is one area where the

recent inflation in prices occurred. Thus, the “agricultural

revival”, as reflected in the figures on growth in

agricultural production was at best partial, and did

not correct the fundamental weakness that has characterised

post-reform growth in India.

The evidence that supported the view that the differential

between agricultural and non-agricultural growth rates

was being redressed was the rate of growth of GDP

in Agriculture and Allied Activities. While the rate

of growth of GDP in this sector was just 2.9 per cent

over the period 2000-01 to 2007-08 as a whole, it

stood at 5.9, 3.8 and 4.5 per cent respectively over

the three years ending 2007-08. Hence, the new evidence

that on a first quarter to first quarter basis agricultural

growth has fallen from 4.4 to 3.0 per cent, is indeed

disconcerting, especially because of news that the

monsoon this year has not been all too munificent

in many parts of the country.

The second feature of the first quarter 2008-09 GDP

figures that gives cause for concern is the fact that

manufacturing growth has slowed substantially from

10.9 per cent in the first quarter of 2007-08 to just

5.6 per cent during April to June of this financial

year. An aspect of the high growth in recent years

was that unlike during the second half of the 1990s

and the early 1990s, the sector that contributed significantly

to the growth transition was manufacturing, which

had recorded a sharp acceleration in annual rates

of growth after 2003. It had also registered a significant

and consistent increase in its contribution to the

quarter-on-quarter annual increment in GDP. This less-recognized

aspect of the growth story signified a shift away

from the excessive dependence on services to generate

increases in India’s GDP growth. What we have now

are signs of a possible reversal of this tendency.

Third, there is reason to believe that the Construction

sector, which had experienced significant acceleration

in its contribution to GDP from 7.7 to 11.4 per cent

of GDP between the first quarters of 2007-08 and 2008-09,

is losing its dynamism in recent times. Not only do

reports indicate that property prices and activity

in the property market are subdued, but credit to

the housing sector is drying up. Personal loans to

the housing sector, which grew by 25 per cent in 2007-08,

registered a much lower increase of 10.7 per cent

last year. And the increase in lending to the real

estate sector fell from 69 per cent to 38 per cent.

Finally, the evidence suggests that growth has once

again come to depend on an expansion of services,

with Services GDP growing faster than aggregate GDP.

But here too growth has been decelerating in most

areas. A disaggregated analysis suggests that there

is only one component of the services sector—Community

Social and Personal Services—that appears to have

registered an acceleration in GDP growth.. On the

other hand, the rate of growth of the other important

segments of services— Financing, Insurance, Real Estate

and Business Services and Trade, Hotels, Transport

and Communications—which were important players in

the aggregate growth story of recent years and incorporate

most of the so-called “modern services”, have shown

signs of deceleration.

Put all this together and the picture is by no means

comforting. Especially since this slowdown, with signs

indicating that it could persist, occurs in the context

of sharp inflation exceeding 12 per cent on an annualised

basis. Food articles are important contributors to

this high inflation rate. Since agricultural growth

appears to be slowing as well, this buoyancy in prices

is likely to continue. The observed ability of the

system to manage the effects of the difference between

agricultural and non-agricultural growth is clearly

now weakening, presaging a long episode of slow growth

and inflation, or stagflation.

It is in this background that we need to assess the

likely consequences of the implementation of the Pay

Commission’s recommendations, including the payment

of 40 per cent of the arrears that would give government

servants a windfall gain. Inasmuch as that gain would

result in increased expenditure and demand it would

have the salutary effect of spurring growth. But inasmuch

as the increased demand occurs in a context where

prices are already rising and agricultural supplies

are constrained it is bound to spur inflation as well.

It is, therefore, likely that a government faced with

a series of state elections that culminate in a national

election next year, would look to the foreign exchange

reserves the country has to resort to imports to hold

the price line. That may not be good for the long

run viability of domestic production, especially in

the agricultural sector. But what matters in practice

is what is good for the UPA, not what is good for

the country.

Percentage change over previous

year

in GDP at factor cost |

00

|

00

|

|

|

Q1 2007-08 |

Q1 2008-09 |

|

Agriculture, forestry & fishing |

4.4 |

3.0 |

|

Mining & quarrying |

1.7 |

4.8 |

|

Manufacturing |

10.9 |

5.6 |

|

Electricity, gas & water supply |

7.9 |

2.6 |

|

Construction |

7.7 |

11.4 |

|

Trade, hotels, transport &

comm |

13.1 |

11.2 |

|

Financing, ins., real est. &

bus. services |

12.6 |

9.3 |

|

Community, social & personal

services |

5.2 |

8.4 |

|

GDP at factor cost |

9.2 |

7.9 |

|

Source:

Central Statistical Organisation |

Table

1 >> Click

to Enlarge