While

economists of repute increasingly populate India's

policy-making establishment, holding regular or advisory

positions, economic policy itself seems ever more

self-contradictory. Consider, for example, the monetary

and fiscal policy recommendations being made by this

establishment as reported by the media. There is a

growing consensus within it that the Reserve Bank

of India should reduce overly high interest rates

to revive growth, even while maintaining a close watch

on inflation. In this view, inflation is a threat,

but not so much as to warrant stifling growth with

high interest rates. Responding to this pressure the

RBI has in its recent annual policy statement decided

to go in for a significant half-a-percentage-point

reduction in the repo rate.

Meanwhile another argument is gaining ground that

fiscal policy should play a greater role in controlling

inflation. The magic remedy for inflation being recommended

by adherents to this view is a reduction in the fiscal

deficit on the government's budget. Besides being

based on the belief that a reduced fiscal deficit

would automatically rein in inflation, this recommendation

is noteworthy for the specific way in which the reduction

is sought to be ensured. The government is being urged

to reduce its expenditure to curtail the deficit by

raising administered prices and user charges and cutting

budgetary subsidies. More specifically, a case is

being made out for raising the prices of petroleum

products so as to reduce subsidies or transfers to

the oil marketing companies. In recent times this

establishment demand has become an orchestrated campaign.

The argument from sources in the Finance Ministry

and the Planning Commission seems to be that if you

raise a set of prices that would reduce the fiscal

deficit, the overall rate of price increase would

be lower and not higher.

This push for raising administered prices to reduce

the fiscal deficit is supported by other similarly

''potent'' arguments. For example, former IMF chief

economist and advisor to the Prime Minister, Raghuram

Rajan, has at a function held to release the second

edition of a festschrift in honour of Manmohan Singh,

reportedly called for a complete freeing of diesel

prices in order to rein in the fiscal deficit and

boost the confidence of foreign investors.

All this is confusing indeed. It is known that since

petroleum products are in the nature of universal

intermediates, increases in their prices inevitably

have a cascading effect on costs and prices of other

commodities and result in an acceleration of inflation.

And since cost-push inflation is unlikely to be smothered

by reduced demand, it would be realised despite any

reduction in the fiscal deficit that may ensue. So,

while the RBI is being advised to cautiously stimulate

demand and growth, while keeping a watch on inflation,

the Finance Ministry is being cajoled into stoking

inflation by hiking a range of prices.

This policy muddle is all the more disconcerting since

it seems to be accompanied by a misreading of the

inflation scenario. The case for reducing interest

rates is backed by evidence that annual inflation

as measured by month-on-month Wholesale Price Index

(WPI) trends is much below its recent peak and still

declining. However, other evidence suggests that inflation

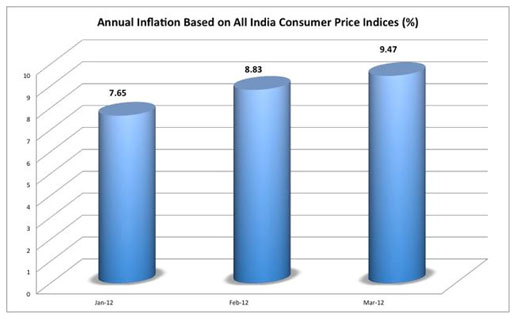

in India still rules high. According to the recently

released Consumer Price Index (CPI) numbers for March

2012, the annual month-on-month rate of inflation

had risen to 9.5 per cent from 8.8 per cent in February

and 7.7 per cent in January (see Chart). Since this

new series of All India Consumer Price Indices (with

2010 as base) are being released only from January

2011, these are the only months for which inflation

figures can be calculated as of now.

Chart

1 >> (Click

to Enlarge)

Those figures point in two directions. First, that

inflation at the retail level is high and rising,

especially because of inflation in the prices of food

articles such as milk and milk products, vegetables,

edible oils and eggs, meat and fish, besides fuels.

Second, that there is a growing divergence in inflation

trends based on the WPI, on the one hand, and the

CPI, on the other, with inflation based on the WPI

ruling lower and falling from 7 per cent in February

to 6.9 per cent in March.

To recall, the official justification for the release

of the new CPI series was the argument that the WPI

was not reflecting retail price trends adequately

and that inflation measurement based on retail consumer

prices was the international practice. The release

therefore marked the beginning of a transition in

which the government and central bank were to rely

on this new index rather than the WPI to compute the

''benchmark'' inflation rate in the economy.

Preponderant among the goods that enter the nation's

consumption basket and therefore the CPI would be

food articles and fuels. The supply of the former

articles is more volatile (because of variable monsoons,

for example) as well as less responsive in the short

run to changes in demand. Their prices, therefore,

tend to be more buoyant than that of most other commodities.

On the other hand, because of political and economic

developments in countries contributing a major part

of the world's energy supplies, the fuels component

of the consumption basket is also more ''inflation''

prone than many other goods. In the event, there is

a significant threat of an acceleration of inflation

as measured by the CPI.

Since according to that yardstick inflation is still

with us and would possibly climb, it could be argued

that the RBI, which is convinced that a hike in interest

rates is the appropriate weapon against inflation,

was pushed into cutting interest rates at this point.

However, the muddle over policy seems to afflict the

RBI as well. In its recent assessment of Macroeconomic

and Monetary Developments over the last financial

year, the central bank has also come out in favour

of increases in petroleum product prices and other

input prices to address the threat posed by ''suppressed

inflation''. That is, since the transmission of international

prices is inevitable, imported inflation can only

be suppressed and not avoided. And, if supressed,

inflation is a threat. However, if that be the case,

since further inflation is almost a certainty, the

RBI by its own logic would be forced to reverse its

interest rate reduction decision. Why cut interest

rates then?

Perhaps recognising this contradiction the RBI states:

''The upside risks to inflation on the one hand and

the depressed domestic growth outlook on the other,

warrant calibrated measures to maintain a sustainable

balance in a dynamic growth-inflation scenario.'' Presumably,

that is about as clear as one can get.

*

This article was originally published in The Hindu

on 20th April 2012 and is available at

http://www.thehindu.com/opinion/columns/Chand

rasekhar/article3336278.ece