It perhaps is a little too early

to predict the coming death of "neoliberalism",

or the economic philosophy that governments should

facilitate the functioning of "free" economic

agents rather than regulate them. More crudely put,

the idea is that markets should be left free to work

so long as they deliver profits. But globally evidence

has been growing that markets are just not working,

precipitating crises that requires bringing the state

back in. Oil prices have risen to levels close to

their inflation-adjusted historic highs and there

are no signs of quick adjustment. Governments, therefore,

need to ensure that prices in the areas they govern

are not left to the market. Financial markets that

had convinced some policy makers of their ability

to govern themselves are facing their worst crisis.

The sub-prime problem, everybody admits, is merely

a symptom of a deeper malaise which calls for a return

to intensive regulation. And the crisis in global

food markets, that has triggered food riots which

threaten to spread globally, has made clear that nations

cannot expect markets to deliver crucial public goods

like food security.

These, however, are the starkest and most critical

failures of neoliberal policy. But there have for

some time now been many areas where outcomes that

were initially considered signs of the success of

neoliberalism have turned out to be more of a problem

that an economic gain. In the Indian case, consider,

for example, the increase in foreign exchange reserves

because of a more liberal policy with regard to foreign

direct and portfolio investment and foreign borrowing.

During the 1990s the resulting accumulation of reserves,

though gradual, was quoted as evidence of the success

of neoliberal policy. In 1991, India had faced a foreign

exchange crisis. The change in policy that followed,

it is argued, ensured that we have enough and more

reserves to prevent the recurrence of any such crisis.

More recently, however, the perspective on reserves

has changed. The problem now is that we have too much.

Foreign currency assets accumulated by the Reserve

Bank of India crossed the $300 billion mark in early

April, having risen by more than $100 billion over

the previous year. Much has been written about the

difficulties this rapid accumulation creates for the

central bank in terms of both exchange rate and monetary

management. Rising reserves have as their counterpart

increases in money supply, which the RBI wants to

rein in given the inflationary conditions prevailing

in the economy. But, large and persistent inflows

of foreign currency imply that unless the RBI mops

up these dollars through its purchases, the rupee

would appreciate with adverse consequences for India’s

already beleaguered exporters. In practice, the RBI

has intervened substantially in forex markets, even

if it has not been completely successful in stalling

rupee appreciation.

Caught in this quandary, the RBI and, more recently,

the government, have been contemplating the possibility

of limiting inflows. But the efficacy of any measures

adopted towards that end would depend on the kind

of inflows that predominantly account for such accumulation.

Detailed figures on the sources of accretion of foreign

exchange reserves over the period April to December

2007 (Table 1), recently released by the RBI, permit

an assessment of the room for manoeuvre the government

has to adopt policies that can realise its goals.

The figures show that, after allowing for valuation

changes, foreign currency reserves with the RBI rose

by $76.1 billion between the beginning of April and

the end of December of 2007.

Table

1: Sources of Accretion to Foreign Exchange

Reserves |

|

April-December

2007 |

April-December

2006 |

Current

Account Balance |

-16 |

-14 |

Capital

Account (net) (a to f) |

83.2 |

30.2 |

Foreign

Investment (i+ii) |

41.4 |

12.8 |

(i)

Foreign Direct Investment |

8.4 |

7.6 |

(ii) Portfolio Investment |

33 |

5.2 |

Banking

Capital |

5.8 |

0.2 |

of

which: NRI Deposits |

-0.9 |

3.7 |

Short-Term

Credit |

10.8 |

5.7 |

| External

Assistance |

1.3 |

1 |

| External

Commercial Borrowings |

16.3 |

9.8 |

| Other

items in capital account |

7.6 |

0.7 |

| Valuation

change |

8.9 |

9.4 |

| Total

(I+II+III) |

76.1 |

27.8 |

Source:

Reserve Bank of India. |

Table

1 >> Click

to Enlarge

Among the factors underlying this rise in reserves,

are invisible receipts that helped cover a substantial

share of the deficit on the merchandise trade account

recorded during April to December 2007. According

to balance of payments figures from the RBI, gross

invisibles receipts comprising current transfers (that

include remittances from Indians overseas), revenues

from services exports, and income amounted to $100.2

billion during April to December of 2007. The increase

in invisibles receipts was mainly led by remittances

from overseas Indians ($13.8 billion) and software

services ($27.5 billion). After accounting for outflows

net invisible receipts stood at $50.5 billion.

The result of these inflows was that while on a BoP

basis the merchandise trade deficit had increased

from $50.3 billion during April to December 2006 to

$66.5 billion during April to December 2007, or by

more than $16 billion, the current account deficit

had gone up by just $2 billion from $14 billion to

$16 billion.

Given its small size, financing that deficit with

capital inflows was not a problem. The problem in

fact has turned out to be exactly the opposite: capital

inflows have been too large. Net capital inflows during

the first nine months of financial year 2007-08 amounted

to $83.2 billion. The three major items accounting

for these inflows were portfolio investments ($33

billion), external commercial borrowings ($16.3 billion)

and short term credit ($10.8 billion). To accommodate

these and other flows of smaller magnitude, without

resulting in a substantial appreciation of the rupee,

the central bank had to purchase dollars and increase

its s reserve holdings (after adjusting for valuation

changes) by as much as $76 billion or by an average

of around $8.5 billion every month. This trend has

only intensified since then with reserves having risen

by $33.8 billion between the end of December 2007

and the end of Mach 2008 or by an average of more

than $11 billion a month.

Though inflation is now the focus of policy attention

in the country, the government cannot postpone any

further dealing with this problem. The first step

the government needs to take is to put a stop to borrowing

abroad by Indian corporates, much of which is to finance

rupee expenditures. This is a clear form of a carry

trade in which loans at lower than domestic interest

rates in foreign markets is used to finance domestic

investments, some of which may even be speculative,

in the hope that the investor concerned can not merely

benefit from differentials in the rates of return

but also from the appreciation of the rupee between

the time the loan is contracted and repaid. There

is no reason why the government and the central bank

should be left with a macroeconomic muddle just because

sections of the private sector are looking for quick

returns. A return to a more stringent external borrowing

regime with lower ceilings is the obvious option for

the government.

Controlling the second of the flows that are resulting

in large accretion of foreign exchange reserves, namely,

portfolio investment flows is more difficult. This

consists of flows in which the acquisition of shares

by a single foreign investor in an Indian company

is less than 10 per cent of the aggregate shareholding.

This could occur either through the FII route involving

purchases of shares in the stock market or the private

placement route where share acquisition is ensured

through negotiations with the promoters. Acquisitions

through private placements now far exceed acquisitions

through the stock market. Thus, while the SEBI reports

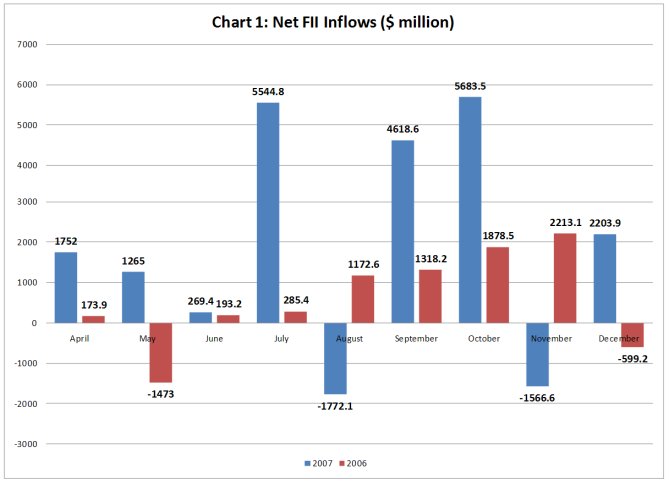

that net FII inflows in the form of equity and debt

during April to December 2007 was around $18 billion

(Chart 1), the RBI reports that net portfolio investment

during the period was $33 billion. Almost as much

portfolio investment seems to be coming through the

private placement route as is happening through the

FII route.

This suits foreign investors, investments by whom

would otherwise have been constrained by the volume

of free floating shares of listed companies that are

available for trading. This is known to be small.

Private placements suit Indian promoters as well because

they are in a position to sell, at a premium, a small

slice of shares, which would not threaten their control

over the company. If these are new shares issued for

the purpose and if the premium is large enough, the

company obtains a relatively large volume of resources

to finance expansion. In return for this investment

existing shareholders who now own a part of a larger

company need to reward the foreign investors with

dividends only when profits are made. If the promoters

had resorted to borrowing instead, interest and amortisation

payments would have to be paid irrespective of the

profit performance of the company. It is of course

true that foreign investors are resorting to such

investments in the hope of selling out these shares

at a later date at an appreciated price. If such expectations

are realised, the promoters gains because it increases

the market valuation of their own shares and therefore

their net worth. If these expectations are not realised

the promoters anyway benefit from the expansion of

the company financed with funds obtained at extremely

low cost. Here again, it is the search for significant

gains by domestic wealthholders that is partly driving

the large inflow.

Chart

1 >> Click

to Enlarge

As is known it is far easier for the government through

tax-based or quantitative measures to control capital

inflows through the stock market route. Controlling

inflows through directly negotiated purchases of equity

requires retracting some of the liberalisation of

foreign investment rules that has been adopted in

recent years. Thus far the government and the nation

have borne the costs associated with this form of

profit making by foreign and domestic wealth holders.

This may be defensible for some time. But with the

inflows persisting, exchange rate and macroeconomic

management proving increasingly difficult and instability

increasing, it is time to rethink at least some of

the liberalisation that has led up to this situation.

This is one more area where, the dangers of lightly

controlled or uncontrolled markets are being driven

home. It is better to learn the lessons early rather

than be burdened with a crisis whose dimensions are

unknown and solutions unclear – as is currently true

in the world of finance globally.