India,

the government would have us believe, is the new growth

''miracle'' in the developing world. According to

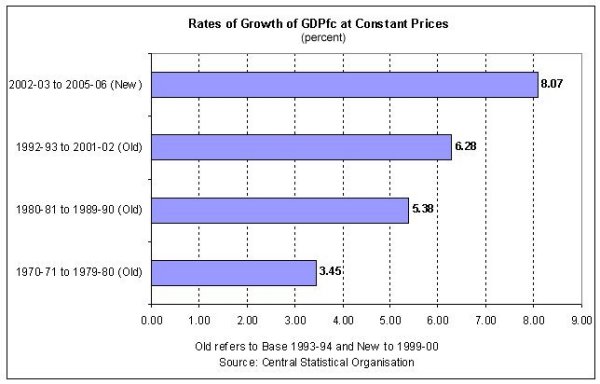

official figures, GDP growth has accelerated from

its ''Hindu rate'' origins of around 3.5 per cent

in the 1970s and earlier to 5.4 per cent in the 1980s,

6.3 per cent during the decade starting 1992-93 and

an annual average rate of more than 8 per cent during

the three years ending 2005-06. Since this acceleration

has occurred in a context of limited inflation, the

government is now targeting a further rise to 9 and

even 10 per cent over the Eleventh Plan.

Chart 1 >>

Click

to Enlarge

However, in the

midst of the celebration over the acceleration of

growth, certain features of the growth trend that

call for caution are often ignored. To start with,

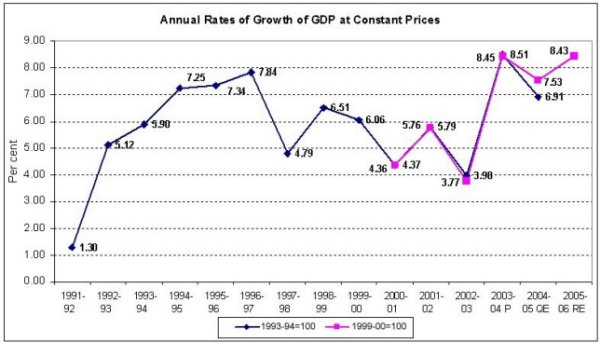

the 8 per cent rate of the last three years, which

is the first real evidence of India's transition to

''miracle'' status, may be more an exception rather

than the rule. High annual rates of growth of between

7 and 8 per cent were recorded even during the three-year

period 1994-95 to 1996-97, only to be followed by

a slump in rates to within the 4-6 per cent range

over the subsequent six years. As a result, the trend

rate of growth fell from 7.1 per cent during 1992-93

to 1996-97 to 5.3 per cent during 1997-98 to 2002-03.

Moreover, the GDP figures for the last three years

are still provisional, and are likely to be revised

downwards, even if marginally. Unless there are strong

reasons to believe that the growth rates they reflect

are robust and sustainable, it may be prudent to hold

back on the celebration, which declares that higher

growth is the result of accelerated reform and calls

for pushing ahead with policies that increase economic

vulnerability.

Chart

2 >> Click

to Enlarge

A second feature of significance is the structure

of this growth. For some time now the rate of growth

of services GDP has been much higher than the rate

of growth of overall GDP. As a result the share of

services in GDP, which was around a third in the mid-1970s,

had risen to more than a half by 2004-05. More than

sixty per cent of the increment in GDP during the

period 1993-94 to 2004-05 was due to an increase in

GDP from services.

Services have also contributed significantly to the

recent acceleration of the growth rate, with rates

of growth of services GDP touching 8.2, 9.9 and 10.1

respectively in the three years ending 2005-06. Though

construction has performed even better, with corresponding

figures of 10.9 12.5 and 12.1 per cent respectively,

given the high share of services in overall GDP, that

sector would account for an overwhelming share of

the higher rate of growth.

This trajectory does make India's growth experience

unusual, if not unique. The sharp increase in the

share of services in GDP in India has occurred at

a much lower level of per capita income than characterised

the developed countries when they experienced a similar

expansion. There are, of course, reasons why growth

in developing countries today would reflect a premature

expansion of services. To start with, globally manufacturing

units today rely as much or more on management and

control as on technology to raise productivity and

reduce costs. This has increased the services component

in manufacturing GDP. The pressure to reduce costs

leads to the outsourcing of many of these functions,

resulting in the services component of manufacturing

GDP appearing as a separate revenue stream and generating

a consequent increase in services GDP. Inasmuch as

liberalisation leads to a faster adoption of imported

best practice technologies in developing countries,

they too would tend to reflect this tendency. Secondly,

the communications revolution has cheapened the cost

of communication services, resulting in a much greater

and earlier use of such services. Not surprisingly,

the reach of and revenues from communication services

has increased substantially in developing countries,

contributing to an increase in GDP from services.

Finally, the shift in emphasis in government spending

from participation in production to provision of a

range of public services tends to increase the share

of public administration (not to mention defence)

in GDP. Overall, these factors could trigger a diversification

of economic activity in favour of services at an earlier

stage of development than that expected on the basis

of the historical experience of the developed countries

of today.

However, even these factors cannot explain the Indian

experience, wherein unlike many other similarly placed

developing countries GDP from services now exceeds

50 per cent of the total. Services must be growing

faster than warranted by the above factors. What seems

to matter at the margin, is an increase in the exports

rather than domestic supply (and consumption) of services.

Services were earlier considered non-tradables since

they required in most cases the presence of the supplier

at the point of provision. But modern developments

have made a number of services exportable through

various modes of supply, including cross-border supply

through digital transmission.

Chart

3 >> Click

to Enlarge

Such exports do seem to play an important role in

India. Exports of software services, which amounted

to an average of 7.1 per cent of services GDP during

2000-01 to 2002-03, stood at an average of 11.2 per

cent during 2003-04 to 2005-06 and close to 14 per

cent in 2005-06. Software and business (largely IT-enabled)

services dominate services exports, accounting for

52.8 per cent of the total during 2004-05, 56.1 per

cent in 2005-06 and a massive 66 per cent in the first

quarter of 2006-07. There is reason to be sceptical

about the sustainability of this process of services-driven

growth, based on exports that are overwhelmingly directed

at one or a few markets. New alternative suppliers

may arise increasing competition and reducing India's

dominant market share in the outsourcing business.

The threat of job losses in the developed countries

may trigger a protectionist response against outsourcing

of services, as is already happening in some countries.

Or, a slowing of growth in the developed countries

may curtail corporate spending and therefore the demand

for outsourced services.

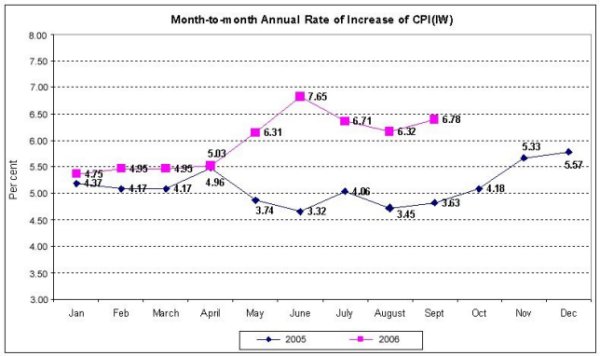

Finally, there is reason to believe that the services

surge is indeed triggering inflation, which is not

always reflected in the movement of whole sale price

indices. The annualised month-to-month increase in

the consumer price index for industrial workers, which

was at or below 5 per cent for all but one of the

16 months starting January 2005, has averaged 6.8

per cent during May to September this year. Moreover,

the deficit on the current account of India's balance

of payments, which stood at $10.6 billion in 2005-06,

when oil prices were still ruling high, has touched

$6.1 billion in the first quarter of financial year

2006-07 alone. This has prompted even The Economist

to declare that India's economy is overheating and

that the ''recent acceleration largely reflects a

cyclical boom, thanks to loose monetary and fiscal

policy.'' In its view, ''India cannot grow as fast

as China without igniting inflation because of its

lower investment rate, particularly in infrastructure,

and labour bottlenecks.'' That note of caution, which

predicts that the acceleration in GDP cannot last,

is unusual for a source that has repeatedly lauded

the performance of a country it sees as a tiger uncaged

by liberalisation. Fortunately, there is some respect

for the evidence rather than the hype at least in

some quarters.