Perhaps

more than any other purely economic issue, inflation

has always been a pressing socio-political concern

in India. That is because the vast majority of our

working people receive incomes that are not indexed

to prices, and are therefore directly and adversely

affected especially by the rise in prices of necessities.

Since money wages and the incomes of small businesses

of the self-employed adjust to rising prices only

with a lag, this means that their real incomes get

eroded over time. So inflation has direct income distribution

consequences.

Of

course, periods of slow price rise are not necessarily

always beneficial, even for the poor. If low inflation

is the result of restrictive macroeconomic policies

that reduce economic activity and employment growth,

it can be even worse for the mass of people than moderate

inflation rates that are associated with rising aggregate

income and employment.

Recent macroeconomic policy discussions have been

rather complacent about the issue of inflation in

India, especially given the relatively low rates that

prevailed over much of the past decade. However, in

the past year the increase in the overall inflation

rate, as well as the rise in prices of particular

commodities, have brought into question both the sustainability

of the current economic growth process and the efficacy

of public management of price rise in particular sectors.

Chart 1 >>

Click

to Enlarge

Chart

2 >> Click

to Enlarge

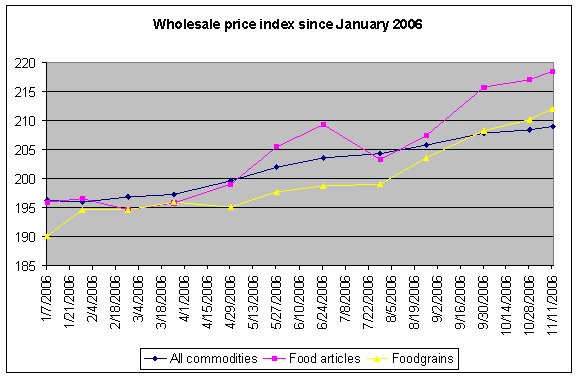

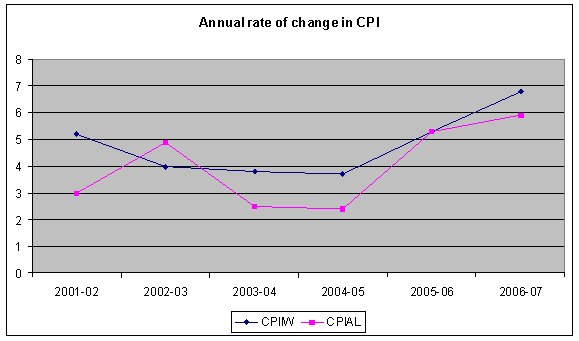

The

charts indicate that consumer prices have definitely

increased in the recent past, such the annual rate

of inflation at present is between 6 and 7 per cent.

Movements in the Wholesale Price Index (WPI) show

that the recent rise has been sharpest in food articles,

including food grains, which still form the most basic

of necessary goods. Indeed, for some commodity groups

like pulses, prices have risen by nearly 33 per cent

between January and November this year.

What

has brought about this recent acceleration of inflation

in the Indian economy? In a statement before Parliament

in July (as reported in the Rajya Sabha proceedings

of 24 July 2006) Finance Minister P. Chidambaram claimed

this was the result of three forces. According to

him, two of these are completely out of the government’s

control.

The first factor Mr. Chidambaram described as the

cost-push effect emanating from the hardening of world

commodity prices, such as oil and other fuels, minerals

and metals. With world prices in these increasing,

it is only to be expected that domestic prices will

also rise. However, in fact global oil prices have

been falling in recent times and are now below the

levels of even one and a half years ago. The same

is true of most agricultural commodities, and of some

minerals and metals imported by India. So cost-push

inflation because of higher import prices is unlikely

to explain the rise in Indian prices after June 2006.

The second factor he mentioned was the demand-pull

effect of higher economic growth, which puts pressure

on available supplies and therefore leads to what

he described as a temporary rise in prices. Certainly

there is evidence that rapid growth in some sectors

has put pressure on raw material supplies and may

lead to supply bottlenecks of particular inputs, including

not only raw materials and intermediates, but also

some forms of skilled labour.

However, this process – and the resulting price rise

- is not a necessary concomitant of high growth. It

is worth noting that the Chinese economy has grown

very rapidly for nearly thirty years, with only moderate

inflation. Even in the current year, when the Chinese

economy is apparently growing by more than 10 per

cent in real terms, inflation has been only 1.4 per

cent at an annual rate. So clearly, rapid growth in

domestic demand need not lead to higher inflation.

Further, since China is also a more import-dependent

economy than India, importing a greater proportion

of inputs for manufacturing production, it should

have been more adversely affected by the rise in world

commodity prices that Mr Chidambaram spoke of. Instead,

inflation rates have been lower than in the past!

The third factor that Mr. Chidambaram mentioned is

what he refers to as ''supply shocks'' but which would

be better described as poor management of critical

areas of the economy. Here, in fact, the Finance Minister

probably hit the nail on the head, perhaps inadvertently.

He referred to the mismatch between demand and supply

in important commodities such as wheat, pulses and

sugar, suggesting that unexpected output shortfalls

for these crops led to a temporary rise in prices

which would get mitigated once supplies were enhanced,

for example through imports.

But this is only part of the story. It is misleading

to speak only of crop failures, for what happened

was essentially a policy-created process that was

subsequently mismanaged. The government allowed the

entry of large (and multinational) private players

into the grain trade, and opened up the futures market

for trading in these essential commodities, which

all have a history of hoarding. Having thus allowed

for speculation, the government was then very surprised

when it actually happened.

In wheat, for example, the Food Corporation of India

was unable to procure adequate amounts for the public

distribution system because private players like Cargill

were offering higher prices to the farmers. Procurement

declined by nearly 40 per cent compared to last year

and wheat stocks fell by 20 per cent to less than

7 million tonnes. This was not only inadequate for

the requirements of the government in terms of the

PDS and school meals programmes, but also insufficient

to quell speculative activity in wheat markets when

prices started to rise.

Eventually, the government was forced to import wheat

at prices several times higher than what it had been

willing to pay Indian farmers, and in the meantime

consumers had to cope with rising prices of wheat.

A similar story operates for pulses, except that mitigating

imports have not yet occurred so the price rise continues

unabated.

This is such expensive incompetence that in any country

with real democratic accountability, heads would have

rolled over this. But in India, ministers can talk

glibly of ''supply-demand imbalances'' as if these

were somehow completely outside the purview of government.

The government is indeed now concerned about inflation,

but unfortunately the knee-jerk response has been

to use the blunt instrument of the interest rate.

In the past months, the RBI’s discount rate has been

increased three times, most recently on October 31.

But this affects all productive sectors alike, and

has disproportionately negative effects upon small

enterprises that already find it more difficult to

get bank credit.

Instead of this blanket measure there should have

been more nuanced and directed interventions addressing

the sectors in which speculative bubbles are clearly

visible. The stock market, for example, continues

to be irrationally exuberant, and the imposition of

a capital gains tax at this point could only have

a salutary effect, besides raising more revenue for

the government. The real estate market is clearly

overheating – house prices in the metros are estimated

to have more than doubled in the past two years. Yet

the banking system and the income tax structure continue

to encourage property loans.

Clearly, the recent rise in inflation reflects not

higher growth but just economic mismanagement.