|

On

February 4, the Reserve Bank of India took a major step

forward towards full convertibility of the rupee. It

announced that resident Indians can, with immediate

effect, remit an amount of up to $25,000 per calendar

year for any current or capital account transaction,

or a combination of both. This implies that resident

Indians would not just be able to open and operate foreign

currency accounts outside India, but can use the money

remitted to those accounts to acquire financial or immovable

assets without prior approval from the RBI.

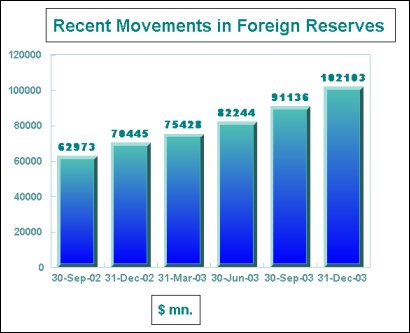

Chart

>> Click

to Enlarge

On the surface, the sum of $25,000 involved may appear

small, especially when compared to net capital inflows

into the country of $12 billion in 2002-03 and $6 billion

in the first quarter (April-June) of 2003-04, and reserve

accumulation of $17 billion during 2002-03, and around

25 billion during April to December 2003. But, looked

at otherwise, if one million Indians, or just 0.1 per

cent of the country's population choose to avail of

the facility in full, the outflow would be adequate

to wipe out the foreign exchange reserves accumulated

during the first three quarters of a year (2003-04)

that has seen record inflows of capital. It is not India's

new and old rich alone who would seek to exploit the

new ‘facility'. The large numbers of middle class households

who have members moving abroad on H1 B visas or for

educational purposes would see some reason for holding

an account, if not making some investment, abroad. A

million may not be a large figure for the number willing

every year to transfer the equivalent of Rs. 11.5 lakh

abroad at current exchange rates. Not surprisingly,

within a day after the new facility was announced, banks

have rushed to press, to advertise their willingness

to manage remittances under this head for interested

clients.

Needless to say, if all or a large part of capital inflows

are consumed in this fashion, it could send out a signal

that the country is losing its ability to meet its repatriation

commitments, either in the form of the returns that

would accrue to foreign investors or in the form of

permission to exit from investments in the country.

This could slow capital inflows or even result in outflows,

leading to a collapse in reserves and a financial crisis.

This is typically the way in which countries that are

temporarily the favourites of foreign investors and

experience a capital inflow surge often find themselves

the victims of outflows that lead to crisis. The "feast-or-famine"

syndrome characteristic of capital flows to emerging

markets has been documented widely. A reading of that

literature does warrant the conclusion that by beginning

the journey to full convertibility, the government has

opened the sluice gates to outflows that can empty its

foreign exchange reserves.

An analysis of the sources of reserve accumulation by

the RBI over a long period points to the important role

of inflows in the form of NRI deposits and foreign institutional

investor investments. Outstanding NRI deposits increased

from US$ 13.7 billion at end-March 1991 to US$ 31.3

billion at end-September 2003. Cumulative net FII investments,

increased from US$ 827 million at end-December 1993

to US$ 19.2 billion at end-September 2003. These kinds

of investments rarely, if ever at all, finance new investments

in the domestic economy. These are also typically inflows

that would be reversed in case of any sign of uncertainty.

Thus, comparisons of likely outflows with the size of

inflows and the extent of reserve accumulation are not

without some basis. Reserve accumulation occurs when

the RBI is forced to intervene in the foreign currency

market and purchase dollars or other foreign currencies.

This it is forced to do when large capital inflows result

in a surplus of foreign exchange in the system, since

the supply of foreign exchange exceeds demand from firms

and individuals for permitted current and capital account

transactions such as imports, private or business travel,

remittance for gifts, donations, study abroad, medical

treatment, investment abroad and so on. When the supply

of foreign exchange exceeds such demand, the rupee tends

to appreciate vis-à-vis foreign currencies under India's

liberalized and market-driven exchange rate regime.

A rising rupee increases the dollar value of India's

exportables and adversely affects her export competitiveness.

It is to prevent such appreciation that the RBI has

been purchasing foreign exchange in the market and enhancing

its reserves.

Beyond a point, however, increasing reserves are a problem

for the central bank. When the foreign exchange assets

of the RBI rise, so do its liabilities, which typically

imply an increase in money supply. Since allowing that

to happen amounts to loosing control of its monetary

policy lever, the central bank chooses to retrench other

assets such as government securities to sterilize inflows.

Unfortunately for the Reserve Bank of India, foreign

capital inflows have in recent months been massive and

unrelenting. The consequent huge and rapid increase

in its reserves, can no more be sterilized easily, since

the central bank has already brought down its holding

of government securities substantially.

Excessive reserve accumulation is a problem also because

of its negative balance of payments implications. Investors

bringing in the capital earn minimum returns of around

7 percent. The maximum would be many multiples of that,

especially from capital gains associated with recent

investments in the stock market. These returns have

to be paid out in foreign exchange. On the other hand,

when the dollar flowing into the country are acquired

by the RBI and invested through central and commercial

banks, the returns are much lower. According to the

RBI, during the year 2002-03 (July-June), the return

on foreign currency assets, excluding capital gains

less depreciation, decreased to 2.8 per cent from 4.1

per cent during 2001-02, because of lower international

interest rates. This implies that the interest associated

with capital inflow and its accretion as reserves involves

little foreign exchange earning but substantial foreign

exchange payouts.

Finally, it is becoming diplomatically increasingly

difficult to accumulate reserves in order to prevent

currency appreciation. India has been identified along

with China as a country whose large reserves prove that

it has an "undervalued" currency that discriminates

against imports from the US. The pressure to allow the

currency to appreciate is therefore on the increase.

For all these reasons, it had become clear to the central

bank and the government that something had to be done

to prevent further rapid reserve accumulation. The choice,

therefore, was either to curb flows or to stimulate

the demand for foreign exchange. Given its unthinking

commitment to liberalization and "reform",

it's the latter route that the government has chosen.

Recent months have, therefore, seen not just irrational

and sometimes bizarre trade liberalisation manoeuvres,

such as across-the-board duty reductions and the license

to bring in laptops duty free as part of baggage, but

the relaxation of ceilings on remittances abroad for

purposes as varied as education, health and investment.

All of these have proved inadequate given the fact that

India has proved to be the flavour of the season for

foreign investors, who have rushed into the country

in herd-like fashion.

It is this set of circumstances, rather than rational

decision-making, that has forced the government to all

on a sudden liberalize controls on capital account outflows.

The sequence has to be noted. First, regulations regarding

purely financial inflows are liberalized to attract

capital into the country so as to finance the outflows

that trade liberalization was expected to result in.

Since the initial response of foreign investors was

lukewarm, further liberalization, in the form of relaxing

ceilings on FII holdings of equity in firms in different

sectors, was resorted to. Suddenly, for reasons extraneous

to the performance of the Indian economy, which has

grown at an indifferent rate for at least three consecutive

years before the current "recovery", inflows

accelerate. Unable to manage those inflows, the government

attempts to encourage foreign exchange profligacy through

liberalization of foreign exchange access for various

current account transactions. When even that proves

inadequate, it opts for capital account convertibility.

The problem is that when

controls on capital account outflows are liberalized,

it is difficult to control the volume of outflows. And

if large outflows raise the threat of depreciation in

the value of the rupee, outflows accelerate and capital

flight out of rupee denominated assets would occur.

Having whetted the appetite of India's rich for a financial

foothold abroad, it would be extremely difficult to

reverse the decision. Moreover, any such reversal would

encourage the flight of financial investors out of the

country. A currency and financial collapse would be

inevitable. In short, the sluice gates have been opened.

It is, therefore, clearly time to prepare for the coming

crisis.

|