|

The

deliberate adoption of a myopic vision is writ large

in the India Shining campaign, with its principal focus

on a successful, urban, middle India. This effort to

manipulate perspective is revealed in the use of figures

of economic performance in a single year or a couple

of selectively chosen ones to cloud events of even the

immediate past. It is reflected in the tendency to emphasise

and elevate the double effect of speculative FII inflows

in sharply increasing India's foreign exchange reserves

position on the one hand, and triggering a boom (however

volatile) in India's stock market on the other, while

ignoring the poor performance of the commodity producing

sectors. It is seen in the effort to celebrate new,

and yet marginal, trends in employment while downplaying

the devastation that poor agricultural labourers and

small farmers must have faced because of the drought

in 2002-03, whose effects on production was far more

severe than any prediction – official or otherwise.

A typical example of such new trends is the rapid rise,

albeit from a small base, in employment and revenues

from IT-enabled services like call centres, that have

reportedly generated jobs for around 1,70,000-2,00,000

young Indians.

The effects of this myopic vision are seen in the approach

to all sectors of the economy. Consider, for example,

industry. Conventionally urban prosperity was linked

to the advance of a dynamic industrial sector. Unfortunately,

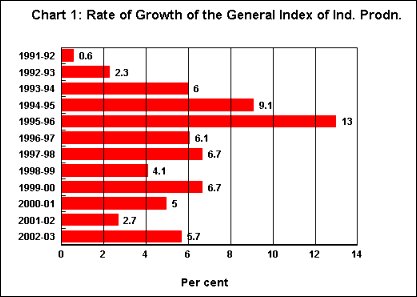

going by the figures on the Index of Industrial Production,

industrial growth was at an unremarkable 6.3 per cent

during the first nine months of so-called boom year

2003-04, when agricultural production shot back from

its 2002-03 trough.

Chart

1>> Click to Enlarge

During the peak of the liberalization and reform euphoria

in 1994-95 and 1995-96, respectively, industrial growth

was at 9.1 and 13 per cent respectively, well before

the NDA's magic ostensibly began to transform this country.

The lack of dynamism that this decline in industrial

growth since the early mid-1990s reflects is all the

more disturbing because it combines with an overall

stagnation in the investment rate in a country that

is supposedly on the move and is the darling of foreign

investors.

Chart

2>> Click to Enlarge

As Chart 2 indicates, after rising in the first half

of the 1990s to touch a peak of 27.3 per cent in 1995-96,

the rate of capital formation in the economy has remained

well below that level in all but one of the subsequent

years. This decline and subsequent stagnation in investment

occurs despite the visible signs of movement, in sectors

like telecom and more recently in highway construction

– sectors that the Prime Minister has identified as

epitomising the direction the rest of India should take.

What he missed out was the fact that investment in these

sectors, at whatever rates they are actually occurring,

failed to pull along investment in the rest of the economy.

Conventionally, through its effects on profits and utilisation

in the rest of the economy, future investment is triggered

elsewhere. This, Shining India has not been able to

ensure. Clearly, if investment is not buoyant, an economy

could not be. Seen from the angle of vision of the principal

commodity producing sector, what is happening is that

the early gloss is fading under the NDA.

The lack of investment has been accompanied by dismal

trends in employment over the 1990s, despite the Planning

Commission's propagandist claims of the government having

"created" 84 lakh jobs every year over the

last years. This intriguing claim, it now appears, is

based on a comparison of the "usual status"

workforce figures yielded by two NSS surveys relating

to July-June 2000 and July-December 2002, which have

as their mid-points the two dates (1 January 2000 and

1 October 2002) that provide the 33-month period for

which the claim is being made. As Prof. K. Sundaram

from the Delhi School of Economics has pointed out (Economic

Times, 14 February 2004), there are a number of problems

with using these surveys for such short term comparisons.

Thus, the NSS surveys seem to suggest that employment

increased by 76 lakh (not 84 lakh as claimed) in the

33-month period between 1 January 2000 and 1 October

2002, 68 lakh in the 21-month between 1 January 2001

and 1 October 2002, and 300 lakh in the 24-month period

between 1 January 2000 and 1 January 2002, while it

declined by 90 lakh in the 9-month between 1 January

2002 and 1 October 2002. If the last of these is used

as the basis for judgement, Indian is clearly not shining

more recently. Given the specific focus of each round

of the NSS, using the figures yielded for such short

term comparisons may not be the best way to assess increases

(or decreases) in absolute employment.

But that this is not all. Even if we stick by the two

surveys and the two time points used by the Planning

Commission in its advertisement, which claims that in

the last three years "we" are getting close

to achieving the Prime Minister's target of providing

one crore new employment opportunities every year, the

evidence on "whose India is shining" is quite

damaging. First, urban areas which account for 23 per

cent of the workforce account for 40 per cent of the

increase in "employment opportunities" during

the 33-month period. Second, the number of women workers

in the country declined by 15 lakh or around 5 lakh

per annum. Third, this decline in the case of women

in rural areas amounted to close to 10 lakh per annum.

Fourth, the number of women workers in the 15-34 age

group declined by 17 lakh per annum. Finally, the share

of all those in the 15-34 age group (who feature prominently

in the India Shining campaign) in the new employment

opportunities claimed to have been created amounted

to just 25 per cent, whereas those aged '60 and above'

accounted for around 17 per cent. Once we take note

of these figures, little needs to be said about the

dismal "quality" of the "employment opportunities"

that the government claims to have created.

These trends, in output, investment and employment are

indeed surprising given the fact that this has been

the period when huge concessions and tax benefits have

been handed out to India's corporate sector with the

aim of reviving the animal spirits of India's dormant

monopoly groups and kick-starting investment. The spur

to industry does not stop there. It also comes from

the consumption and housing finance boom that has been

spurred by the reckless lending at declining interest

rates that financial liberalisation has resulted in.

According to reports on a study undertaken by KSA Technopak,

personal credit outstanding in the country rose by 300

per cent from Rs. 40,000 crores in 2000 to Rs.1,60,000

crores in 2003 and is still growing. Though this still

accounts for only 12-14 per cent of aggregate consumption

spending in the country, its concentration among the

"middle class", especially in urban India,

would imply that there is a growing credit overhang

that is based on excessive exposure to a small section

of the population. These are also the sections which

are being provided large volumes of housing finance

at low nominal interest rates by financial firms desperate

to find vents for the liquidity that they can access.

The Reserve Bank of India has already warned housing

finance companies about the high risk portfolio that

many of them are carrying.

This credit boom may be increasing fragility in India's

increasingly liberalised financial sector. But it is

also helping along sales volumes in corporate India

and holding up profits. The problem however is that

having bought earlier versions of the India Shining

campaign, corporate India has created so much excess

capacity in many areas that the increases in demand

only go to increase utilisation of already created capacities,

and has not helped spur investment in recent times.

However, combined with the concessions that have been

handed out to the private sector that we referred to

earlier, these trends have indeed helped the corporate

sector declare reasonably high profits. This is one

more recent trend that provides the gloss for India's

shine. Those profits and the fact that India is the

flavour of the season for foreign institutional investors

have provided the basis for a spurt of speculation in

the stock markets taking the Sensex to new temporal

highs, even if this is accompanied by substantial volatility.

Therefore, the Sensex has become one more barometer

for a government in search of the shine that is constantly

rendered murky by visible signs of poverty.

That search has been successful also because of another

consequence of the stock market rush: the surge of FII

investments in the country that have contributed substantially

to the sharp and sudden increase in the size of India's

foreign exchange reserves. Having crossed the $100 billion

mark, those reserves have become a source of embarrassment

and a problem for the government. Embarrassment because

those reserves, which arise because of RBI purchases

of foreign exchange to prevent the rupee from appreciating

and affecting India's export competitiveness adversely,

are now being cited as evidence of the fact that the

rupee is "undervalued". Revalue the rupee,

the US argues, so that imports are not discriminated

against in the Indian market.

The reserves are also a problem because, while the inflows

that deliver them earn high returns that can be repatriated

in foreign exchange, their investment abroad yields

the country a less than 3 per cent average return. This

implies that the country is paying a high price in foreign

exchange in order to accumulate and maintain such reserves.

To boot, the inflows that contribute these reserves

are in the nature of "hot money" flows. If

and when foreign investors begin to suspect that the

shine was never there, there could be a rush of investment

out of the country. Since the government, egged on by

the reserves, has decided to encourage profligate foreign

exchange spending and investments abroad by ordinary

citizens who have the wherewithal, any such exit would

soon turn into an exodus, precipitating a financial

crisis of a kind that the world is all too familiar

with.

Unwarranted claims in all these areas is sought to be

strengthened by figures of recent performance. But even

here the lie is hard to sell. It is indeed true that

growth this year in agriculture has been remarkable.

But that clearly is because of the bad monsoon-induced

collapse of agricultural output that makes a return

to output levels achieved in 2001-02 deliver a remarkable

growth rate. It is true that the recovery in agriculture

combined with a credit-driven spending boom has helped

industrial growth along. But that growth is far short

of what the advocates of liberalisation promised to

deliver and did manage to do so for a brief period in

the mid-1990s when the NDA was yet to take power. It

is true that the software and IT-enabled services sector

is witnessing high rates of growth of revenues, exports

and employment. But that occurs on a low base in a sector

which remains an enclave and cannot compensate for the

slow growth in the commodity producing sectors. It is

also true that India's foreign exchange reserve position,

its stock markets and its financial sector are buoyant.

But all that also reflects the fragility that underlies

the kind of jobless growth process that the NDA government

has unleashed during its tenure.

Why is the government choosing to manipulate the nation's

vision by behaving as if what it says is true? It should

be obvious that the real intent of the India Shining

slogan is to conceal the poor performance of the commodity

producing sectors and the fragility of much else of

the economy. If India's economy is shining, that shine

is similar to the light reflected off an overblown bubble.

The coming election, therefore, is also one that would

decide who would pick up the pieces when that bubble

does burst. |